Notice is hereby given that an ordinary meeting of the Horowhenua District Council Risk and

Assurance Committee will be held on:

|

Date:

Time:

Meeting Room:

Venue:

|

Wednesday 30 April

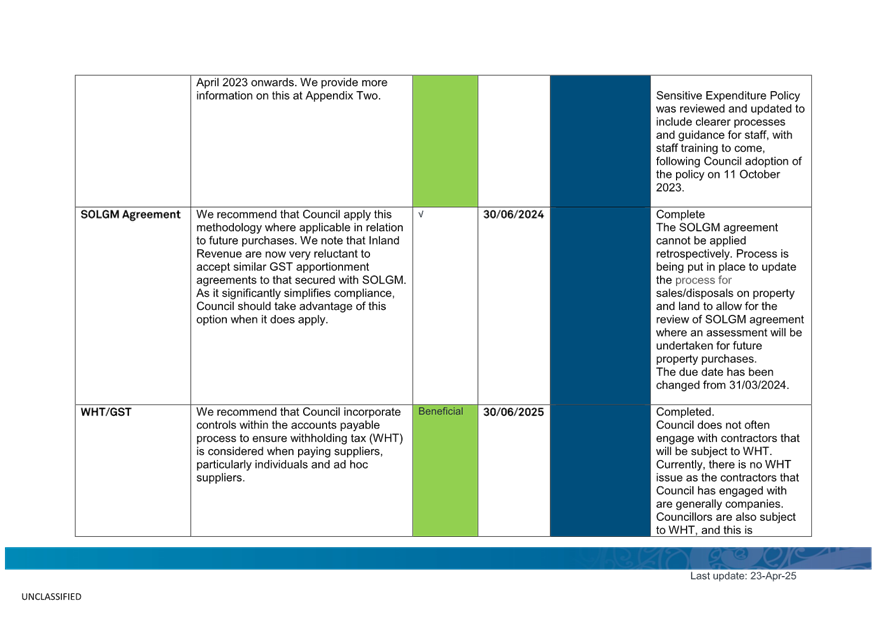

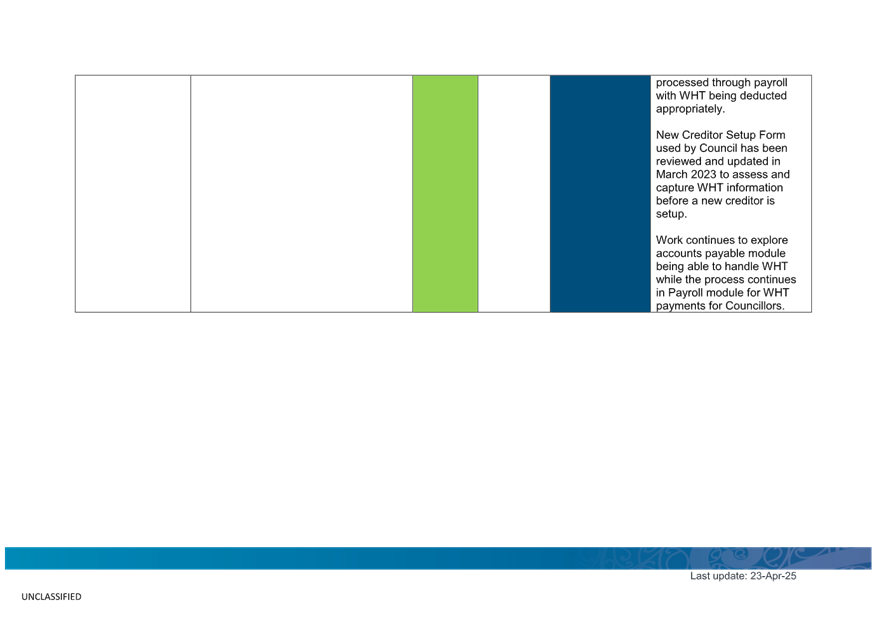

2025

1:00pm

Council

Chambers

126-148 Oxford St

Levin

|

|

Risk and Assurance Committee

OPEN AGENDA

|

MEMBERSHIP

|

Chairperson

|

Cr Sam Jennings

|

|

|

Deputy Chairperson

|

Cr Paul Olsen

|

|

|

Members

|

Cr Alan Young

|

|

|

|

Cr Clint Grimstone

|

|

|

|

Cr Jonathan Procter

|

|

|

|

Mayor Bernie Wanden

|

|

|

|

Jenny Livschitz

|

Independent Member

|

|

|

Sarah Everton

|

Independent Member

|

|

Risk and Assurance Committee

30 April 2025

|

|

ITEM TABLE OF CONTENTS PAGE

KARAKIA TIMATANGA

|

Whakataka te hau

ki te uru

Whakataka te hau

ki te tonga

Kia

mākinakina ki uta

Kia

mātaratara ki tai

E hī ake

ana te atakura

He tio, he huka,

he hau hū

Tīhei mauri

ora!

|

Cease the winds

from the west

Cease the winds

from the south

Let the breeze

blow over the land

Let the breeze

blow over the ocean

Let the

red-tipped dawn come with a sharpened air.

A touch of

frost, a promise of a glorious day.

|

PROCEDURAL

1 Apologies 5

2 Late Items 5

3 Declarations

of Interest 5

4 Confirmation

of Minutes 5

REPORTS

5 Reports

for Noting

5.1 PwC Tax Governance Presentation 7

5.2 Continuous Improvement and

Audit Actions Monitoring Report 21

5.3 Health, Safety and

Wellbeing Dashboard - Quarterly Report 73

5.4 Legislative Compliance 99

5.5 Risk and Assurance

Committee Work Programme 115

5.6 Financial Dashboard as at

31 March 2025 119

5.7 Treasury Update - March

2025 123

C1 Discussion on the Options

for Credit Rating Services

C2 Risk Management Quarterly

Report 135

KARAKIA WHAKAMUTUNGA

|

Kia whakairia te

tapu

Kia wātea

ai te ara

Kia turuki

whakataha ai, kia turuki whakataha ai

Haumi e, hui e,

taiki e!

|

Restrictions are

moved aside

so the pathway

is clear

To return

to everyday activities

Draw together,

affirm!

|

Karakia

1 Apologies

2 Late

Items

To consider, and if thought fit, to pass a resolution to permit the

Council to consider any further items which do not appear on the Agenda of this

meeting and/or the meeting to be held with the public excluded.

Such resolution is required to be made pursuant to Section 46A(7) of

the Local Government Official Information and Meetings Act 1987, and the

Chairperson must advise:

(i) The reason why the

item was not on the Agenda, and

(ii) The reason why the

discussion of this item cannot be delayed until a subsequent meeting.

3 Declarations of Interest

Members are

reminded of their obligation to declare any conflicts of interest they might

have in respect of the items on this Agenda.

4 Confirmation of Minutes

Recommendations

That the

meeting minutes of Risk and Assurance Committee, 26 February 2025 be accepted

as a true and correct record.

That the

meeting minutes of Public Excluded Risk and Assurance Committee, 26 February

2025 be accepted as a true and correct record.

|

Risk and Assurance Committee

30 April 2025

|

|

File No.:

25/203

5.1 PwC

Tax Governance Presentation

|

Author(s)

