Notice is hereby given that an ordinary meeting of the Horowhenua District Risk and Assurance

Committee will be held on:

|

Date:

Time:

Meeting Room:

Venue:

|

Wednesday 7

June 2023

3.30pm

Council

Chambers

126-148 Oxford St

Levin

|

|

Risk and Assurance Committee

OPEN AGENDA

|

MEMBERSHIP

|

Chairperson

|

Cr Sam Jennings

|

|

|

Deputy Chairperson

|

Cr Paul Olsen

|

|

|

Members

|

Cr Alan Young

|

|

|

|

Cr Clint Grimstone

|

|

|

|

Cr Jonathan Procter

|

|

|

|

Mayor Bernie Wanden

|

|

|

|

Jenny Livschitz

|

Independent Member

|

|

|

Sarah Everton

|

Independent Member

|

|

Contact

Telephone: 06 366 0999

Postal

Address: Private Bag 4002, Levin 5540

Email:

enquiries@horowhenua.govt.nz

Website:

www.horowhenua.govt.nz

Full Agendas are available on Council’s website

www.horowhenua.govt.nz

Full Agendas are also available to be collected from:

Horowhenua District Council Service Centre, 126 Oxford Street,

Levin

Te Awahou Nieuwe Stroom, Foxton,

Shannon Service Centre/Library, Plimmer Terrace, Shannon

and Te Takeretanga o Kura-hau-pō, Bath Street, Levin

|

|

Risk and Assurance Committee

07 June 2023

|

|

ITEM TABLE OF CONTENTS PAGE

PROCEDURAL

1 Apologies 5

2 Public

Participation 5

3 Late Items 5

4 Declarations

of Interest 5

5 Confirmation

of Minutes 5

REPORTS

6 Reports

for Noting

6.1 Audit Management Letter,

Engagement letter and Audit plan for 2022/23 Annual Report 7

6.2 Treasury Report for the

March 2023 quarter 85

6.3 Risk and Assurance

Committee Resolutions and Actions Monitoring Report 95

6.4 Health, Safety and

Wellbeing Quarterly Report - June 121

6.5 Insurance Renewal Strategy

Update 141

6.6 Risk Management Status

Quarterly Report - June 2023 153

6.7 Internal Audit Work

Programme 225

6.8 Conflict of Interest

Report 227

6.9 Legislative Compliance

Report 243

6.10 Risk and Assurance Committee Work

Programme 247

7 Proceedings

of Committees

IN COMMITTEE

8 Procedural

motion to exclude the public 251

6.6 Risk Management Status

Quarterly Report - June 2023

d. Operational Risk

Register May 2023 Updated 10 251

e. Organisation

Risk Register May 2023 Updated 10 251

Karakia

|

Whakataka te hau ki te uru

Whakataka te hau ki te tonga

Kia mākinakina ki uta

Kia mātaratara ki tai

E hī ake ana te atakura

He tio, he huka, he hau hū

Tīhei mauri ora!

|

Cease the winds from the west

Cease the winds from the south

Let the breeze blow over the land

Let the breeze blow over the ocean

Let the red-tipped dawn come with a sharpened air.

A touch of frost, a promise of a glorious day.

|

1 Apologies

2 Public Participation

Notification of a

request to speak is required by 12 noon on the day before the meeting by

phoning 06 366 0999 or emailing public.participation@horowhenua.govt.nz.

3 Late

Items

To consider, and if thought fit, to pass a resolution to permit the

Council to consider any further items which do not appear on the Agenda of this

meeting and/or the meeting to be held with the public excluded.

Such resolution is required to be made pursuant to Section 46A(7) of

the Local Government Official Information and Meetings Act 1987, and the

Chairperson must advise:

(i) The reason why the

item was not on the Agenda, and

(ii) The reason why the

discussion of this item cannot be delayed until a subsequent meeting.

4 Declarations of Interest

Members are

reminded of their obligation to declare any conflicts of interest they might

have in respect of the items on this Agenda.

5 Confirmation of Minutes

5.1 Meeting minutes Risk and Assurance Committee, 1

March 2023

5.2 Meeting

minutes In Committee Meeting of Risk and Assurance Committee, 1 March 2023

5.3 Meeting

minutes Extraordinary Meeting of Risk and Assurance Committee, 26 April 2023

Recommendations

That the

meeting minutes of the Risk and Assurance Committee, 1 March 2023 be accepted

as a true and correct record.

That the

meeting minutes of the In Committee Meeting of Risk and Assurance Committee, 1

March 2023 be accepted as a true and correct record.

That the

meeting minutes of the Extraordinary Meeting of Risk and Assurance Committee,

26 April 2023 be accepted as a true and correct record.

|

Risk and Assurance Committee

07 June 2023

|

|

6.1 Audit Management Letter, Engagement letter

and Audit plan for 2022/23 Annual Report

File No.:

23/369

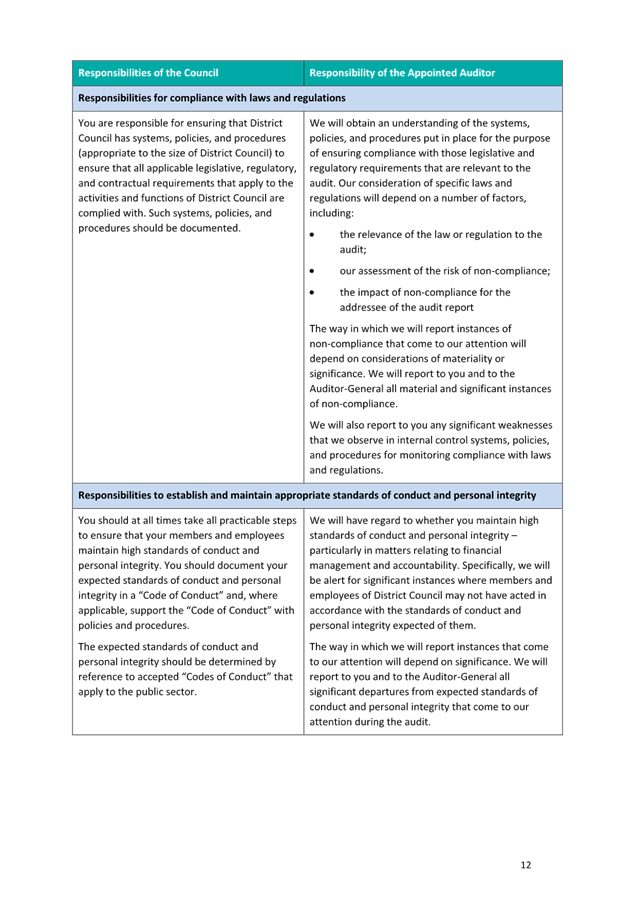

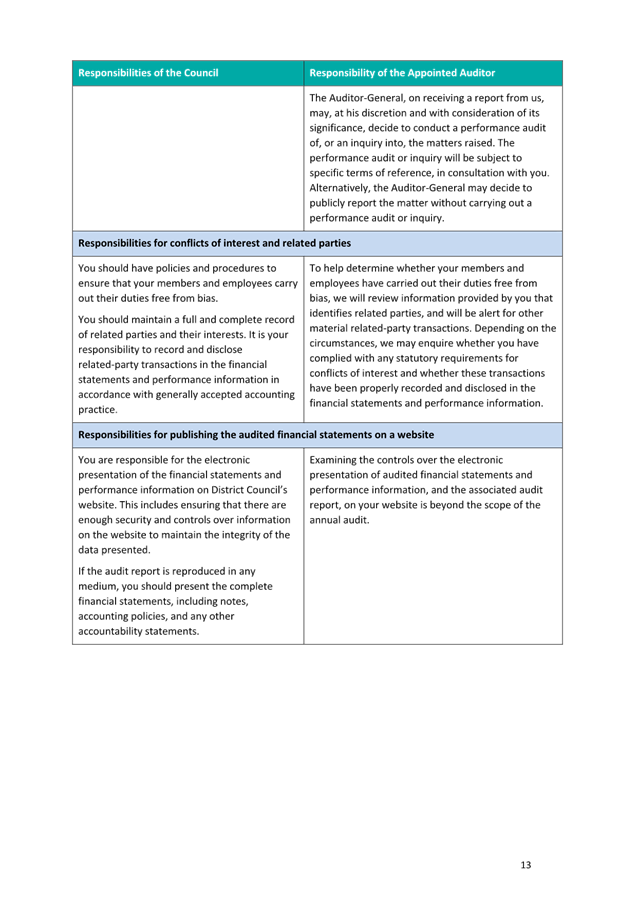

1. Purpose

1.1 This

report is to present to the Risk and Assurance Committee the Audit management

letter for the 2021/22 year and the engagement letter and audit plan for the

2022/23 Annual Report.

2. Recommendation

2.1 That Report

23/369 Audit Management Letter, Engagement letter and Audit plan for 2022/23

Annual Report be received.

2.2 That this

matter or decision be recognised as not significant in terms of s76 of the

Local Government Act 2002.

2.3 That the

Audit and Risk Committee agree to joining the Council meeting on 25 October,

2023 to review and adopt the Annual Report for 2022/23, noting that this will

provide greater opportunity for the report to be adopted prior to 31 October,

2023.

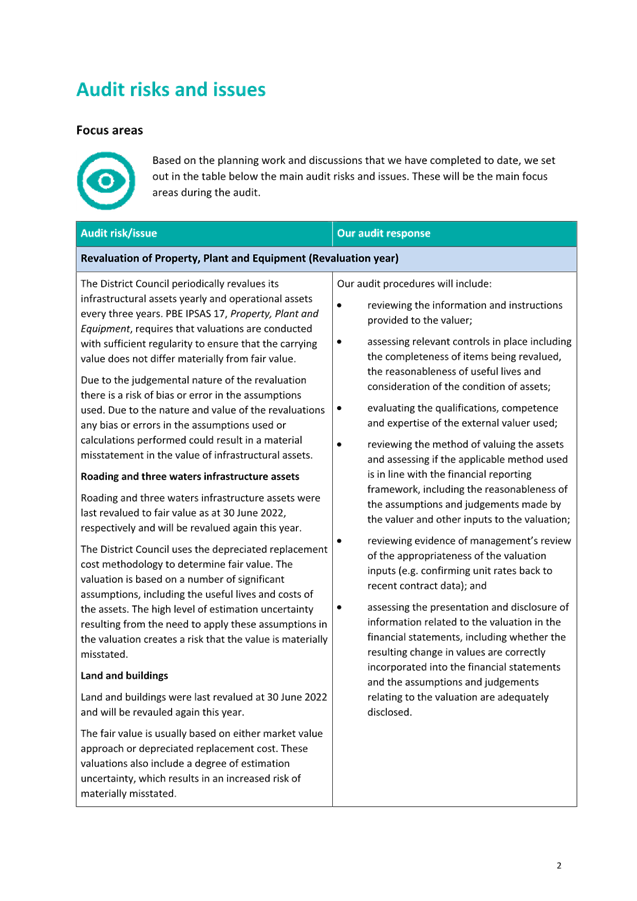

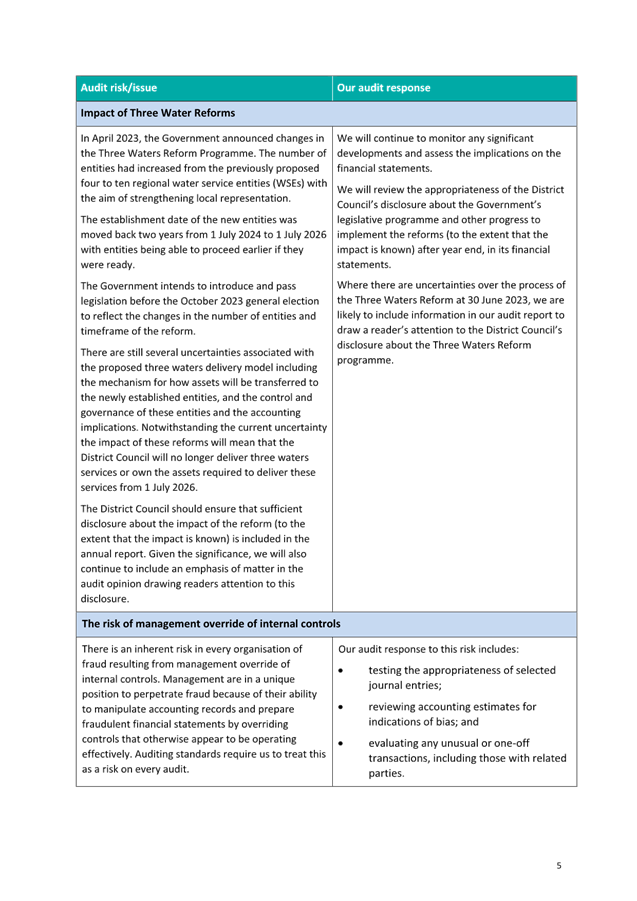

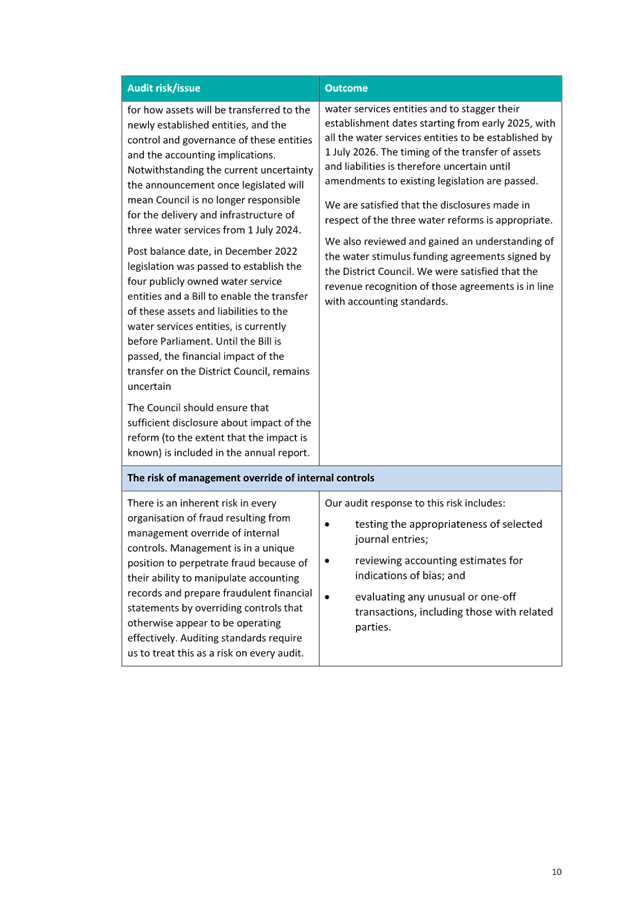

3. Issues for Consideration

Audit

Management Letter

3.1 A

copy of the draft management letter is included in Appendix D. It is in line

with the presentation that the Committee received from our Audit Director when

the Annual Report was presented. The points cleared by audit during this annual

report have been cleared from the monitoring report.

Audit

Engagement Letter

3.2 Audit

New Zealand have provided the engagement letter for the 2022/23 Financial Year.

This is included in Appendix B.

Audit

Fee

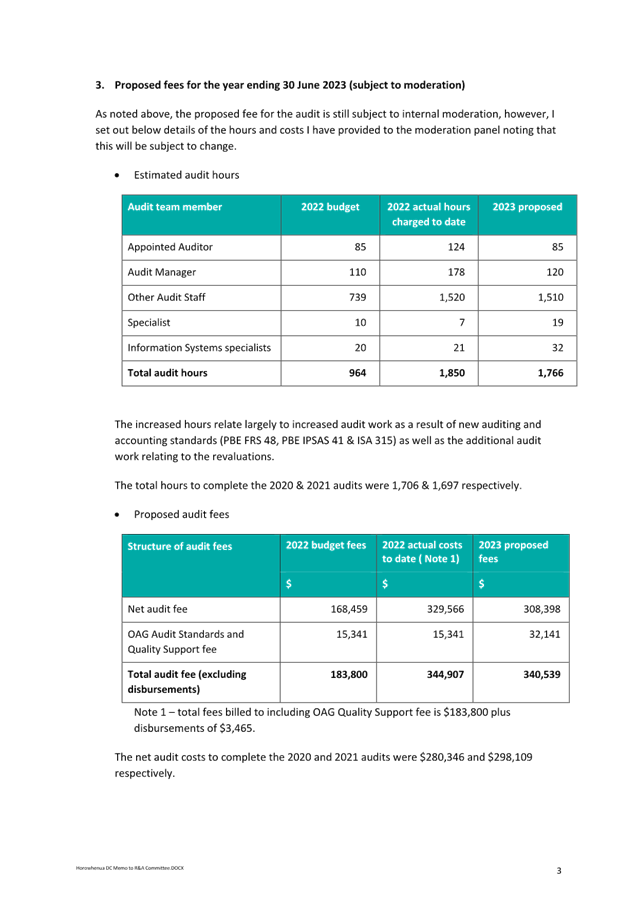

3.3 Audit

New Zealand have also recently begun a review of the 2022/23 proposed fees and

have provided an early indication that it could be as high as $340,000. This

compares to $194k for 2021/22. Appendix A includes a table outlining the

proposal.