|

Pei Shan Gan

Financial

Controller | Kaiwhakahaere Tahua Pūtea

|

|

Approved by

|

Jacinta Straker

Group Manager

Organisation Performance | Tumu Rangapū, Tutukinga Whakahaere

|

|

|

Monique Davidson

Chief Executive

Officer | Tumuaki

|

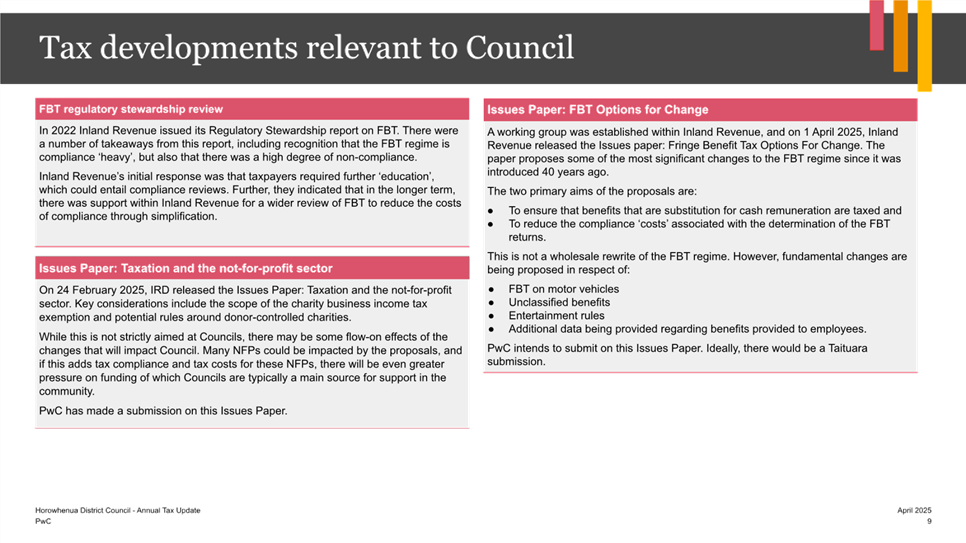

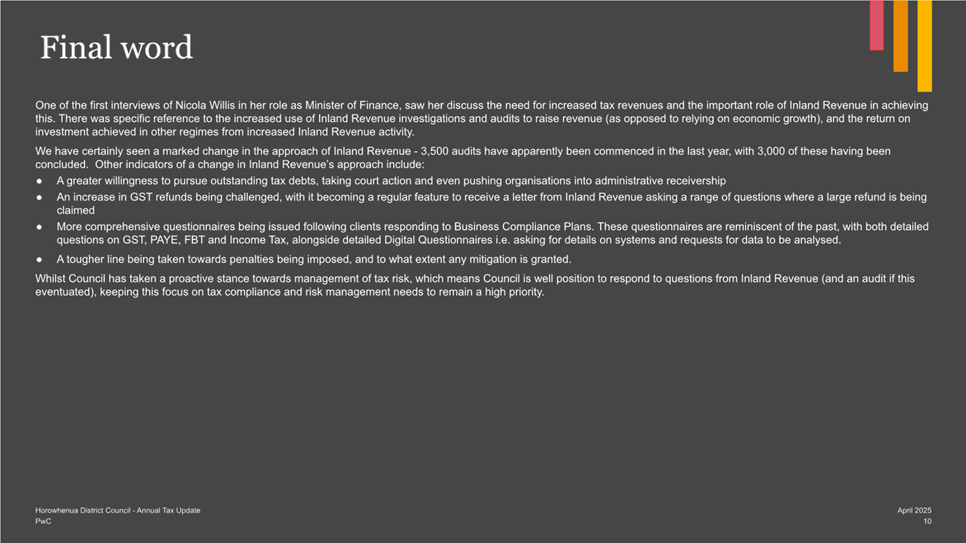

Purpose | TE PŪTAKE

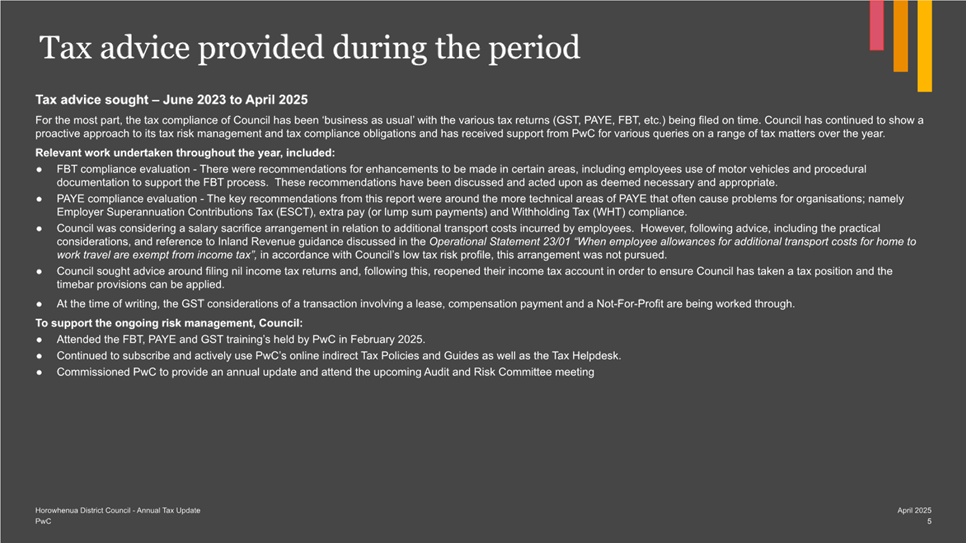

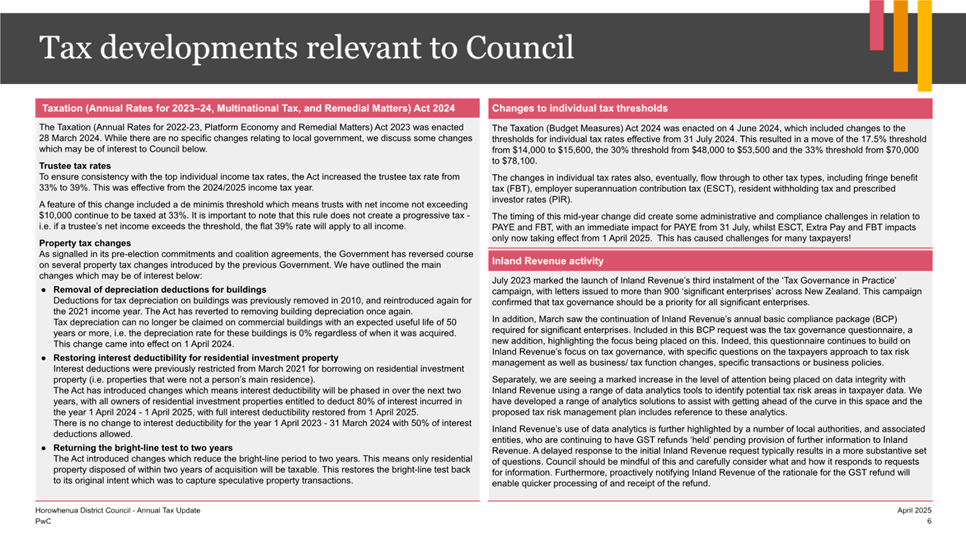

1. This

report presents the Risk and Assurance Committee with the

PricewaterhouseCoopers (PwC) annual tax update for the Horowhenua District

Council, as part of the tax governance framework programme.

2. PwC

will be in attendance to lead the presentation.

This matter

relates to Ensuring Financial Discipline and Management

Ensure financial

discipline and compliance with our financial strategy and benchmarks.

Provide transparent

financial reporting and regular updates to the community on the Council’s

financial performance and initiatives.

RECOMMENDATION | NGĀTAUNAKITANGA

A. That Report 25/203 PwC Tax Governance Presentation be received and

noted.

B. That this matter or decision be recognised as not significant in

terms of s76 of the Local Government Act 2002.

C. That the Committee notes the Annual Tax Update presentation by PwC.

bACKGROUND | hE

KŌRERO TŪĀPAPA

3. Council

has a high public profile and as such, must maintain exemplary governance and

tax compliance standards.

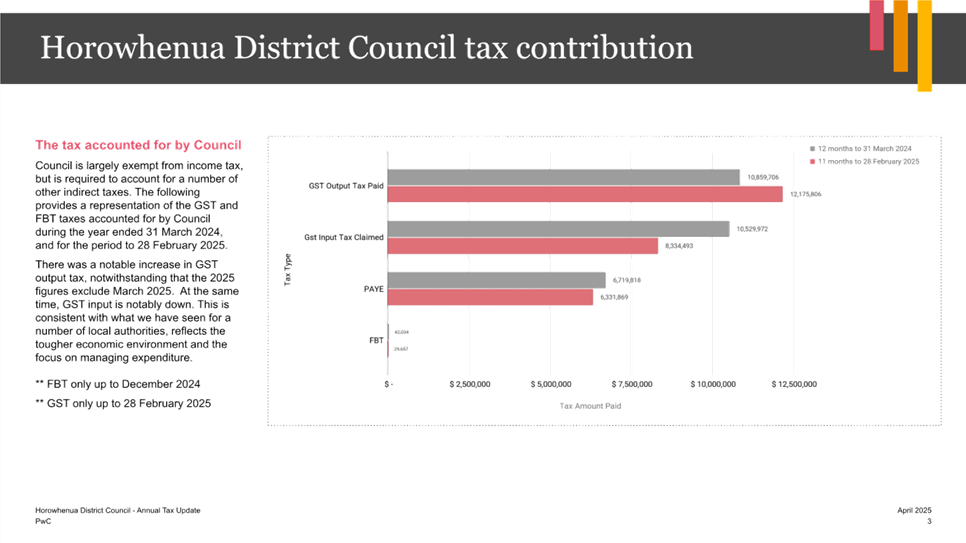

4. Although

Council does not pay corporate income tax, it is required to correctly account

for Goods and Services Tax (GST), Fringe Benefit Tax (FBT), Pay as you Earn

(PAYE) and a range of other withholding taxes.

5. Inland

Revenue Department (IRD) has signalled its expectation that all large

organisations should have tax risk management incorporated within their

governance framework.

6. Council

has an obligation to fulfil its tax compliance obligations as required by tax

legislation, including the Income Tax Act 2007, Goods and Services Tax Act

1985, and Tax Administration Act 1994.

DISCUSSION | HE MATAPAKINGA

7. Proactive

tax risk management can facilitate the mitigation of operational risk,

financial risk and compliance risk. Given the high profile and public nature of

Council, there is a need to adopt a conservative approach towards tax compliance.

Accordingly, Council adopts a “LOW” tax risk profile such that it

has an open and honest working relationship with the IRD through PwC.

8. A

tax risk governance framework was adopted by the Council as a proactive step

towards identifying and managing tax risk to maintain the Council’s low

risk profile. As part of the tax governance framework, PwC have prepared an

annual tax update as a report to this Committee.

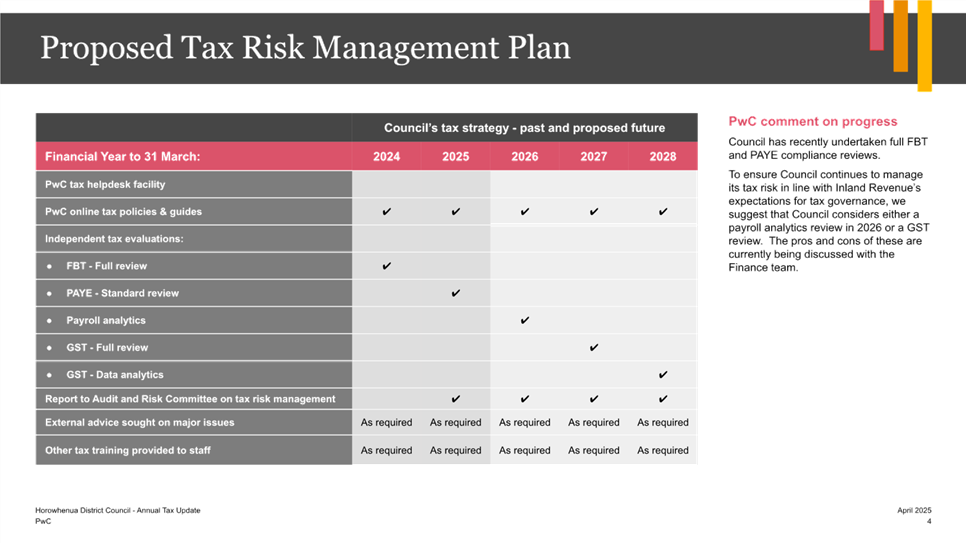

9. Table

below shows Council’s tax compliance evaluation journey:

|

Financial

year

|

Tax

Compliance evaluation completed

|

|

2021/22

|

PAYE

independent tax evaluation

|

|

2022/23

|

GST

independent tax evaluation

|

|

2023/24

|

FBT

independent tax evaluation

|

|

2024/25

|

PAYE

independent tax evaluation

|

10. For

the 2025/26 financial year we are planning an evaluation by PwC on payroll

analytics. Inland Revenue have invested heavily in data analytics, particularly

in relation to KiwiSaver and Employer Superannuation Contribution Tax (ESCT).