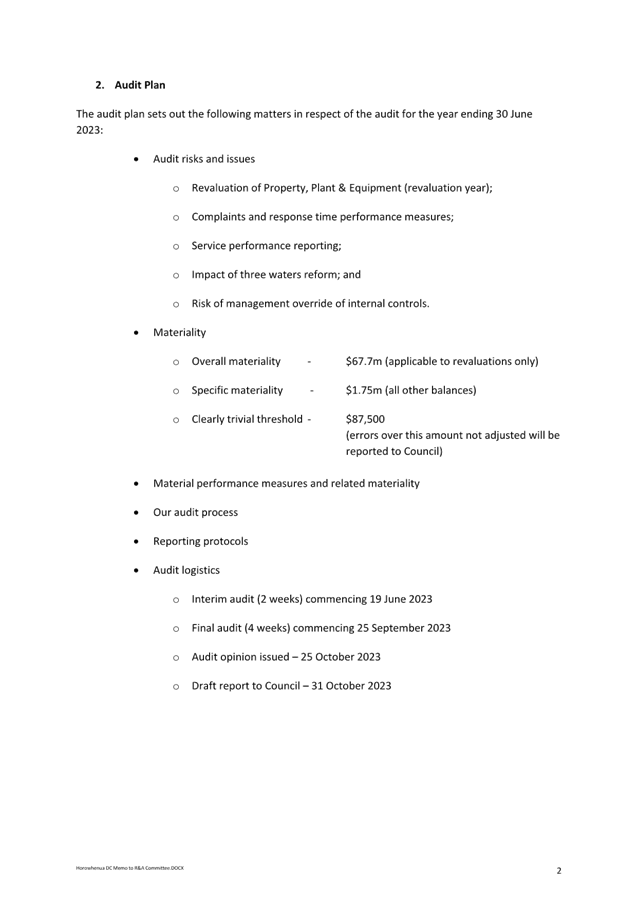

Audit

Plan

3.4 Audit

New Zealand’s overall Audit Plan is included within a summary of the

proposed timing that is included below. It is important to note that this plan

includes an assumption that the Council will need to revalue our three waters,

roading and land and building assets again for this financial year.

3.5 This

is a significantly costly exercise both in officer time, contracting external

valuers and auditor time to review. Officers are currently completing a high

level review of how assets values have changed (fair value assessment) to

determine if it is necessary to revalue the assets again.

Audit

Timing

3.6 In

preparation for the 2022/23 Annual Report, officers have been working with

Audit New Zealand to ensure that the Annual Report is adopted before the 31

October statutory deadline. This is proving difficult to meet as resources for

the audit have yet to be confirmed, and the focus of effort for Audit New

Zealand in the first part of September is on Central Government audits.

3.7 The

soonest that Audit New Zealand can agree to provide verbal audit clearance is

20 October 2023. This assumes a standard audit of four weeks.

3.8 While

the extraordinary Council meeting scheduled to adopt the 2022/23 annual report

is on 25 October 2023, this would not allow the reports to be released for the

agenda on 18 October with clearance already provided.

3.9 This

is an unfortunate timeframe that would also require independent members of the

Risk & Assurance Committee to join the Council meeting to review and

discuss the report prior to adoption rather than the standard process of first

taking the report through the Committee.

3.10 Council’s

Audit Director Clint Ramoo has agreed to provide regular updates for the

committee on the status of the audit.

Attachments

|

No.

|

Title

|

Page

|

|

a⇩

|

Memo to R&A Committee from Audit

NZ

|

10

|

|

b⇩

|

Audit Engagement Letter

|

14

|

|

c⇩

|

Audit Plan 2023

|

28

|

|

d⇩

|

Audit Management Letter - Final 2022

|

49

|

|

Confirmation of statutory

compliance

In accordance with section 76 of the

Local Government Act 2002, this report is approved as:

a. containing sufficient information about the options

and their benefits and costs, bearing in mind the significance of the

decisions; and,

b. is based on adequate knowledge about, and adequate

consideration of, the views and preferences of affected and interested

parties bearing in mind the significance of the decision.

|

Signatories

|

Author(s)

|

Pei Shan Gan

Financial Controller

|

|

|

Approved by

|

Jacinta Straker

Group Manager Organisation Performance

|

|

|

|

Monique Davidson

Chief Executive Officer

|

|

|

Risk and Assurance Committee

07 June 2023

|

|

|

Risk and Assurance Committee

07 June 2023

|

|

|

Risk and Assurance Committee

07 June 2023

|

|

|

Risk and Assurance Committee

07 June 2023

|

|

|

Risk and Assurance Committee

07 June 2023

|

|

6.2 Treasury Report for the March 2023 quarter

File No.:

23/333

1. Purpose

1.1 To

present to the Risk and Assurance Committee the Bancorp Treasury Reporting

Dashboard for the March 2023 quarter.

2. Recommendation

2.1 That Report

23/333 Treasury Report for the March 2023 quarter be received.

2.2 That this

matter or decision be recognised as not significant in terms of s76 of the

Local Government Act 2002.

3. Background/Previous Council Decisions

3.1 This

quarterly Treasury Reporting Dashboard is produced by Council’s Treasury

Advisors, Bancorp Treasury Services Limited, for the benefit of Executive

Leadership Team, Council and the Risk and Assurance Committee.

3.2 Standard

and Poor’s visited the Council and the Risk and Assurance Committee

during May as part of the annual ratings review. We are expecting to receive

our updated rating on 1 June 2023.

4. Issues for Consideration

4.1 Council

had $144m of current external debt as at 31 March 2023, comprised of Commercial

Paper (CP), Fixed Rates Bonds (FRBs) and Floating Rates Notes (FRNs), all

sourced from the Local Government Funding Agency (LGFA).

4.2 Cost

of funds as at 31 March 2023 was 3.78%. Interest rates had a very volatile

quarter, driven largely by swings in offshore markets. Officers work closely

with Council’s Treasury Advisor to manage fixed vs. floating rate cover.

4.3 Since

the last meeting, Council has entered into a new interest rate agreement with

BNZ in April for $10,000,000 starting 20 March 2026 and finishing on 20 April

2029 at 3.89%. This has been done to ensure an increased level of fixed rate

debt based on Council’s policy bands set out in the Liability Management

Policy. This corrects the reported breach for our level of fixed rate debt in

the 2-4 year bucket.

Attachments

|

No.

|

Title

|

Page

|

|

a⇩

|

Horowhenua Treasury Dashboard as at

31 March 23

|

87

|

|

Confirmation of statutory

compliance

In accordance with section 76 of the

Local Government Act 2002, this report is approved as:

a. containing sufficient information about the options

and their benefits and costs, bearing in mind the significance of the

decisions; and,

b. is based on adequate knowledge about, and adequate

consideration of, the views and preferences of affected and interested

parties bearing in mind the significance of the decision.

|

Signatories

|

Author(s)

|

Pei Shan Gan

Financial Controller

|

|

|

Approved by

|

Jacinta Straker

Group Manager Organisation Performance

|

|

|

Risk and Assurance Committee

07 June 2023

|

|

|

Risk and Assurance Committee

07 June 2023

|

|

Risk and Assurance Committee Resolutions and Actions

Monitoring Report

File No.:

23/362

1. Purpose

The purpose of this report is to report to

the Risk and Assurance Committee on previous resolutions.

|

2. Recommendation

2.1 That Report

23/362 Risk and Assurance Committee Resolutions and Actions Monitoring Report

be received.

2.2 That

this matter or decision be recognised as not significant in terms of s76 of

the Local Government Act 2002.

2.3 That

the Risk & Assurance Committee notes the Risk & Assurance Committee

resolution and actions monitoring report.

|

3. Issues for Consideration

This paper reports on actions generated

from Committee resolutions, and any requests noted through the minutes, or

requested for action accepted by the Chair.

This paper is provided for information.

Much like the Committee Work Programme, the Resolution Monitoring Report will

be standing item, and reported through at each committee meeting.

The monitoring actions have been carried

over from the Finance, Audit and Risk Committee from the previous Triennium.

Attachments

|

No.

|

Title

|

Page

|

|

a⇩

|

Risk & Assurance Committee Monitoring

Report

|

97

|

|

Confirmation of statutory

compliance

In accordance with section 76 of the

Local Government Act 2002, this report is approved as:

a. containing sufficient information about the options

and their advantages and disadvantages, bearing in mind the significance of

the decisions; and,

b. is based on adequate knowledge about, and adequate

consideration of, the views and preferences of affected and interested

parties bearing in mind the significance of the decision.

|

Signatories

|

Author(s)

|

Pei Shan Gan

Financial Controller

|

|

|

Approved by

|

Jacinta Straker

Group Manager Organisation Performance

|

|

|

|

Monique Davidson

Chief Executive Officer

|

|

|

Risk and Assurance Committee

07 June 2023

|

|

|

Risk and Assurance Committee

07 June 2023

|

|

6.4 Health, Safety and Wellbeing Quarterly

Report - June

File No.:

23/360

1. Purpose

1.1 To provide

the Committee with health, safety and wellbeing information and insight from 1

February to 30 April 2023 and to update the Committee on key health and safety

critical risks and initiatives.

2. Recommendation

2.1 That Report

23/360 Health, Safety and Wellbeing Quarterly Report - June be received.

2.2 That this

matter or decision be recognised as not significant in terms of s76 of the

Local Government Act 2002.

Issues

for Consideration

2.3 The Health,

Safety and Wellbeing (HSW) Dashboard report gives a broad overview of Lead and

Lag reporting across all of Council. It is designed to give Elected Members

assurance that HSW is being managed for all staff through worker engagement,

risk management and leadership. The variety of reporting captures multiple

aspects of data available to Council and allows the story of HSW across the

three month reporting period to be told.