Accordingly, PwC have developed data analytic capability that run off the

payday returns (Employment Information) filed. These are comparable to the

tests that PwC understands Inland Revenue are now performing, and can assist

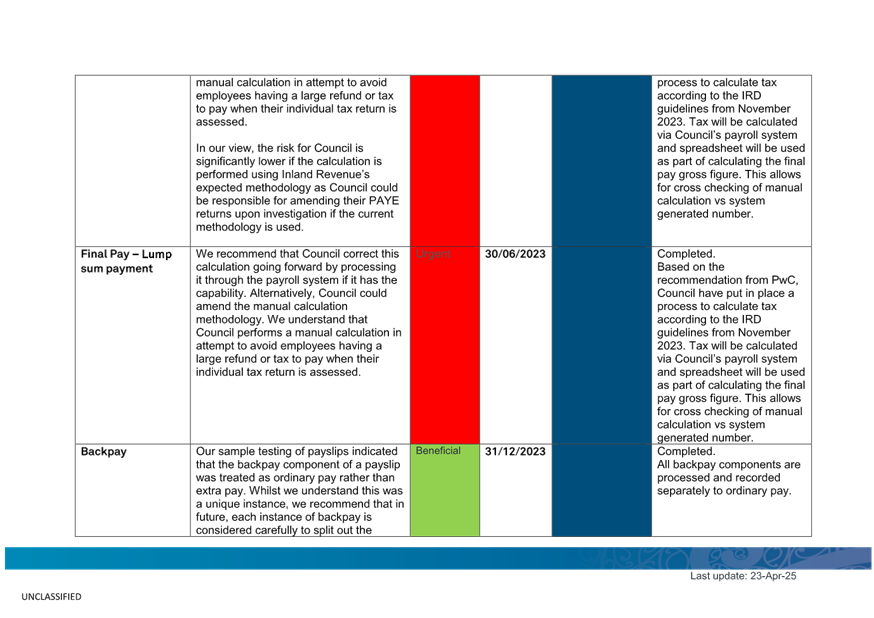

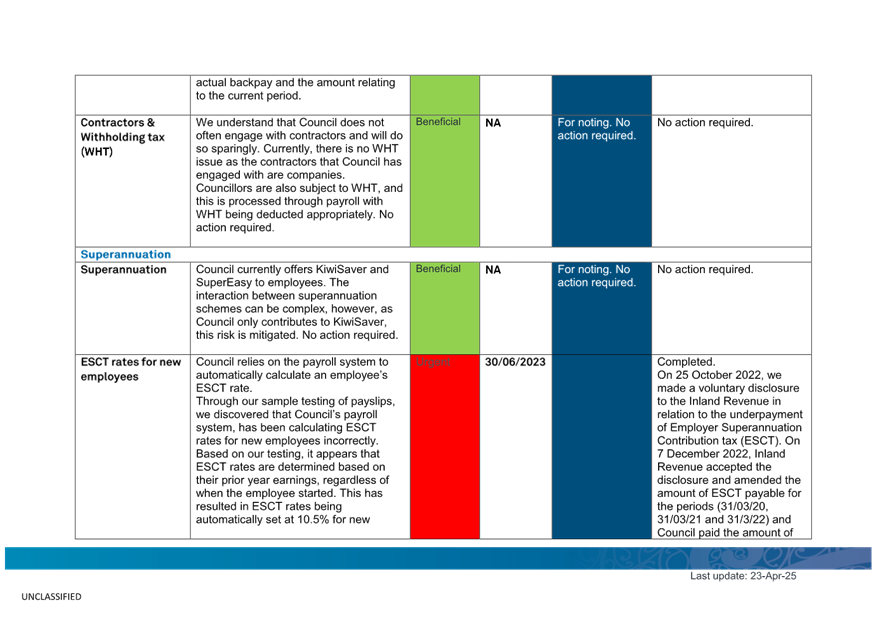

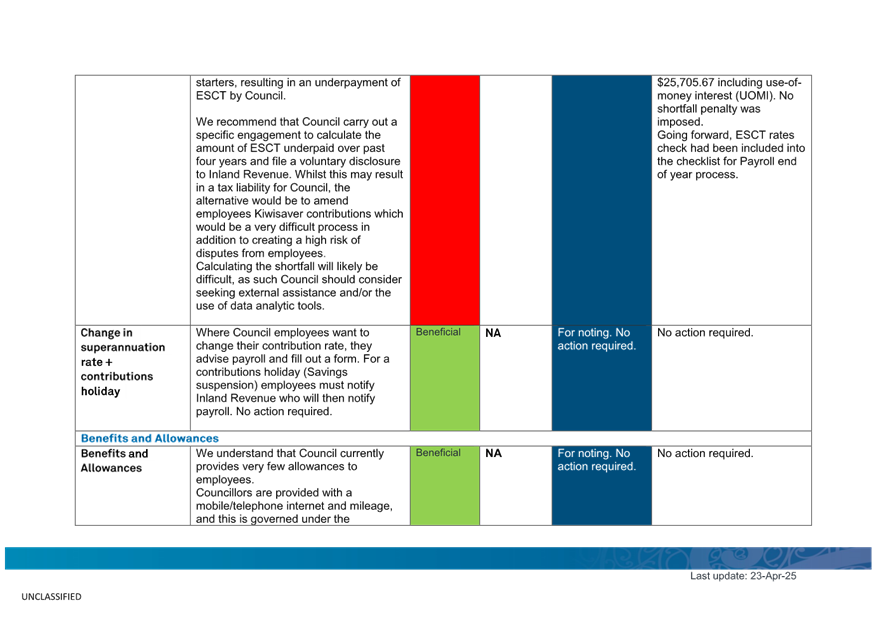

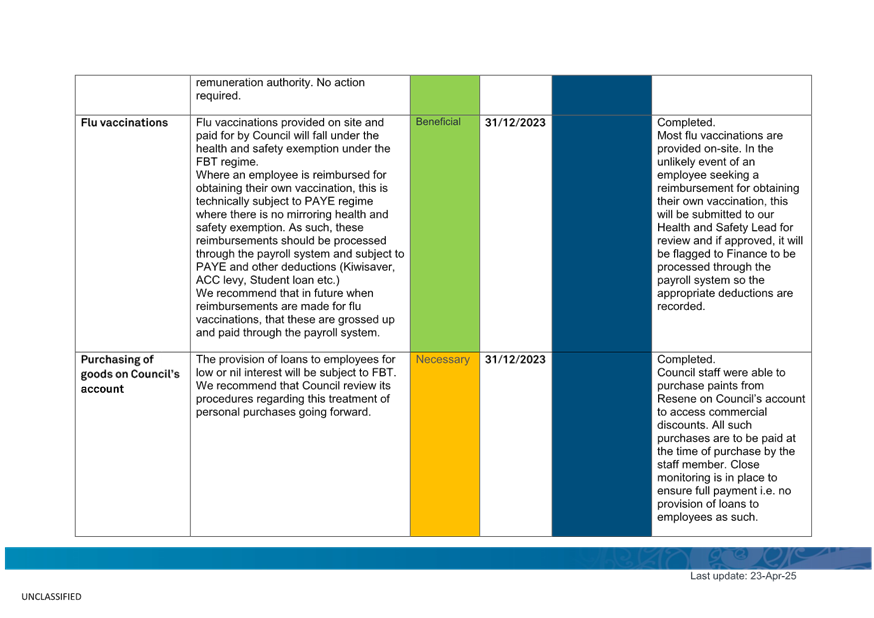

Council in being prepared for any data scrutiny by Inland Revenue.

·

|

Confirmation of statutory compliance

In accordance

with sections 76 – 79 of the Local Government Act 2002, this report is

approved as:

a. containing

sufficient information about the options and their advantages and

disadvantages, bearing in mind the significance of the decisions; and,

b. is

based on adequate knowledge about, and adequate consideration of, the views

and preferences of affected and interested parties bearing in mind the

significance of the decision.

|

Attachments | NGĀ

TĀPIRINGA KŌRERO

|

No.

|

Title

|

Page

|

|

a⇩

|

Horowhenua District Council -

Annual Update - April 2025 by PwC

|

9

|

|

Risk and Assurance Committee

30 April 2025

|

|

|

Risk and Assurance Committee

30 April 2025

|

|

File No.:

25/195

5.2 Continuous

Improvement and Audit Actions Monitoring Report

|

Author(s)

|

Pei Shan Gan

Financial

Controller | Kaiwhakahaere Tahua Pūtea

|

|

Approved by

|

Jacinta Straker

Group Manager

Organisation Performance | Tumu Rangapū, Tutukinga Whakahaere

|

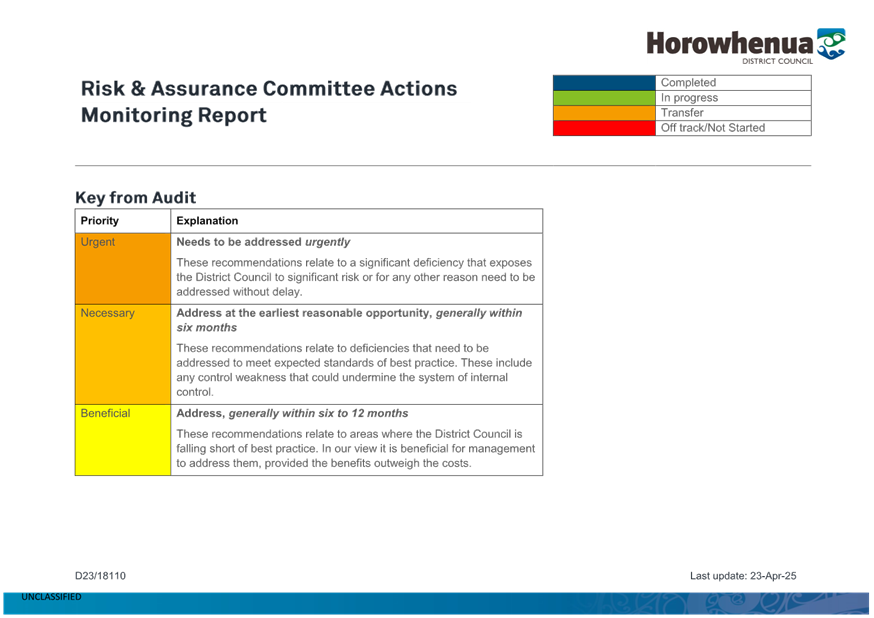

Purpose | TE PŪTAKE

1. This

report updates the Risk and Assurance Committee on progress on the action items

from previous resolutions.

This matter

relates to Pursuing Organisation Excellence

Continuing the

journey of organisational transformation by enabling a culture of service,

excellence and continuous improvement.

RECOMMENDATION | NGĀTAUNAKITANGA

A. That Report 25/195 Continuous Improvement and Audit Actions

Monitoring Report be received and noted.

bACKGROUND | hE

KŌRERO TŪĀPAPA

2. This

paper reports on actions generated from Committee resolutions, and any requests

noted through the minutes, or requested through external and internal audit

work and for actions accepted by the Chair.

3. Much

like the Committee Work Programme, the Continuous Improvement and Audit Actions

Monitoring Report is a standing item, and reported through at each committee

meeting.

4. The

monitoring report includes actions that have been carried over from the Finance,

Audit and Risk Committee from the previous Triennium.