2.4 Alongside the

HSW Dashboard report this month is a deep dive on Threatening Behaviour,

identified in the health and safety risk register as People Behaviour. This is

a critical risk and closely managed across all areas of Council. The deep dive

shows reporting, types of threatening behaviour reported per facility, training

and learning opportunities for staff, the range of current controls in place

and an example of a reported incident and the controls in place to mitigate the

risks.

Attachments

|

No.

|

Title

|

Page

|

|

a⇩

|

HDC Risk and Assurance Committee

HS&W Dashboard - RAC - June 2023 Final

|

123

|

|

b⇩

|

Threatening Behaviour Deep Dive

- RAC - June 2023

|

131

|

|

Confirmation of statutory

compliance

In accordance with section 76 of the

Local Government Act 2002, this report is approved as:

a. containing sufficient information about the options

and their benefits and costs, bearing in mind the significance of the

decisions; and,

b. is based on adequate knowledge about, and adequate

consideration of, the views and preferences of affected and interested

parties bearing in mind the significance of the decision.

|

Signatories

|

Author(s)

|

Tanya Glavas

Health & Safety Lead

|

|

|

Approved by

|

Ashley Huria

Business Performance Manager

|

|

|

|

Jacinta Straker

Group Manager Organisation Performance

|

|

|

|

Monique Davidson

Chief Executive Officer

|

|

|

Risk and Assurance Committee

07 June 2023

|

|

|

Risk and Assurance Committee

07 June 2023

|

|

|

Risk and Assurance Committee

07 June 2023

|

|

6.5 Insurance Renewal Strategy Update

File No.:

23/344

1. Purpose

1.1 To

provide an update on the 2023 -24 Insurance Renewal Workstream, this is

established to maximize the accuracy and effectiveness of Horowhenua District

Councils Insurance Renewal submission. Necessary to ensure the impacts of sharp

increase of inflation, significant weather events causing damage and GEO

Economic Confrontation is having on rising insurance premiums, doesn’t

impact on our community through increased rates.

2. Recommendation

2.1 That Report

23/344 Insurance Renewal Strategy Update be received.

2.2 That this

matter or decision be recognised as not significant in terms of s76 of the

Local Government Act 2002.

2.3 That the Risk

and Assurance Committee endorse the proposed planned approach for the Insurance

Renewal.

3. Discussion

Introduction

Due

to timing and the urgency surrounding the 2023/24 Insurance Renewal Process (T1

& T2 below), there was a need to start work in March 2023 to identify our

approach immediately. This would give us the best possible chance to provide a

Renewal Submission that is well informed and accurate for key areas such as the

Asset Register, Valuations, Asset location mapping with natural hazards against

associated risks and disaster recovery priorities.

Subsequently

an Insurance Renewal Working Group was established (table T3) to concentrate on

updating the asset register(s), asset mapping overlaid with our existing hazard

mapping, valuations, research on deductibles and comparisons with other

Councils and LG Agencies.

T1. Property

|

March/April 23

|

May 23

|

7 July 23

|

August 23

|

October 23

|

1 November 23

|

|

Pre renewal

review

|

Schedules

provided to Council

Meeting with AON

re submission

|

Council submit

renewals to AON (Broker)

|

Renewal

Submissions to Insurer (London)

|

Confirm Renewal

|

Start new

schedule and premium

|

T2. All other lines of coverage

|

March/April 23

|

7 July 23

|

September 23

|

October 23

|

1 November 23

|

|

Pre renewal review

|

Council submit renewals declaration to AON

(Broker)

|

Renewal Submissions to Insurer

|

Confirm Renewal

|

Start new schedule and premium

|

T3. Insurance Renewal Working Group

|

Team Member

|

Position

|

|

Rob

Benefield

Cathryn

Pollock

Ann

Clark

Stephen

Emerson

Barrie

Wallington

Steve

McTaylor-Biggs

Abraham

Chamberlain

|

Risk Manager

3 Waters

Transition Manager

GIS Analyst

3 Waters

Technical Lead

Information

Services Manager

Business

Financial Analyst & asset Management

Manager Financial

Planning

|

Risk Retention & Transfer

As indicated we are

faced with an opportunity to reassess how we manage the risk associated with

our Insurance Coverage of our key assets. The diagram illustrates the risk

transfer options on axes of the two elements – likelihood and size of

loss. There is a higher likelihood of small losses than of larger ones, and

catastrophic losses have a very low probability. As an organisation that main

revenue stream relies on rates from the community, we need to be accurate when

assessing the level risk we retain and the level we want to transfer to

insurance coverage. As an organisation in the past we have decided to transfer

a high level of risk without undertaking the appropriate due diligence to

ascertain what our levels of risk looked like i.e. over the last 3 years we

have invested over $5M in Insurance premiums to transfer risk whilst on making

claims of $45k in motor vehicle claims and $42k for a weather event (tornado)

claim.

T4.

Risk Transfer Options

Current Insurance Climate

The

rising costs of claims for extreme weather can have “far-reaching”

implications for businesses, governments and individuals. Extreme weather

insurance claims in New Zealand were at almost $200 million for the year ended

30 June 2022 that was well on track to break the record amount of $324 million

set in 2021. In 2023 we have already witnessed two significant weather events

with Cyclone Gabrielle the most significant weather event NZ has seen in a

century, which highlights the continuing increase in climate-related insurance

costs. Early estimates from AON for the 4 councils, Hastings District Council,

Napier City Council, Central Hawkes Bay and Hawkes Bay Regional Council is that

claims for the damage to council owned infrastructure is approximately $109

million.

Climate

coupled with rising building and development costs, impacted by increasing

interest rates and inflation continues to damage New

Zealand’s reputation in Global Property Markets and Re-insurance Markets.

It is expected the rating increases plus 10% – 15% before

rate adjustment on individual loss ratios. In the short to long term as

Insurers look to balance their books and return to making profit we could

possibly experience similar increases for the next 2-4 years.

In

the past, insurers’ role has been to provide clients with relief when

disaster strikes. But in a world where disaster doesn’t strike so much as

steamroll, the role of insurance companies is changing. Rather than being

reactionary, insurers are becoming more proactive in helping clients avoid and

plan for disasters. Insurance companies are taking steps now to encourage

better environmental planning & practices. They will be more selective

where they deploy capital and applying risk tolerance to specific areas.

As

a council we need to distinguish ourselves by providing accuracy to our renewal

submissions, this will require a programme redesign driven by an Insurance

Strategy. This will enable us to consistently provide our annual renewal

submission with confidence that our coverage provides an acceptable level of

risk that is accurately defined.

It

should be noted that insurance companies are using recent events to maximise

the opportunities to sell the need for insurance, often applying pressure to

organisations to opt for extensions on existing policies.

Insurance Premiums & Forecast

Based

on our brokers (AON) predictions Insurance premiums are set to rise 10-15% year

on year for the next 3 years as Underwriters look to retrieve money paid out

for natural disasters in recent years. Vehicle and Cyber Insurance by 30% this

year on its own. As per Table T.5 below and based on those predictions

averaging the increase at 12% per annum, HDC could see its premiums increase by

approximately $575k over this period.

Valuations

completed in June 2022 saw our assets change in value from $214m to $313m an

increase of $99M or 46%. Such is the pressure on inflation and the impacts from

Covid on supply this is the single biggest valuation increase over the last 30

years.

HDC

Insurance for infrastructure below ground sits separately to our other policies

above ground (MWLASS), this policy is managed through Local Authority

Protection Programme (LAPP). This is a fund primarily established for disaster

recovery. Our annual premium is currently set at $453,005.83 on declared asset

value of $721,193,862. Our claim threshold is set at $1m and a claim deductible

of $400k. The difference between threshold and claim deductible is the amount of

damage that needs to be reached and the deductible is what we will pay. Beyond

a threshold, central government will pay 60% of the restoration costs, leaving

local authorities 40%. Of the 78 local authorities in New Zealand, 22 are

currently Fund members.