DISCUSSION | HE MATAPAKINGA

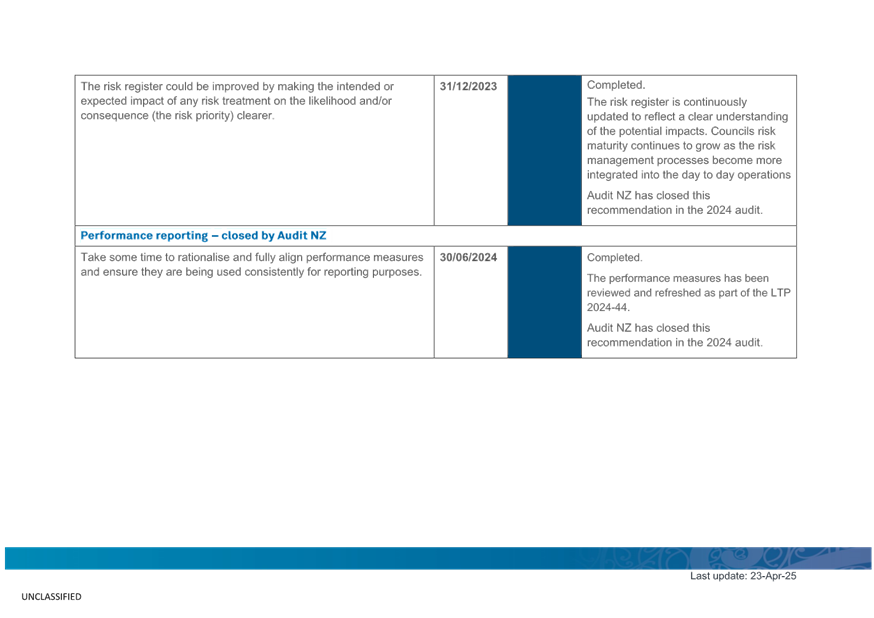

5. Below

is a summary of the status of all recommendations:

|

|

Open recommendations at 1 July 2024

|

Recommendations completed and archived

|

New

|

Recommendations completed

|

Outstanding recommendations

|

|

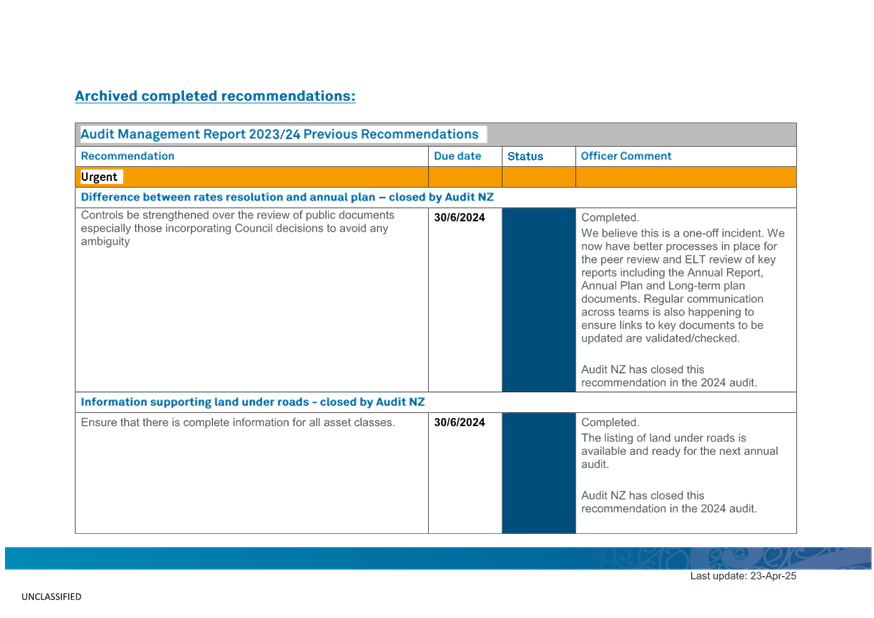

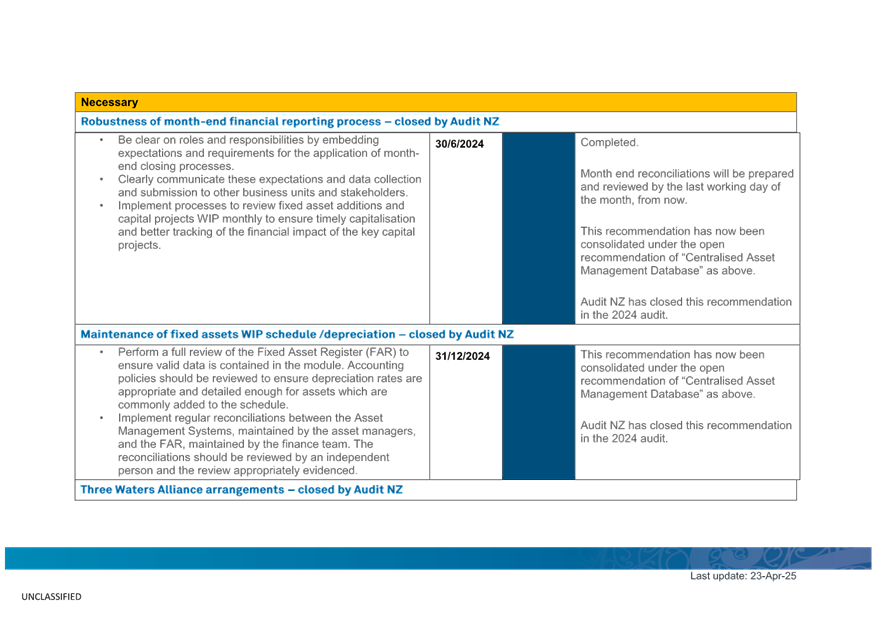

Audit Management report 2023/24 previous

recommendations

|

19

|

(5)

|

4

|

(5)

|

13

|

|

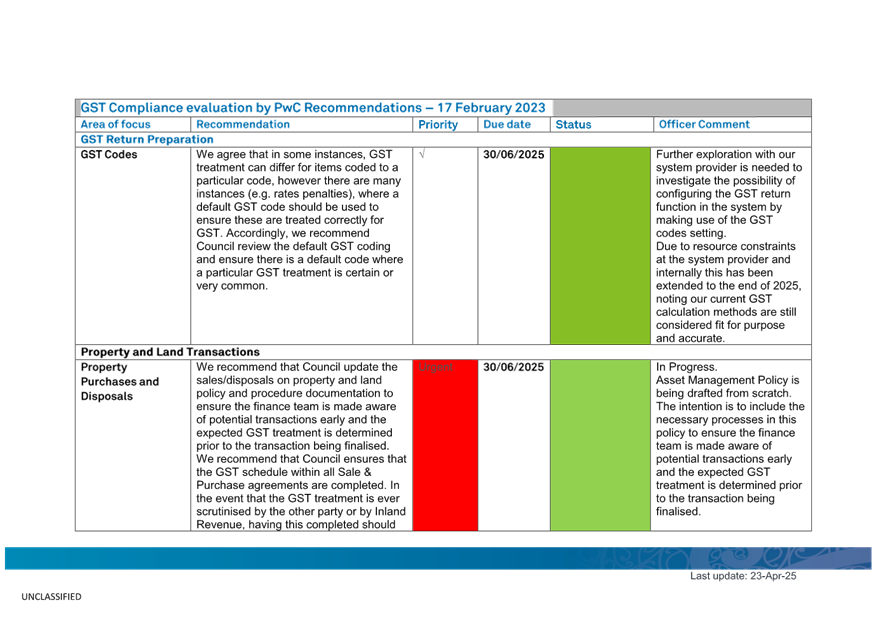

GST Compliance evaluation by PwC recommendations

– 17 February 2023

|

19

|

(16)

|

-

|

-

|

3

|

|

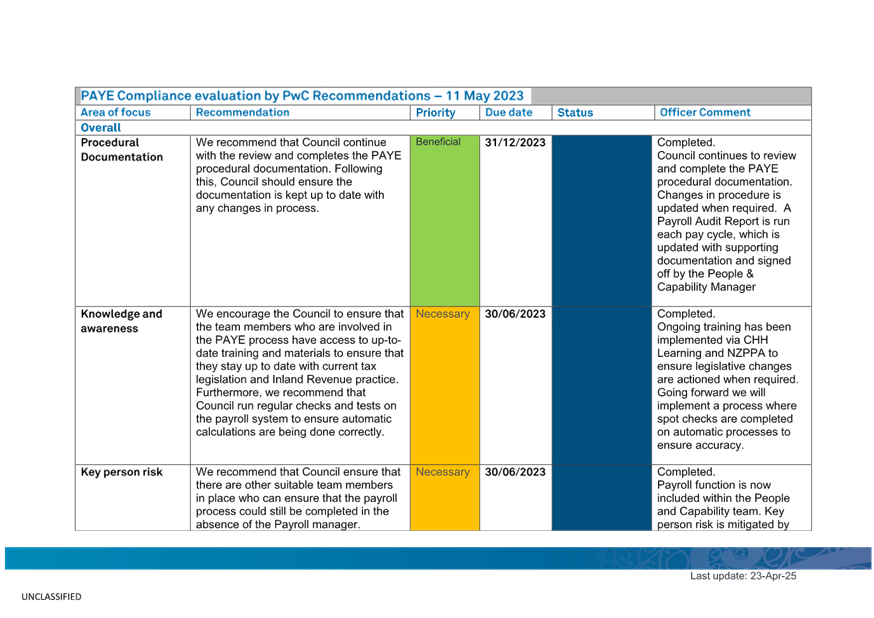

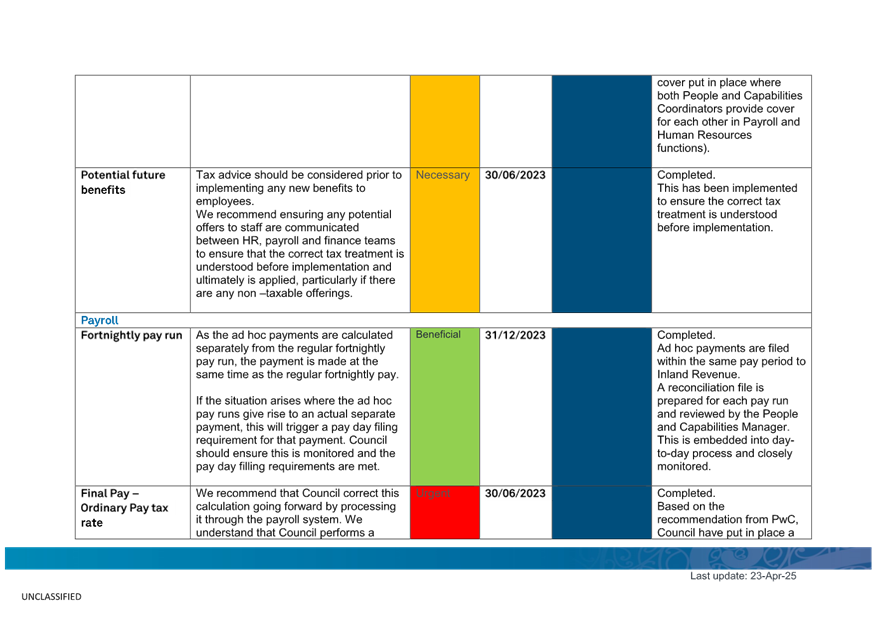

PAYE Compliance evaluation by PwC recommendations

– 11 May 2023

|

18

|

(18)

|

-

|

-

|

-

|

|

FBT Compliance evaluation by PwC recommendations

– June 2024

|

15

|

(11)

|

-

|

-

|

4

|

|

Total

|

71

|

(50)

|

4

|

(5)

|

20

|

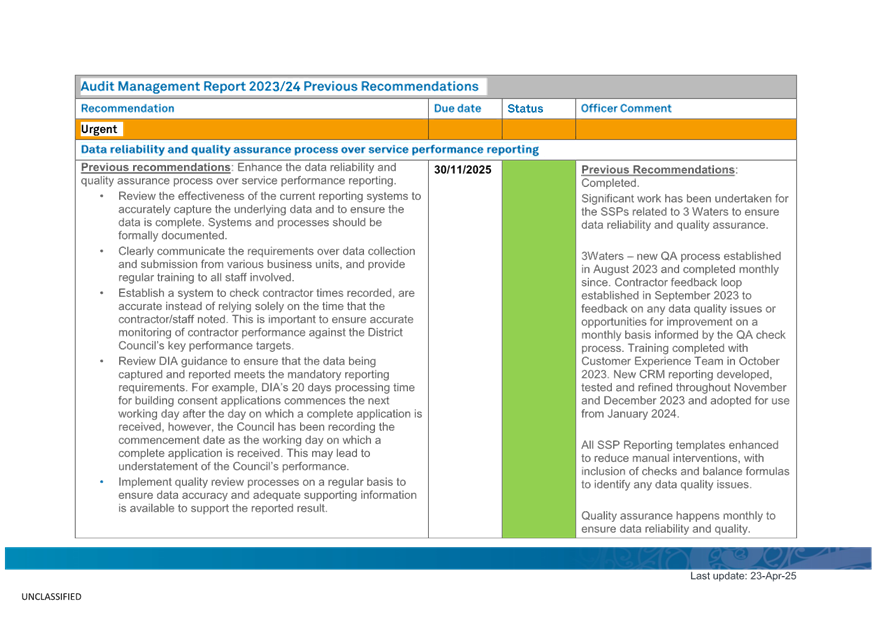

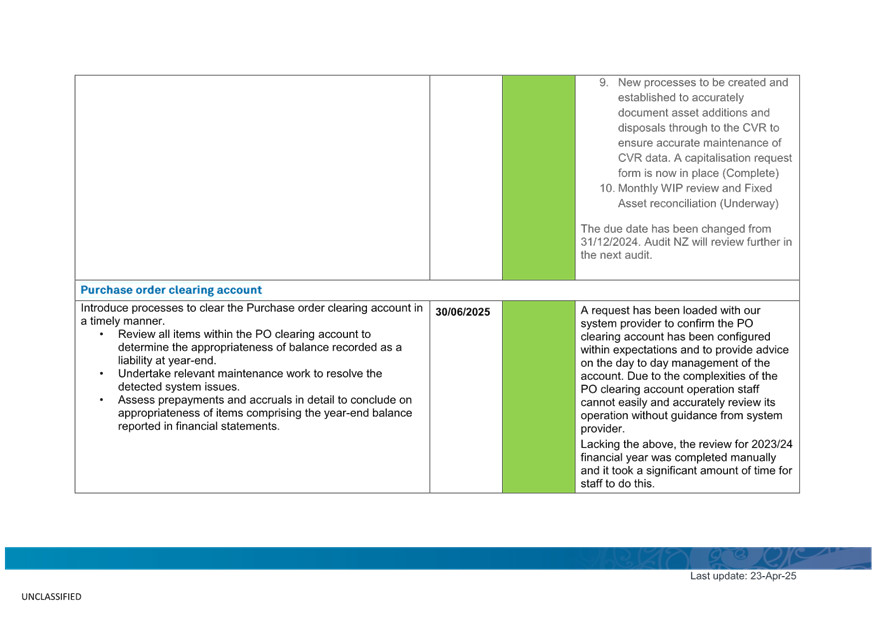

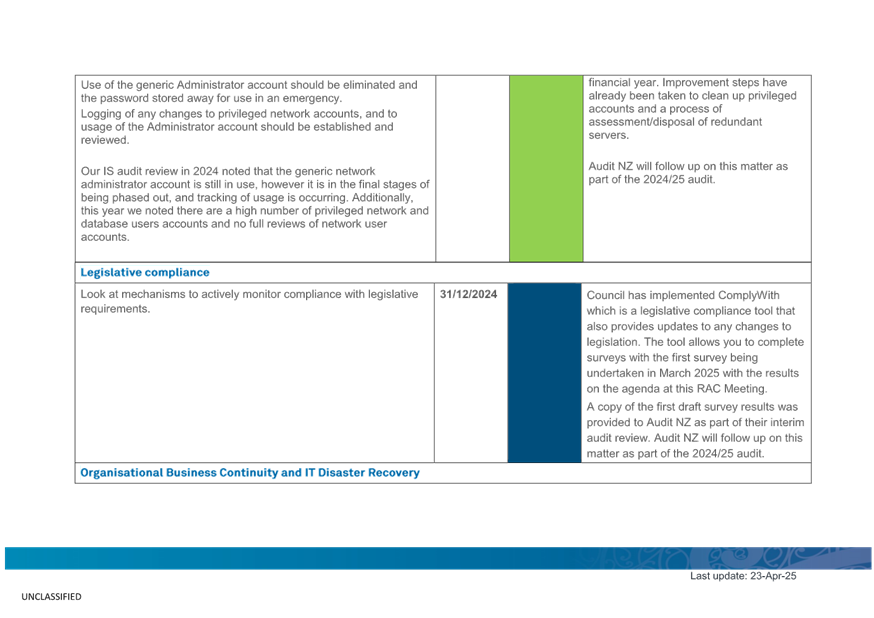

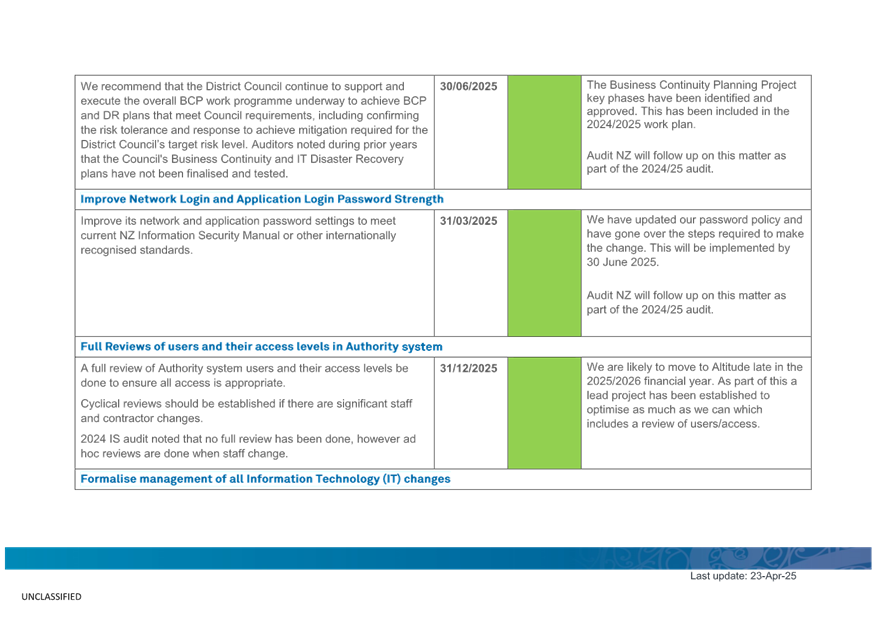

6. There

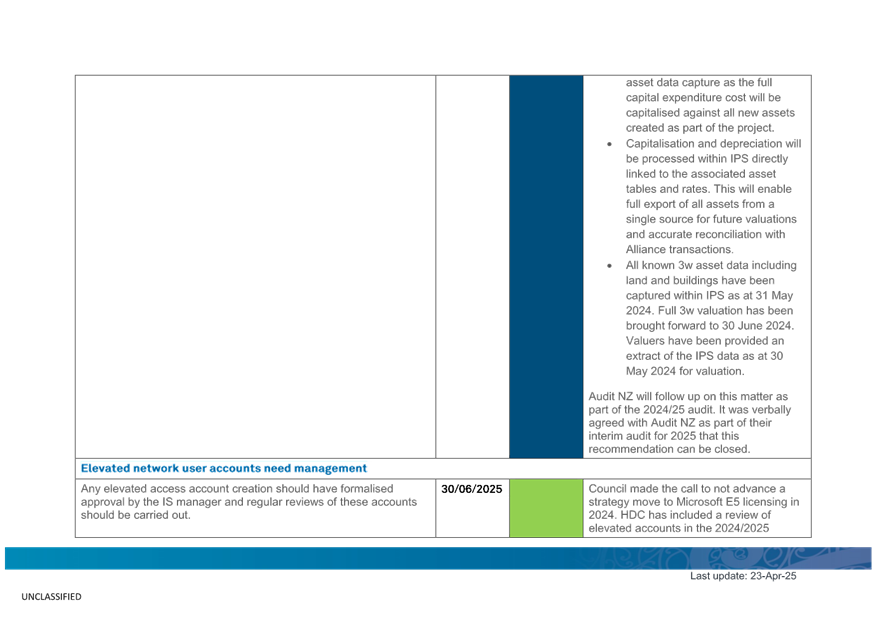

was a total of 18 open recommendations from the Audit Management letter for the

year ended 30 June 2024. There are 13 outstanding recommendations that are

being followed up and worked on. Some will take longer to complete due to

resourcing or system constraints to implement changes or improvements. Some are

also waiting for Audit NZ to finish their assessment during their 2025 annual

audit visit.