T5. Premium Forecast Table

|

Coverage

|

Premium 22-23

|

23-24

12-30%

|

24-25

12 -30%

|

25-226 12-30%

|

|

Material Damage & Business Interruption

(MD&BI)

|

$922,990.08

|

$1,033,748

|

$1,157,798

|

$1,296,734

|

|

MD&BI Excess Layer Liability

|

$199,172.67

|

$223,073

|

$249,842

|

$279,823

|

|

General Liability

|

$25,423.05

|

$28,473

|

$31,890

|

$35,717

|

|

Motor Vehicle

|

$21,698.17

|

$28,270

|

$36,669

|

$41,070

|

|

Cyber Liability

|

$12,149.75

|

$15,794

|

$20,553

|

$22,977

|

|

Employers Liability

|

$1,938

|

$2,171

|

$$2,431

|

$2,723

|

|

Professional Indemnity

|

$131,476.05

|

$147,253

|

$164,923

|

$184,784

|

|

Public Liability & Professional Indemnity Excess

Layer Policy (PL&PI)

|

$14,111.46

|

$15,804

|

$17,701

|

$19,825

|

|

PL&PI Excess Layer

|

$1,426.63

|

$1,597

|

$1,789

|

$2,004

|

|

Statutory Liability

|

$4,967.16

|

$5,563

|

$6,230

|

$6,978

|

|

Aviation Hull (Drones)

|

$2,554.41

|

$2,860

|

$3,204

|

$3,588

|

|

Crime Policy

|

$6,390.00

|

$7,156

|

$8,015

|

$8,977

|

|

Fine Arts Special Risk

|

$2,523.21

|

$2,826

|

$3,165

|

$3,544

|

|

Fine Arts Service levy

|

$1,279.82

|

$1,433

|

$1,605

|

$1,798

|

|

Group Personal Accident

|

$714.53

|

$800

|

$896

|

$1,003

|

|

Forestry

|

$3,391.91

|

$3,798

|

$4,254

|

$4,765

|

|

New Contract Works Policy – Foxton

Pool

|

$21,457.44

|

$24,032

|

$26,916

|

$30,146

|

|

Totals

|

$1,373,664

|

$1,544,567

|

$1,737,869

|

$1,946,413

|

|

LAPP Insurance below ground assets only

|

$453,005.83

|

|

|

|

|

Note: Bridges &

Roads not covered. IT Assets not Insured. Brokers Fees $22,830.88

|

Claims 2018 – 2022

Since

2018 HDC has made claims for $45k for motor vehicles including windscreens.

Subsequently in June 2022 HDC submitted a claim for $52,659 for the Tornado

event, as per our deductible agreement ($10,000) in our MD&BI Policy

$42,659 was paid out.

No

other claims were made against any other of our existing policies during that

period. There are several examples where we have looked to settle

disputes/claims early voiding our ability to enact our insurance policies.

Broker Engagement

Our

relationship with our Insurance Broker has been strong in recent years, and

they have been helpful in our renewal process when making insurance decisions.

However, they have influenced HDCs decisions on policies and risk through

exposure to global and national events that are not always related risks

associated to the Horowhenua District. Equally our decisions are influenced by

decisions and directions that the MWLASS take which encompasses risks other

councils in the region are assessing, which doesn’t always reflect the

uniqueness of hazards and risks that are specific to our district. As part of

our annual renewal and decision making process it is important that all the

facts are available for ensuring decision relating to our insurance coverage is

accurate and appropriate. Therefore, as part of the annual renewal process we

will continue to review the accuracy of registers, upgrade the loss mapping and

undertake complete risk assessments.

Renewal Review Approach –

Modelling of Risk 2023/24

As

indicated above in T.1 & T.2 we have until early July to review and submit

our Renewals Declaration to our Insurance brokers AON, whilst we attempt to

enhance existing information for the renewal process, this is insufficient time

to design and agree an Insurance Strategy that directs HDCs intentions for

assessing and managing risks associated with our assets, coverage and

liabilities long term. For this reason the Insurance Renewal Working Group has

targeted “low hanging fruit” by focusing our initial review on key renewal

declaration components that will provide the Executive and Council with a level

of confidence that we are taking adequate steps towards accurate and cost

effective coverage outcomes.

The

eight areas we have committed to for 2023-24 renewal submission include.

1. Providing

an accurate Asset Register – The team including a short-term

resource to assist’ have been working hard to update the register to

ensure the register is a true reflection of what assets we have, the year they

were built, construction materials used and their location. Location is

ultimately important when mapping the risks associated to the asset specific to

the hazards in our region i.e. Liquefaction, Flooding, Fault Lines, and

Tsunami. Equally important is the need to remove assets at the end of their

life i.e. the old existing Waitarere Surf Club isn’t worth insuring with

the new development underway; or wouldn’t be rebuilt if destroyed; or the

state of depreciation within the organisation. It is important to understand if

our Asset Register is 100% accurate on all important information required for

renewal they will have significantly improved on past years provided a solid

foundation to work from. Also note that as part of the Insurance Strategy

business rules will need to be developed to ensure that asset registers remain

current and accurate at all times.

Currently

we provide a number of community groups including Marae’s and Rural

Community Halls etc support by allowing their insurance requirements to be a

part of the HDC Policies, the main reason for this is to provide a better value

(Cheaper) policy through our premiums and valuations. This does expose HDC and

the community risks if they provide inaccurate declarations or valuations.

2. Asset

Coverage – Timeframes for the Asset Register to be at

a reasonable standard for this year’s renewal submission is to be

completed by 31 May 2023. This will allow time for Group Managers and Managers

aligned to assets to assess the need or option of each asset to be covered or

not i.e. if an asset was destroyed or partially destroyed we wouldn’t

replace it. This assessment would include looking at updated loss mapping

information and risk profiling to identify the type of risk the asset is

exposed to, the likelihood and the impacts associated with the risk.

Motor vehicles Insurance

is generally where we make the majority of our claims, additions and deletions

on the asset register and renewal schedules is important, as is ensuring

current market values are accurate.

3. Valuations

-

Overstated values consequently cause an organisation to carry more insurance

than necessary and pay excessive premiums. On the other hand, an even worse

scenario is an organisation with understated values. Even though a company

would likely be paying less for premiums, the financial impact could be

devastating if that company suffers a loss.

Best

practice is to have big tick assets revalued annually, due to the tight

timeframes of the renewal process and reliance on an accurate asset register

there is no practical time to engage a valuer to update our asset value for

2023. For that reason we will use the 2022 valuations (which realised the

impacts of inflation and supply as our values increased by 44%. The necessity

for applying relevant percentage uplifts if no recent insurance valuations have

been completed, below (T.6) is an indication of percentages which can be

applied to various assets for renewal purposes. Aon Valuations have compiled

this, taking into consideration the current inflation rate, costs of building

products and services as well as the length of time it is taking to obtain both

of these; as well as utilising the Statistics New Zealand information.

T6. Valuation reset percentages for 2023

|

Asset

Type

|

12 months

|

|

Dwelling

Units

|

12.96%

|

|

Commercial

Buildings

|

10.49%

|

|

Factories,

industrial, and storage buildings

|

10.09%

|

|

Hotels,

motels, boarding houses, and prisons

|

9.44%

|

|

Systems

for Water and Sewerage

|

15.02%

|

|

Land

Improvements - Irrigation and Land Drainage

|

20.33%

|

|

Land

Improvements - Reclamation, Slope Stabilisation and River Control

|

5.92%

|

4. Deductibles

– Currently

HDC applies the lowest deductible in the Region set at $10,000 per

event or claim. Councils such as Whanganui have deductibles that range from

$25k to $100k, Horizons Regional Council up to $200k. A number of councils in

other regions have set deductibles at $3-400k depending on the risk profiling.

We have asked AON to provide a schedule that provides indicative savings should

we apply a different level of deductible.

5. Loss

Mapping & Risk Profiling – Insurers look

favourably on organisations when evaluating a submission who have under taken

comprehensive Loss Modelling Programme. Such modelling would include an

increased focus on improved underwriting information i.e. Construction,

Occupancy, Protection and Exposure (COPE - risk

characteristics an underwriter reviews when evaluating a submission for

property insurance). Risk profiling our assets looking at their location

against the hazards associated with that area is important. For that reason the

Insurance renewal team are loading the location of our assets onto our

Geographic Information System (GIS) and overlapping and integrating the

information with our existing Hazard Mapping i.e. Liquefaction, Flood Areas,

Fault Lines, Coastal movement etc. Whilst this information is limited it does

give us a significantly improved overview of the risks associated with each

asset.

As part of the Insurance

Renewal Strategy we will be looking to enhance our mapping data and information

as it is important for HDC when establishing other strategic decisions such as future

growth and developments, locating and upgrading infrastructure, consenting and

managing risk.

To support the mapping the

risk profiling also needs to include research of the risks associated with

natural hazard for the Horowhenua District against other councils in New

Zealand and the region, this research includes:

a. Historical local

natural hazard events, the damage caused and the cost of recovery?

b. The geographical

layout of our terrain – most of our district is fortunate to be made of a

natural flood plain that sees water recede quickly or flow naturally to the

coast line.

c. Where fault line

sit and the activity experienced in the past and more recently.

d. Coastal erosion,

the rate it is eroding, the impacts on our assets and infrastructure over the

year associated with the year of renewal and for outlying years. – A big

part of the coast in the Horowhenua district is moving in the opposite

direction and has an accreting shoreline.

e. Understanding how

good our resilience is in recovering from an event/disaster i.e. Emergency

response and planning and or access to resources during and post an event or

disaster?

f. Understanding

our risk appetite to extent the risk we take when transferring risk to

insurers, this balanced with the impacts of inflation and the cost of living

crisis much of the country is experiencing at the moment. Whilst we can provide

the greatest risk assessment possible there will be an increase in the risk we

take in reducing coverage in certain ways.