7. On

the 9th of April, officers held a meeting with Audit NZ to address

some of the older open recommendations from previous years’ Audit

Management letters. Officers have since provided more supporting information to

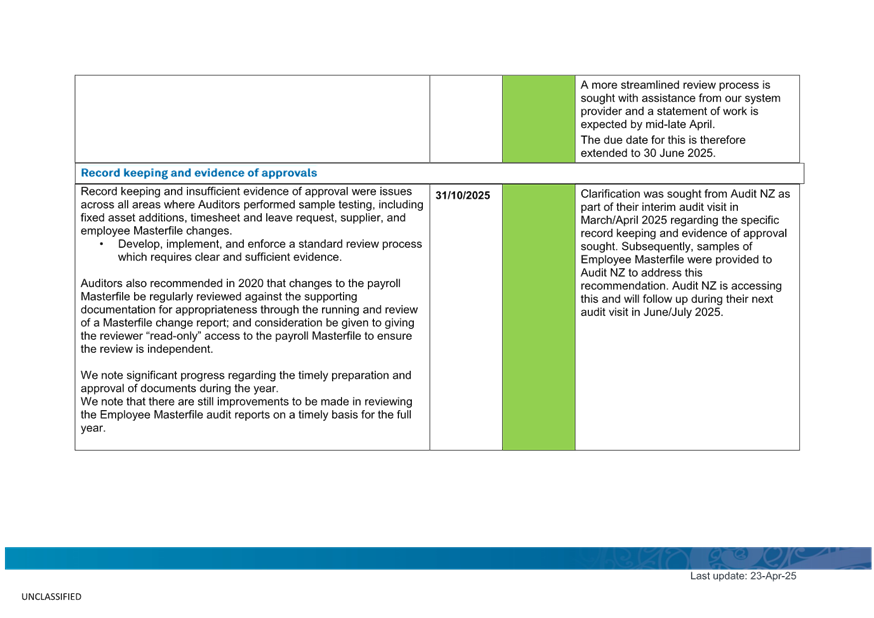

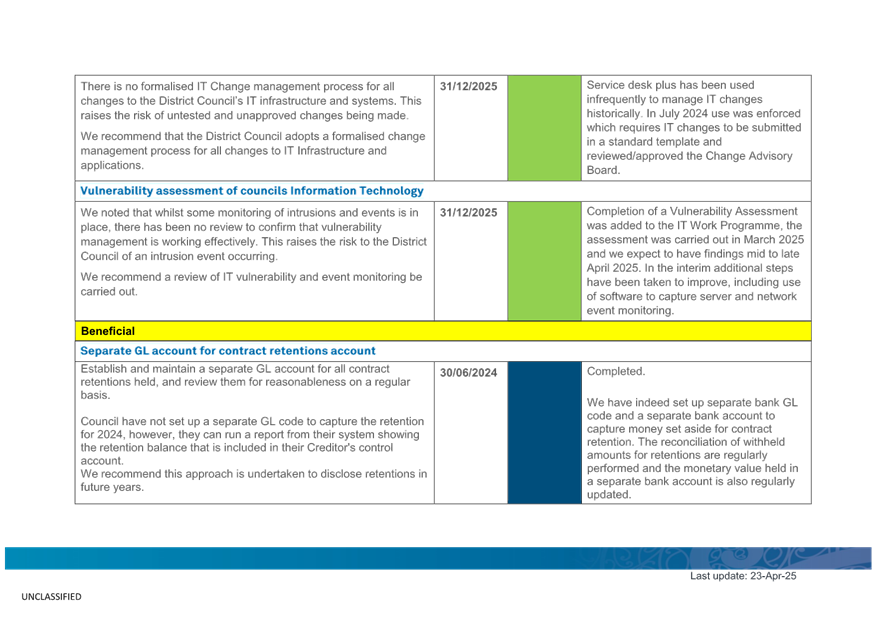

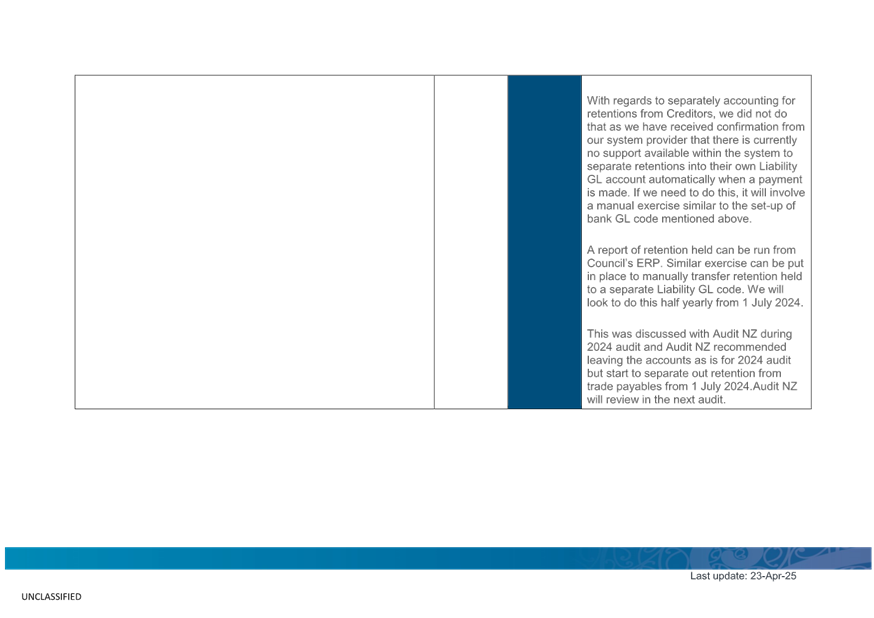

Audit NZ regarding three recommendations:

· “Establish a

separate GL account for contract retentions”

· “Record

keeping and evidence of approvals”

· “Legislative

Compliance”

Audit NZ’s have indicated that

they are likely to close three recommendations off as part of finalising the

interim audit. These relate to the recommendations officers have deemend

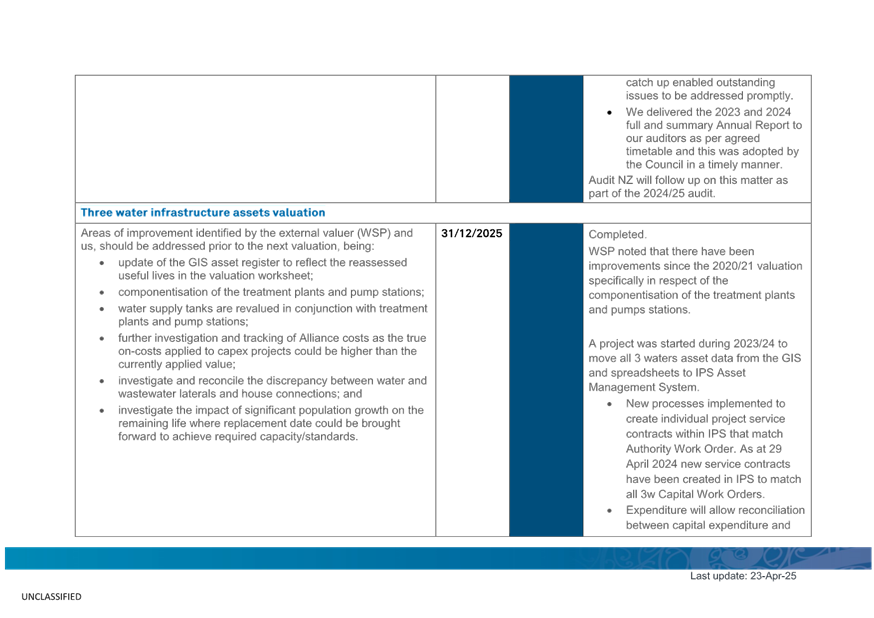

completed. There was also mutual agreement to merge some open recommendations

together, particularly those around asset valuation, and service performance

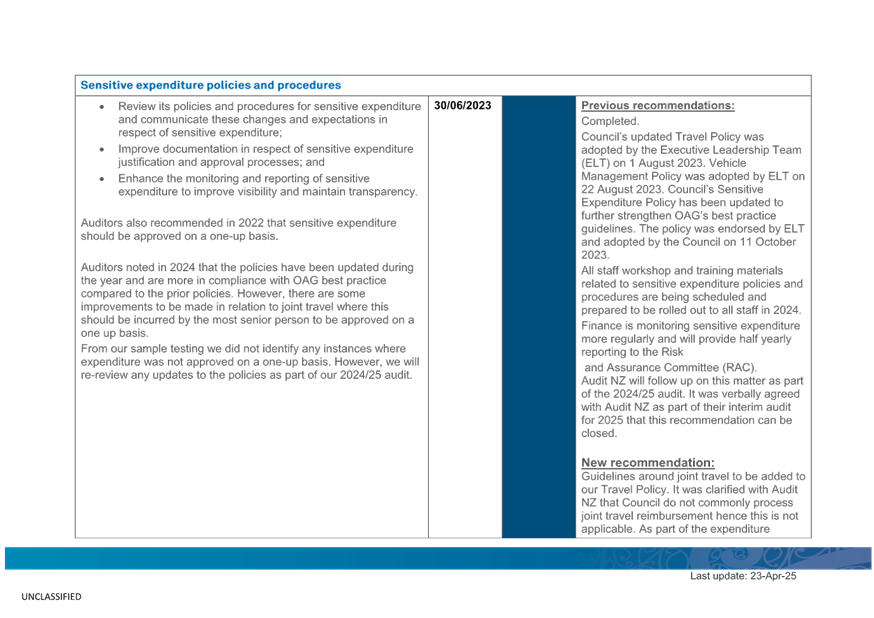

reporting, as well as the mutual agreement to close the recommendation for

“Sensitive expenditure policies and procedures” and for

“Three Waters infrastructure assets”. There are likely to be three

of the 13 open recommendations cleared by Audit NZ as part of the 2025 annual

audit.

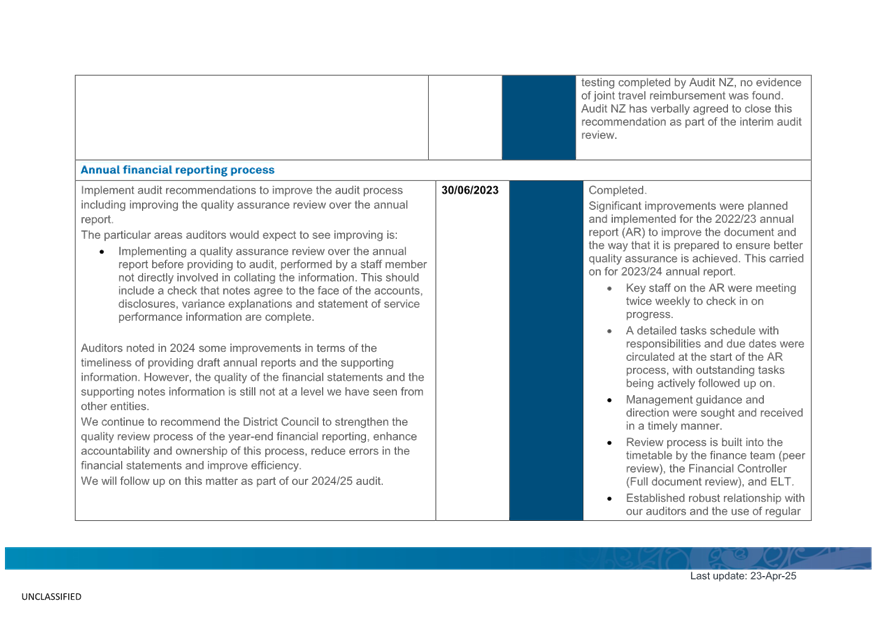

8. Discussion

and consideration mentioned in the point above will be included in 2025 Audit

Management letter. Audit NZ will also be providing a summarised interim audit

management letter to reflect the outcome.

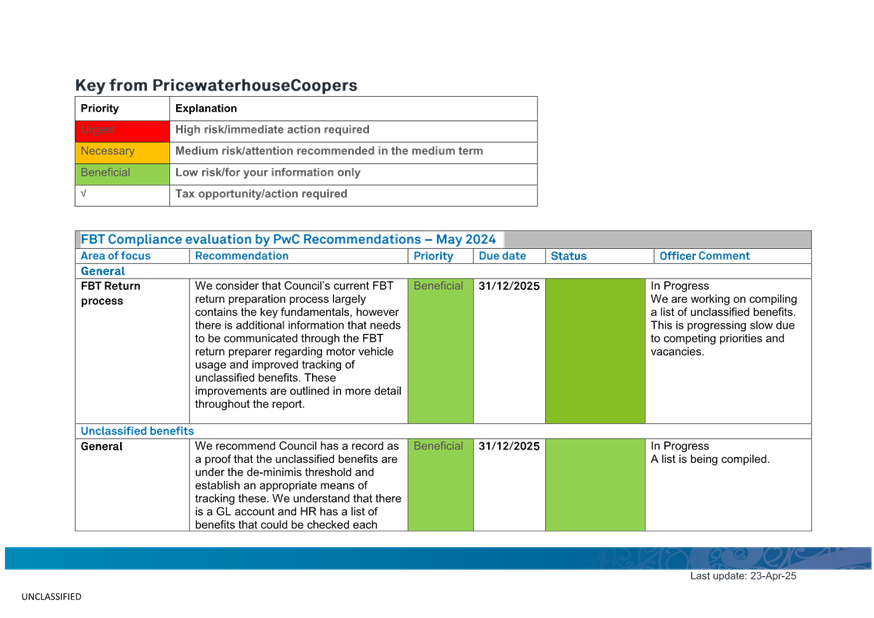

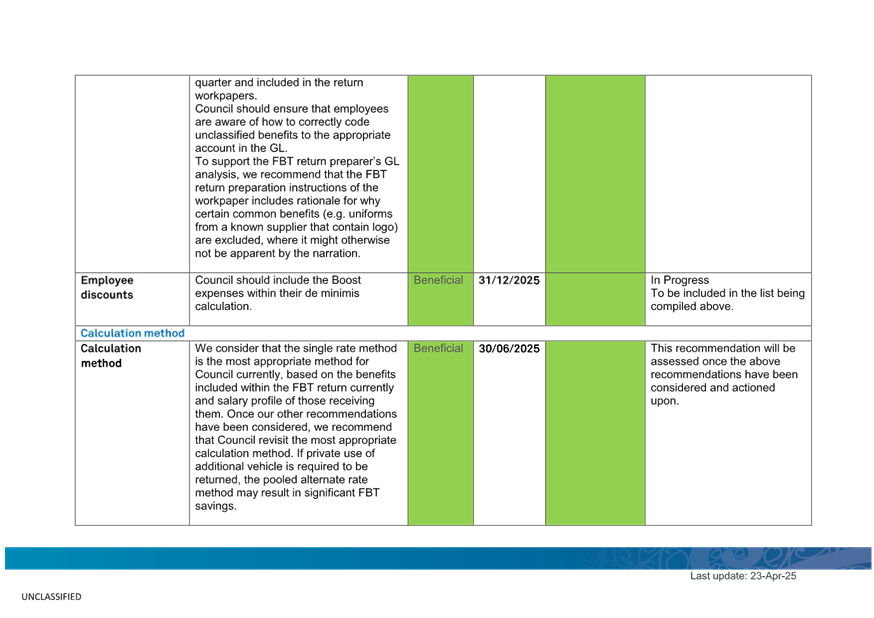

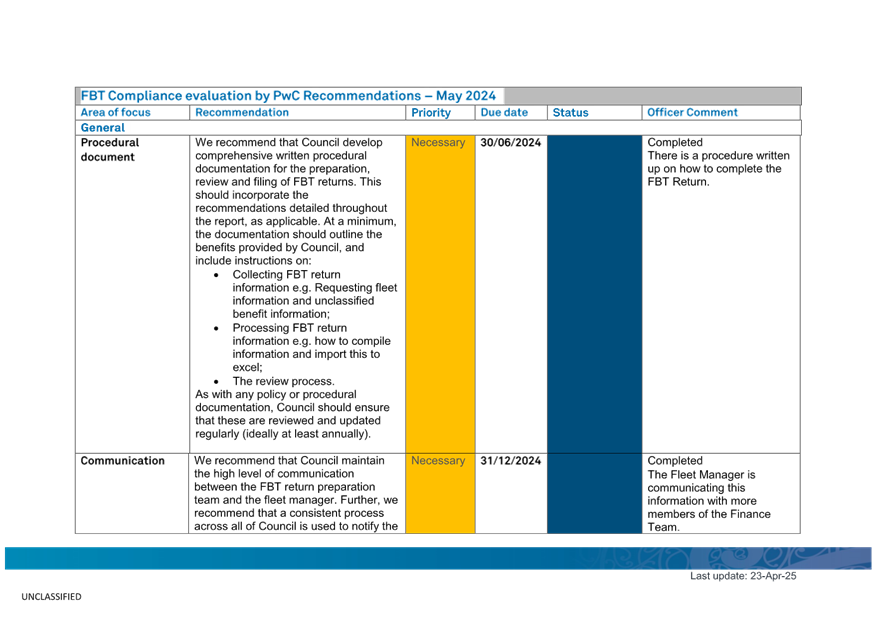

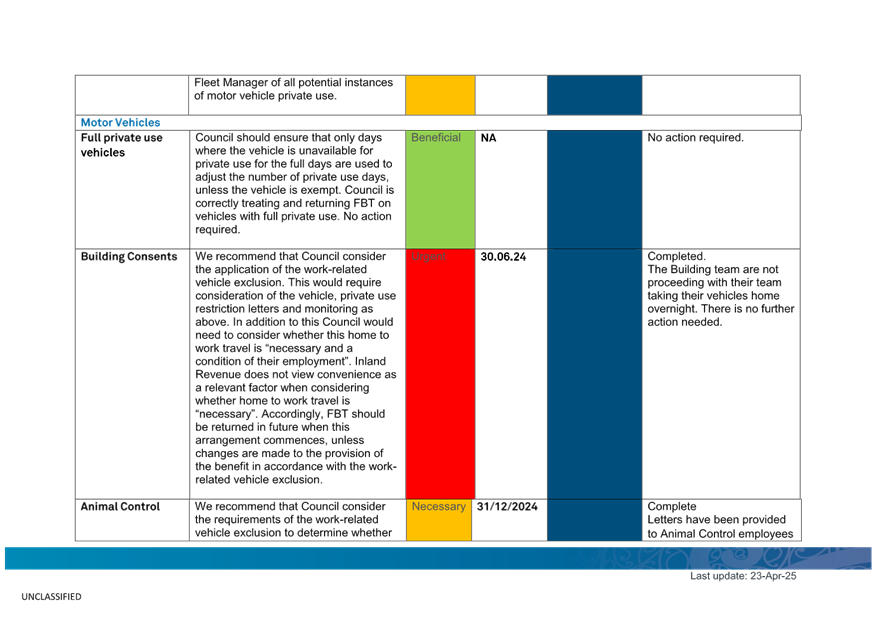

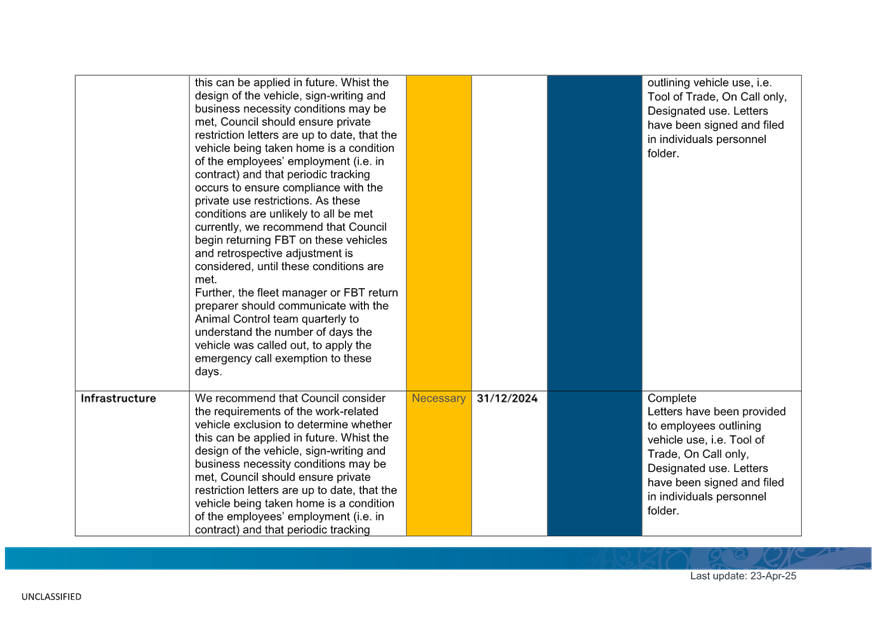

9. Four

outstanding recommendations resulting from the FBT Compliance evaluation by PwC

are in progress. Two recommendations were completed and archived relating to

HDC motor vehicle private restriction letters which had been actioned.

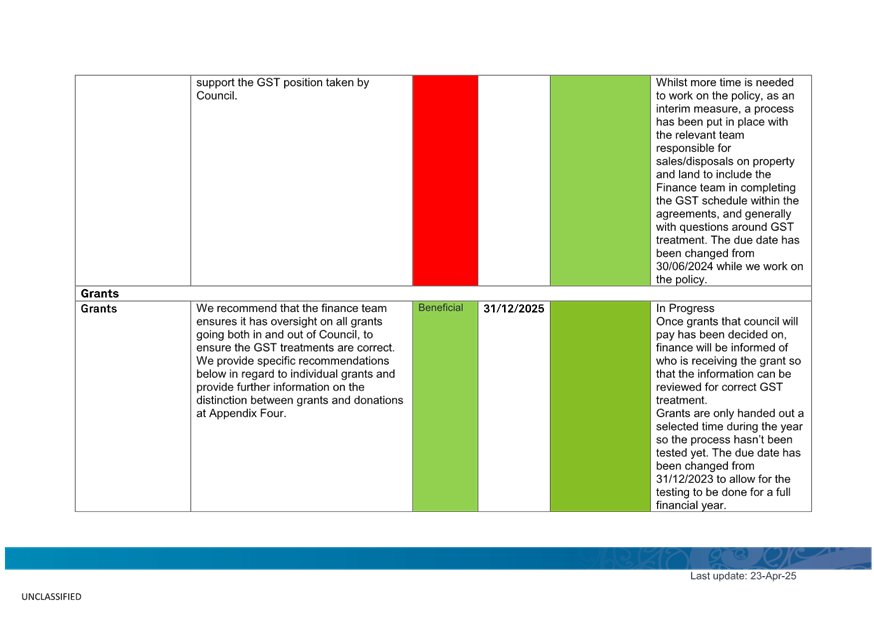

10. Three

outstanding recommendations resulting from the GST Compliance evaluation by PwC

are in progress. These involve fundamental changes needed to Council’s

ERP system to allow for GST coding to be utilised, and drafting of the Asset

Management Policy and so this might not be able to be completed until the next

financial year or as part of the upgrade of our ERP starting in the later part

of 2025/26.