For the 2023 renewal we

will be better informed from loss mapping when looking at the deductible level

for this year, assessing the adequate level of coverage

6. Cyber

Insurance Risk Assessment - Identifying and

addressing data risks, including costs, litigation, mitigation and loss of

reputation. Currently HDC Cyber security is spread across a number of different

platforms making it difficult to understand our risk exposure with layered

levels of visibility.

Currently the Information

Services Manager and Risk Manager are reviewing our risk exposure, assessing

our current security platforms assurance effectiveness and consolidation of

costs associated with maintaining our Cyber security. This review includes

looking at a best practice framework that provides a governance based approach;

and in one platform for ease of reporting on progress and Cyber vitality; and

external assurance/assessment that addresses People, Process and Tech controls;

and produces an Improvement plan that gives your Cyber program structure and

reporting to present to your Executives and RAC; and tracks progress on

the plan and assist with assessments on our 3rd party suppliers; and

importantly the platform is measured against a number of International Security

Standards i.e. ISO27001 & NIST, providing ongoing assessment of our

organisations security against the standards highlighting and gaps or risks.

Having this framework will provide leverage with our underwriters and reduce

premiums associated with transferring our risk to Insurance Policies. This will

come into effect for our 2024-25 renewals submission.

Our Information Services

Manager is currently completing the Cyber Liability Assessment for our renewal

submission for 2023-24. The Risk Manager will be undertaking a Cyber Security

Audit with the Information Services Team in July 2023.

7. Policy

Layer Extensions – In recent years HDC through the MWLASS has

elected to take extensions on its Material Damage & Business Interruption

and Public Liability & Professional Indemnity Policies. The intent behind

extending our policies have been basically the increase in asset values coupled

with increased significant weather events. The drive to add additional layers

has also been heightened by the Insurance Brokers pressure on existing

influences. Policy Layer Extensions need to be assessed against risks each

council are faced with which fits outside the LASS approach. A good example is

the damage to the 3 Council’s (Hastings, Napier & Hawkes Bay

Regional) property as a result of Cyclone Gabrielle (Considered significant)

has claims being assessed around the $100M mark. This sits $50m below the first

MD&BI Policy layer with no extension layer needed. The risks associated

with the 3 Councils and their location on the East Coast of New Zealand are far

greater than the Horowhenua, both with flooding, Tsunami and earthquakes.

Three councils within the

MWLASS have declined the additional layer of coverage. Removing the MD&BI

Excess Layer for 2023/24 will save on premium increase projections.

Secondly the two extensions

on Public Liability & Professional Indemnity were taken out with the

reduction from Insurers in the level of coverage they were willing to

underwrite to $15M. Again this was a decision made by LASS looking to extend

the coverage to a higher level in transferring the risk of large scale claims

against councils. Again this decision was made with considering the exposure of

risk each council was exposed to. Areas that need to be assessed include any

large scale subdivisions, projects that are built in natural hazard areas or

have the potential to consenting liabilities attached to them i.e. Okarito Ave

Sub Division. We also need to considerer that New Zealand has The Accident

Compensation Commission (ACC) which does cover injury in a workplace and

prevents organisations from being sued for workplace accidents. Public

Liability is required to cover property, death or injury in circumstances not

covered by ACC, however the $15m liability coverage is adequate based on

historical claim experience.

Equally with Professional

Indemnity it is important as an organisation at times we will make mistakes in

the course of our service delivery, most common in Local Government is with the

Building Consent process. Coverage is necessary as we need to accept mistakes

are inevitable and that we need to transfer a level of liability risk to

insurers. There are two areas we need to consider moving forward, one is

setting business rules that provide a direction on how we deal with complaints

that could potentially end up in liability claims ensuring that we use our

Indemnity Insurance Coverage wisely before determining resolution. Secondly we

need to consider historical information relating to liability claims against

Councils in New Zealand in determining examples of risk and the levels of risk

we are exposed to i.e. Bella Vista Subdivision and the MBIE Investigation

finding against Tauranga City Council for 21 unsafe homes. It is estimated this

will cost insurers approximately $14M. Also worth noting is that most Professional

Indemnity policies exclude coverage for weathertightness (leaky Home) claims.

AON agreed that HDC was in

a better position than other councils to remove any Excess layer Policies given

our lower exposure to risks associated with PL&PI, however we should review

this annually based on level of growth activity within the district. Removing

the two PL&PI Extension Policies will save on premium projections.

T7. Policy Layer Extension

Example

|

MDBI Change in Values

|

Extension layer on kicks in when primary layer is

exhausted

|

|

|

|

|

2019 TDV

|

2022 TDV

|

Change

|

Example loss

|

share of $150M

|

Share of Excess Layer $150m

|

Total Received

|

Shortfall

|

|

|

Horizons

|

$94.7M

|

$127M

|

$32.2M

|

$23,963,718

|

$11,981,859

|

$11,981,859

|

$ 23,963,718

|

$

-

|

|

|

Horowhenua

|

$214M

|

$313.4M

|

$99.4M

|

$59,129,734

|

$29,564,867

|

$29,564,867

|

$59,129,734

|

$

-

|

|

|

Manawatu

|

$173M

|

$228M

|

$55M

|

$42,987,282

|

$21,493,641

|

$

-

|

$21,493,641

|

-$21,493,641

|

|

|

Rangitikei

|

$115M

|

$184M

|

$69M

|

$34,771,288

|

$17,385,644

|

$

-

|

$17,385,644

|

-$17,385,644

|

|

|

Ruapehu

|

$91M

|

$116M

|

$25M

|

$21,917,075

|

$10,958,537

|

$10,958,537

|

$21,917,075

|

$

-

|

|

|

Tararua

|

$115M

|

$146M

|

$31M

|

$27,487,475

|

$13,743,737

|

$13,743,737

|

$27,487,475

|

$

-

|

|

|

Whanganui

|

$335M

|

$476M

|

$141M

|

$89,743,428

|

44,871,714

|

$44,871,714

|

$89,743,428

|

$

-

|

|

|

Total

|

$1.1B

|

$1,595B

|

$452M

|

$300,000,000

|

$150,000,000

|

$111,120,715

|

$261,120,715

|

-$38,879,285

|

|

|

|

|

|

|

|

|

|

|

|

|

8. Self-Insurance

- The

portion of risk not transferred to the insurance market should not be ignored

(this is non-insurance) but managed as a budgeted expense item. This means any

damage or loss should be investigated, costed and set against the budget in

much the same way that an insurance company would process claims. HDC already

has a deductible level of $10,000 on its policies, this sees a number of our

assets repairs, replacements as part of our budgeted operating expenditure, and

this is evident from the zero claims made against our assets in the last 3

years.

As a note HDCs

administration of a self-insurance programme should include identification and

separate accounting treatment of opportunistic upgrading – taking

advantage of an accident to make improvements – so that a proper record

of self-insured damage costs can be maintained. If such losses are allowed to

disappear among other operating costs, various inefficiencies will creep into

risk handling programmes and continuing review of whether to retain or transfer

risks will be compromised. The cost of risks can be carried as a charge against

operating budgets if they are small to medium losses that are an inevitable,

regular expense. Provided such losses can be identified and quantified, then

their costs can be budgeted; they may range from accidental damage to vehicles

to pilfering or damage to office equipment.

9. Other

opportunities

a. Skinning vehicles,

whilst our branding is important skinning a vehicle costs us approximately $5k

per vehicle and increases the value of the coverage or claim. This may be an

opportunity to reduce our expenditure on our vehicles and overvaluing claims.

b. Remove windscreen

coverage as this immediately impacts renewals in the following year by the

dollar value claimed and another 20%. This is managed holistically through

MWLASS so we are subject to premium increases based on what other councils are

claiming. Any change to this policy would need to be managed through the

MWLASS.

c. Investigate the

opportunity to improve systems such as those used for our Asset Register and

Cyber Assurance Modelling.

d. Provide business

rules that influence the way we as an organisation deal with Complaints that

could potentially lead to claims. As an Organisation that is judged on its

service delivery including prompt resolution, too often we are seeking to

rectify or assess the context that sits behind the issue, risk assessment,

liability, or the risk we have transferred by Insurance Policy coverage.

Insurance Strategy & Workplan

2023 - 25

As

indicated earlier, organisationally we need to distinguish ourselves to

insurers by providing accuracy and long term planning that determine the

quality of our renewal submissions, this will require a programme redesign

driven by an Insurance Strategy. The strategy will be the vehicle that

outlines our direction for insurance coverage, enabling HDC to consistently

provide our annual renewal submission with a high level of confidence that

Insurance Certificates offer the best value for the business and the community.

Equally the strategy will assist in modelling risk that informs master planning

and the Long Term Plan. As part of the Insurance Strategy and Workplan a set of

business rules need to inform the way we manage our annual renewal submissions

rules would include are not limited to:

a) Ensuring valuations

are updated annually where possible

b) The Risk Register

is maintained as part of an asset managers day to day duties

c) Our Loss Mapping of

Natural Hazards are continuously reviewed and updated with the latest

information or technology, including information from other Government Agencies

i.e. EQC

d) Our Loss Mapping is

updated annually in line with our Asset Register.

e) An organisation

risk assessment is undertaken annually to review risks associated with

deductibles, coverage and climate or environmental trends.

f) Group

and Activity Managers review the Asset Register annually to inform asset

coverage exclusions. Accurately define our coverage, what assets

do we insure and identify assets we no longer need to insure.

g) Investigate the

opportunity to self-insure and recommend Loss Limit options (a

property insurance limit that is less than the total property or asset values

at risk but high enough to cover the total property values actually exposed to

damage in a single loss occurrence). Much like deductibles we accept

some value liability. More extensive loss modelling and Loss Modelling Policies

will be required to determine appropriate limits, this will be captured in the

strategy.

h) Investment in

reducing risks i.e. development of a strategy and Investment plan to reduce

risks associated with natural catastrophes i.e. Fit for purpose flood banks

linked to climate change forecasts and modelling; and using flood and

liquefaction modelling to inform our future growth decisions.

i) If the

opportunity presents itself in reducing annual premiums through the renewal

initiatives, there could possibly be an opportunity to explore the

organisations ability to adopt a Health and Wellbeing Insurance for staff as an

incentive to attract new staff and retain existing staff. Local Government

Agencies find it difficult to compete with the private sector when attracting

new staff or retaining the services of existing skills and expertise. With the

Cost of Living Crisis impacting on our communities at present Health &

Wellbeing Insurance will be seen as a lucrative and popular benefit.

Next Steps

T8. Initial Insurance Renewal Review 2023/24

|

Objective

|

Actions

|

Timeframes

|

|

Insurance Renewal

Working Group

|

Form an Insurance

Renewal Working Group that oversees annual submissions and informs key

decisions for ELT and RAC relating to the management of our Insurance

Policies

|

1 May 2023

|

|

2023 Insurance

Renewal Process

|

As per tables

presented in this document meet objectives in maximizing accuracy of 2023/24

renewals.

|

7 July 2023

|

|

Partnership with

AON

|

Engage AON where

necessary to work through opportunities to improve submission however not to

assess risk.

|

Ongoing

|

|

Valuations

|

Establish

accuracy of values property, vehicles and other coverage lines/assets

|

31 May 2023

|

|

Asset Register

|

Update current

Asset Registers to ensure what is recorded captures accurately new assets,

ownership, disposed assets, value and depreciation status

|

31 May2023

|

|

Define Coverage

|

Assess coverage

limits for assets, define level of coverage measured against level of risk;

Are there identified assets that we can remove from coverage; including the

need for Coverage Extensions.

|

16 June 2023

|

|

Deductibles

|

Assess

opportunity to increase deductibles based on level of risk associated with

each asset and value returns deductible options provided by AON

|

16 June 2023

|

|

Renewal

Submission

|

Present our

Renewal Schedule to AON for 2023-24

|

7 July 2023

|

T9. Initial Insurance Strategy & Workplan

|

Objective

|

Actions

|

Timeframes

|

|

Insurance

Renewal Working Group

|

\Insurance

Renewal Working Group that oversees Strategy and Workplan to ensure it

remains current & valid.

|

Ongoing

|

|

Insurance

Strategy

|

Develop

an Insurance Strategy that outlines our long-term approach to modelling risk,

annual approach to managing annual insurance renewals, long term planning,

master planning

|

Draft

to RAC August 2023

|

|

Workplan

|

Develop

Workplan to support the Strategy document, highlighting deliverables linked

to work-streams and outlining actions required to achieving key deliverables.

|

Draft

RAC August 2023

|

|

Partnership

with AON

|

Engage

Engineer from AON to assist with enhancing Loss Modelling programme and work

stream deliverables.

|

Ongoing

|

Attachments

There are no attachments for this

report.

|

Confirmation of statutory

compliance

In accordance with section 76 of the

Local Government Act 2002, this report is approved as:

a. containing sufficient information about the options

and their benefits and costs, bearing in mind the significance of the

decisions; and,

b. is based on adequate knowledge about, and adequate

consideration of, the views and preferences of affected and interested

parties bearing in mind the significance of the decision.

|

Signatories

|

Author(s)

|

Rob Benefield

Risk Manager

|

|

|

Approved by

|

Ashley Huria

Business Performance Manager

|

|

|

|

Jacinta Straker

Group Manager Organisation Performance

|

|

|

|

Monique Davidson

Chief Executive Officer

|

|

|

Risk and Assurance Committee

07 June 2023

|

|

6.6 Risk Management Status Quarterly Report -

June 2023

File No.:

23/350

1. Purpose

1.1 The purpose

of this paper is to report to the Risk and Assurance Committee the risk

landscape, risk management work in progress and to ignite discussion with the

committee about risk.

2. Recommendation

2.1 That Report

23/350 Risk Management Status Quarterly Report - June 2023 be received.

2.2 That this

matter or decision be recognised as not significant in terms of s76 of the

Local Government Act 2002.

2.3 That the Risk

and Assurance Committee endorse the Draft Risk Management Framework.

2.4 That the Risk

and Assurance Committee endorse the Draft Risk Strategy and Workplan.

3. Discussion

3.1 Since

the previous report a significant amount of work has been completed. There are

a number of attachments to this report;

· Draft Risk

Management Framework – has been amended following feedback and attached

for endorsement prior to being taken to a Council meeting for adoption.

· Draft Risk

Strategy and Workplan – has been amended following feedback attached for

endorsement prior to being taken to a Council meeting for adoption.

· Risk Report and

Workplan Update – provides an update on progress since March

· Organisation Risk

Register – an up to date register of key risks

· Operational Risk

Register - an up to date register of key risks

· Draft Risk

Appetite Framework – this is in draft and has been amended following

feedback from a Council workshop. It has been attached to show progress made

and for feedback before going back to Council.

3.2 The

above attachments are important pieces of work submitted to the RAC for your

perusal. The first two documents, The Draft Risk Management Framework and the

Risk Strategy and Workplan are resubmitted seeking endorsement from the RAC so

they can be submitted to Council for adoption. The organisation and Operation

Risk Registers are for your information in providing context and insight to the

mitigation of the top risks identified in the Risk Report. The draft Risk

Appetite framework is included in the report to give you an insight to the

direction we are taking in forming the risk appetite, this is important as we

signal the shift away from existing risk appetite framework. This is an

opportunity for the RAC to understand key frameworks and discuss the content.

Attachments

|

No.

|

Title

|

Page

|

|

a⇩

|

Risk Assurance Quarterly Report

2023 - March-May 2023

|

155

|

|

b⇩

|

Horowhenua District Council - Risk

Management Framework Rev 1.7 Draft

|

166

|

|

c⇩

|

Horowhenua District Council - Risk

Strategy & Workplan 2023 Rev 1.7 Draft

|

191

|

|

d⇩

|

Operational Risk Register May 2023

Updated 10 (Under Separate Cover) - Confidential

|

|

|

e⇩

|

Organisation Risk Register May 2023

Updated 10 (Under Separate Cover) - Confidential

|

|

|

f⇩

|

DRAFT Risk Appetite Framework 2023-24

V3

|

203

|

|

Confirmation of statutory

compliance

In accordance with section 76 of the

Local Government Act 2002, this report is approved as:

a. containing sufficient information about the options

and their benefits and costs, bearing in mind the significance of the

decisions; and,

b. is based on adequate knowledge about, and adequate

consideration of, the views and preferences of affected and interested

parties bearing in mind the significance of the decision.

|

Signatories

|

Author(s)

|

Rob Benefield

Risk Manager

|

|

|

Approved by

|

Ashley Huria

Business Performance Manager

|

|

|

|

Jacinta Straker

Group Manager Organisation Performance

|

|

|

|

Monique Davidson

Chief Executive Officer

|

|

|

Risk and Assurance Committee

07 June 2023

|

|

|

Risk and Assurance Committee

07 June 2023

|

|

|

Risk and Assurance Committee

07 June 2023

|

|

|

Risk and Assurance Committee

07 June 2023

|

|

|

Risk and Assurance Committee

07 June 2023

|

|

6.7 Internal Audit Work Programme

File No.:

23/339

1. Purpose

1.1 This report

provides the Risk and Assurance Committee with a suggested approach to the

internal audit work programme.

2. Recommendation

2.1 That Report

23/339 Internal Audit Work Programme be received.

2.2 That this

matter or decision be recognised as not significant in terms of s76 of the

Local Government Act 2002.

2.3 That Risk and

Assurance Committee endorse utilising the $51,000 budgeted for internal audit

to assist with fixing known areas for improvements such as Fringe Benefit Tax,

Business Continuity Programme, Cyber Security and Financial Policies during the

2023/24 financial year.

3. Issues for Considerations

3.1 The role of

Internal Audit is to assist with the identification of measures to achieve

greater effectiveness, efficiency and economy and to remedy practices that

expose the organisation to risk and vulnerability. It brings a systematic and

disciplined approach to evaluating and improving the effectiveness of risk

management in the organisation.

3.2 Last

financial year, the internal audit budget was allocated towards conducting

audits on various areas. These audits were focused on procurement processes and

internal policies. PricewaterhouseCoopers were also engaged to conduct a

comprehensive review specifically pertaining to PAYE and GST.

3.3 There is

currently $51,000 budgeted for internal audit for the financial year 23/24.

3.4 Officers are

proposing that these funds are utilised this financial year to assist fixing

known areas for improvement such as;

(a) Fringe Benefit Tax – Standard

internal audit tax programme – an audit to ascertain that we are accurate

in declaring and recording fringe benefits that require fringe benefit tax.

(b) Business Continuity Programme

– complete a gap analysis to identify areas for improvement supported by

a workplan.

(c) Cyber Security –

complete an analysis to gain an improved organisation visibility to cyber

security to understand whether our platform is still fit for purpose and meets

national standards.

(d) Financial Policy Reviews

– such as Corporate Debt Management, Credit Card Usage, Cash Handling

Policy, Staff Private Purchasing Policy, Travel Policy –updating policies

to ensure they align with current best practices and standards to incorporate

the most up-to-date guidelines and recommendations.

3.5 Using

available budget to improve business areas and implement solutions instead of

solely focusing on identifying further areas offers several benefits:

(a) Proactive Approach: By

allocating the budget for issue resolution, we adopt a proactive approach to

problem-solving. Instead of looking for further issues, we address the ones we

are already aware of. This can help prevent problems from escalating or causing

additional complications.

(b) Continuous Improvement:

Utilising budget for issue resolution encourages a culture of continuous

improvement. It acknowledges that issues are a normal part of any system or

process and uses resources available to resolve them.

(c) Mitigating Risks: Issues can

have a detrimental impact on various aspects of an organisation, including

operations, customer satisfaction, and financial stability. By allocating the

budget for issue resolution, we can mitigate these risks and minimise the

potential negative consequences.

3.6 Overall,

using the budget for issue resolution complements the process of identifying

known issues by creating a proactive approach for problem-solving, fostering

continuous improvement and mitigating risks.

4. Next Steps

4.1 That Risk and

Assurance confirm where the $51,000 for internal audit is to be spent and

officers undertake the work programme.

Attachments

There are no attachments for this

report.

|

Confirmation of statutory

compliance

In accordance with section 76 of the

Local Government Act 2002, this report is approved as:

a. containing sufficient information about the options

and their benefits and costs, bearing in mind the significance of the

decisions; and,

b. is based on adequate knowledge about, and adequate

consideration of, the views and preferences of affected and interested

parties bearing in mind the significance of the decision.

|

Signatories

|

Author(s)

|

Ashley Huria

Business Performance Manager

|

|

|

Approved by

|

Jacinta Straker

Group Manager Organisation Performance

|

|

|

|

Monique Davidson

Chief Executive Officer

|

|

|

Risk and Assurance Committee

07 June 2023

|

|

6.8 Conflict of Interest Report

File No.:

23/332

1. Purpose

1.1 To update the

committee on the Council’s planned approach to recording and managing

conflicts of interest for Horowhenua District Council employees, this report

does not relate to Elected Members conflict of interest.

2. Recommendation

2.1 That Report

23/332 Conflict of Interest Report be received.

2.2 That this

matter or decision be recognised as not significant in terms of s76 of the

Local Government Act 2002.

2.3 That the

committee not the work that the Council is currently undertaking to better

understand and manage conflicts of interest.

3. Background/Previous Council Decisions

3.1 A conflict of

interest register is an important tool for promoting transparency and integrity

in organisations, particularly those in the public sector. The register is

designed to identify potential conflicts of interest that may arise between an

individual's personal or financial interests and their responsibilities while

being employed by council.

3.2 The

importance of having a conflict of interest register can be summarised in the

following points:

Avoiding actual or perceived conflicts of interest: By

maintaining a conflict of interest register, an organisation can identify and

manage potential conflicts before they have the ability to impact the

organisation, thereby avoiding the risk of damage to its reputation or legal

consequences.

Promoting fairness and objectivity: A conflict of interest

register helps to ensure that decisions made by individuals are based on

objective criteria rather than personal interests.

Ensuring compliance with legal and ethical standards: Many

organisations are legally required to have a conflict of interest policy and

register in place. Failure to comply with these requirements can result in

legal sanctions and reputational damage.

Demonstrating accountability and transparency- By reporting

on the conflict of interest register, an organisation can demonstrate its

commitment to transparency and accountability.

3.3 Overall, a

conflict of interest register is an essential tool for promoting transparency,

accountability, and integrity in organisations, particularly those with a

public interest or regulatory function. It helps to ensure that decisions are

made objectively and fairly, and that individuals act in the best interests of

the organisation rather than their own personal interests.

3.4 In September

2022, a thorough review was conducted of our Conflict of Interest Prevention

Policy, encompassing the comprehensive management plan and the declaration

form, which was then adopted by Council. This review process was essential to

ensure the policy remained current, effective, and aligned with industry best

practices. The next review is scheduled for September 2024. Subsequently, in

March 2023 Council appointed a Registrar of Pecuniary Interests, and the

Pecuniary Interests Register where Elected Members declare interests on an

annual basis to be published on the Council website.

4. Discussion

4.1 Horowhenua

District Council currently maintains a register for employees who have declared

any conflicts of interests.

4.2 Within

our processes, there are trigger points however these are inconsistently

applied across the organisation hence we need to increase focus on it and

improve our processes. These trigger points include:

(a) Employment Process: We have

recently strengthened the employment process by incorporating targeted

questions to identify potential conflicts of interest which are then

effectively evaluated and addressed. The intent of this assessment is to allow us

to uncover any circumstances that may show conflicts. In cases where a

potential conflict of interest is identified, we request additional information

to gain a comprehensive understanding of the situation. This assessment allows

us to gauge the potential impact of the conflict on the candidate's ability to

carry out their duties objectively and impartially.

(b) Employee Disclosure: We rely on

staff to proactively declare any conflicts of interest they become aware of,

this is an area where we can improve practice. The importance of employees

proactively disclosing any conflicts of interest they become aware of. This

requirement encompasses conflicts arising from personal relationships,

financial interests, or any other relevant circumstances.

4.3 These

trigger points aim to establish a framework for managing conflicts of interest.

This proactive approach enables us to address conflicts at various stages, from

the initial employment process to ongoing employee engagement.

4.4 However,

in our current practice, only staff members who identify a conflict of interest

are required to complete a conflict of interest form. Moving forward, we

propose a revised approach where all staff members will be required to complete

the form, regardless of whether or not a conflict is present. This adjustment

aims to establish best practices and ensure thorough compliance by

acknowledging that individuals do not have a conflict of interest. The form

will be completed on an annual basis. To implement this revised process, we will

communicate the updated requirement to all staff members and provide clear

instructions on the completion of the conflict of interest form. Regular

reminders will be issued to ensure timely and accurate completion on an annual

basis. By adopting this approach, we strengthen our commitment to upholding the

highest standards of integrity, transparency, and ethical behaviour across the

organisation.

4.5 A

number of conflicts of interests have been disclosed, and there are

corresponding management plans in place. These conflicts encompass various

categories, including whanau/relationship, shareholder involvement in companies

and community service in community organisations that receive Council funding

or support. By identifying these conflicts and establishing management plans,

we have ensured that there are clear plans and control measures in place.

Noting that Council has conflicts with itself, these can be seen in areas such

as consenting processes, where this occurs management plans are put in place

which vary however can include outsourcing of the regulatory process.

4.6 As

well as the HDC Employee conflict of interest form, all staff involved in

projects or engaged in the tendering process are required to complete a

conflict of interest and confidentiality agreement form specific to their

assigned tasks. These forms are reviewed and recorded by their respective

managers. While this process has been in place for a considerable period, there

is an opportunity to enhance it by centralising the information into a

comprehensive register. This register will serve as a repository for collecting

and managing this critical information in a centralised and easily accessible

manner.

5. Next

Steps

5.1 Implementation

of All Staff Completing a Conflict of Interest Form: Moving forward, it will be

mandatory for all staff members to complete the conflict of interest form no

matter if they have a conflict to declare or not. This form will capture any

potential conflicts or confirm the absence of conflicts.

5.2 Biannual

Reporting to the Risk and Assurance Committee: A report will be established to

provide biannual updates to the Risk and Assurance Committee regarding

conflicts of interest. These reports will include an overview of the disclosed

conflicts, actions taken to manage them, and any emerging trends or patterns.

Attachments

|

No.

|

Title

|

Page

|

|

a⇩

|

Conflicts of Interest Prevention

Policy - adopted September 2022

|

230

|

|

Confirmation of statutory

compliance

In accordance with section 76 of the

Local Government Act 2002, this report is approved as:

a. containing sufficient information about the options

and their benefits and costs, bearing in mind the significance of the

decisions; and,

b. is based on adequate knowledge about, and adequate

consideration of, the views and preferences of affected and interested

parties bearing in mind the significance of the decision.

|

Signatories

|

Author(s)