11. One

outstanding item resulting from the PAYE Compliance evaluation by PwC relates

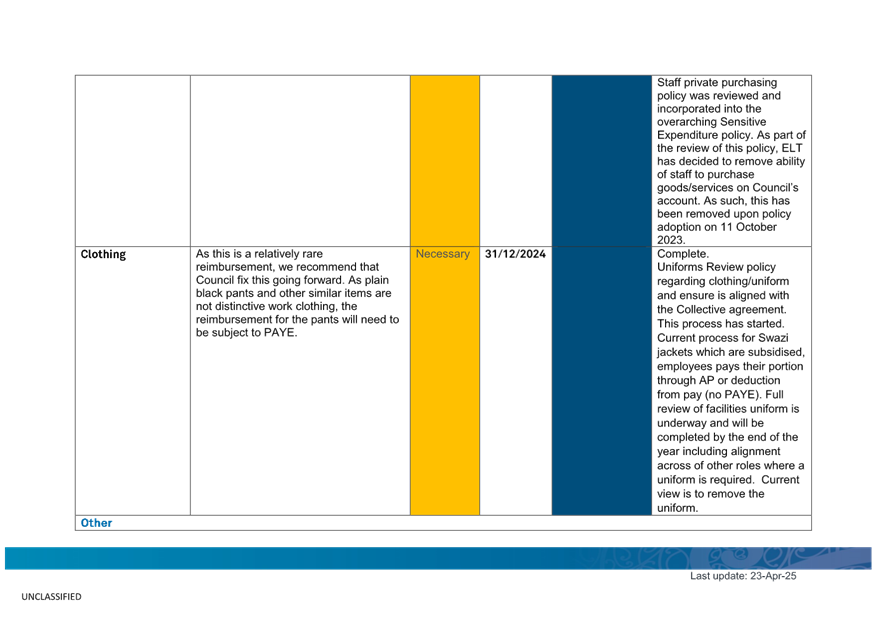

to the review of policy regarding clothing/uniform in the Collective agreement.

Full review of facilities uniform is underway and will be completed by the end

of the year including alignment across of other roles where a uniform is

required. Current view is to remove the uniform. This recommendation was

completed and archived since it was last reported to the committee.

12. Completed

recommendations are archived and shown towards the end of the monitoring report

in Attachment A.

13. As

part of the Tax Governance Framework, PwC has completed the PAYE Compliance

evaluation in April 2025. At the time of writing this report, officers have

just received the draft report from PwC to review. The final report will be tabled with this Committee in subsequent meeting. Any

recommendations resulted from this evaluation will be added to subsequent

monitoring report.

·

|

Confirmation of statutory compliance

In accordance

with sections 76 – 79 of the Local Government Act 2002, this report is approved

as:

a. containing

sufficient information about the options and their advantages and

disadvantages, bearing in mind the significance of the decisions; and,

b. is

based on adequate knowledge about, and adequate consideration of, the views

and preferences of affected and interested parties bearing in mind the

significance of the decision.

|

Attachments | NGĀ

TĀPIRINGA KŌRERO

|

No.

|

Title

|

Page

|

|

a⇩

|

Risk & Assurance Committee

Monitoring Report

|

24

|

|

Risk and Assurance Committee

30 April 2025

|

|

|

Risk and Assurance Committee

30 April 2025

|

|

File No.:

25/207

5.3 Health,

Safety and Wellbeing Dashboard - Quarterly Report

|

Author(s)

|

Tanya Glavas

Safety and

Wellbeing Lead | Kaiārahi Whai Oranga

|

|

Approved by

|

Ashley Huria

Business

Performance Manager | Tumu Tutukinga Pakihi

|

|

|

Jacinta Straker

Group Manager

Organisation Performance | Tumu Rangapū, Tutukinga Whakahaere

|

Purpose | TE PŪTAKE

1. This report provides the Committee with Health, Safety and

Wellbeing information and insights for the quarter from January 2025 –

March 2025.

This matter

relates to Pursuing Organisation Excellence

Continuing the

journey of organisational transformation by enabling a culture of service,

excellence and continuous improvement.

RECOMMENDATION | NGĀTAUNAKITANGA

A. That Report 25/207 Health, Safety and Wellbeing Dashboard -

Quarterly Report be received and noted.

DISCUSSION | HE MATAPAKINGA

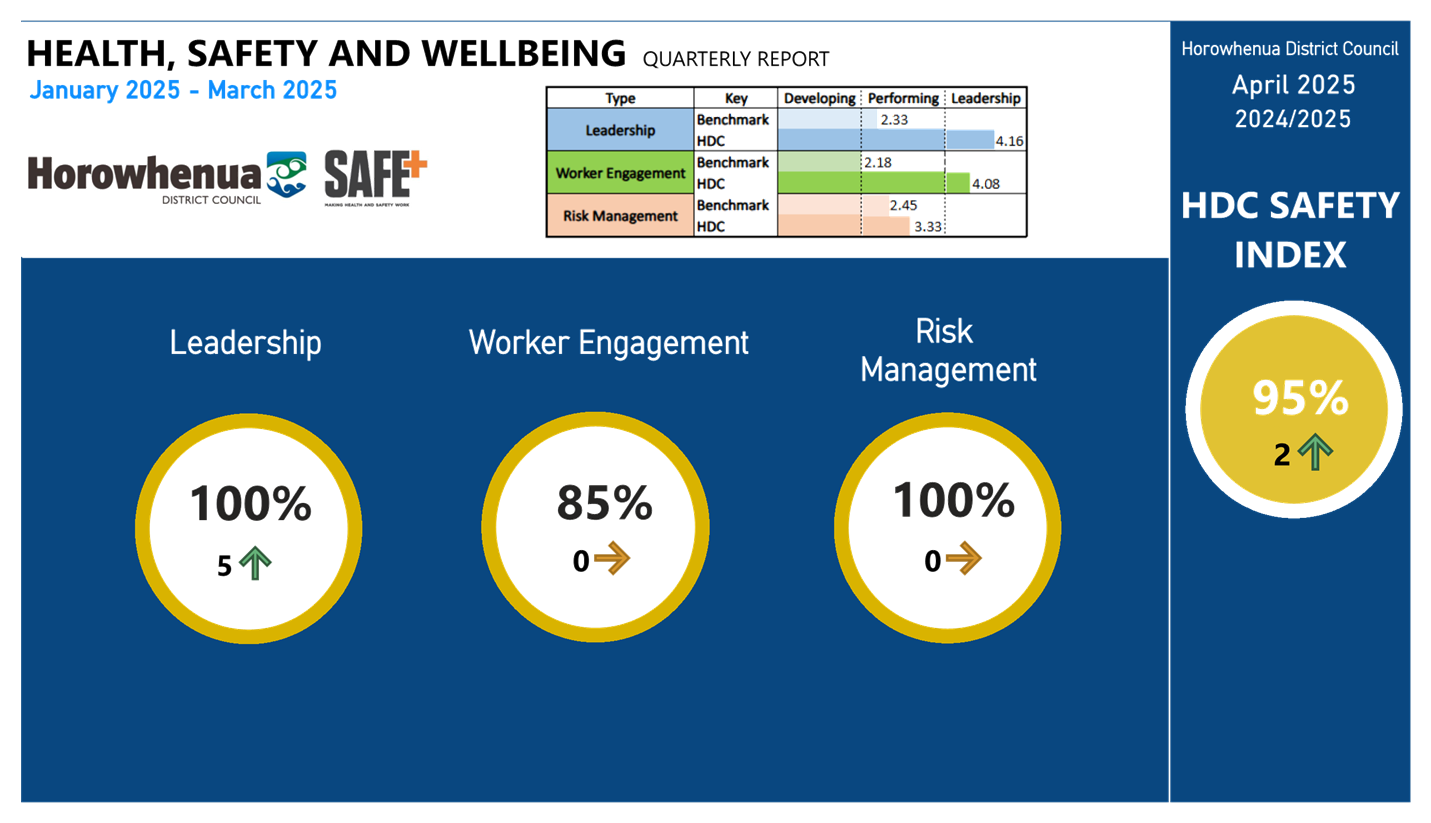

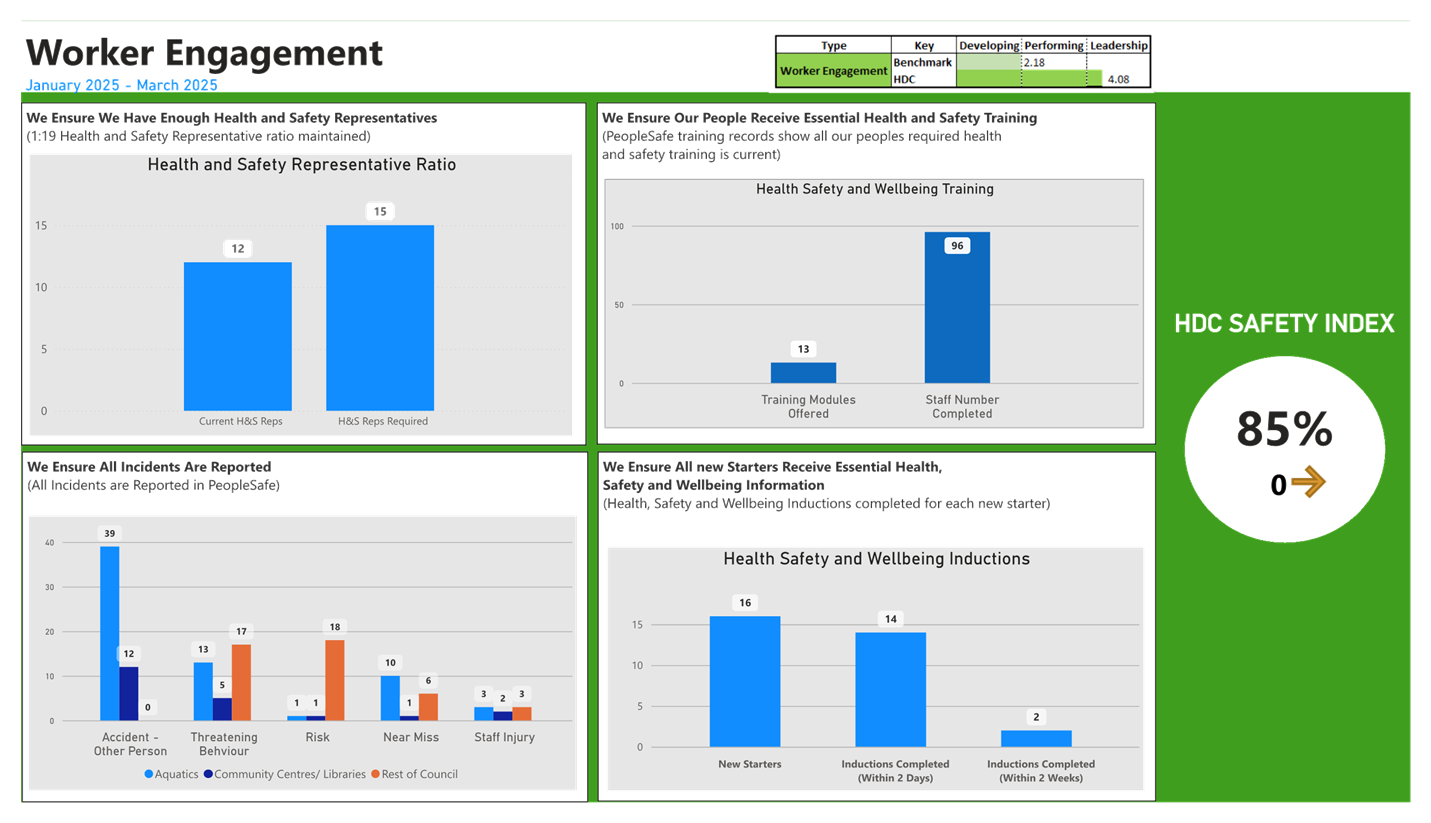

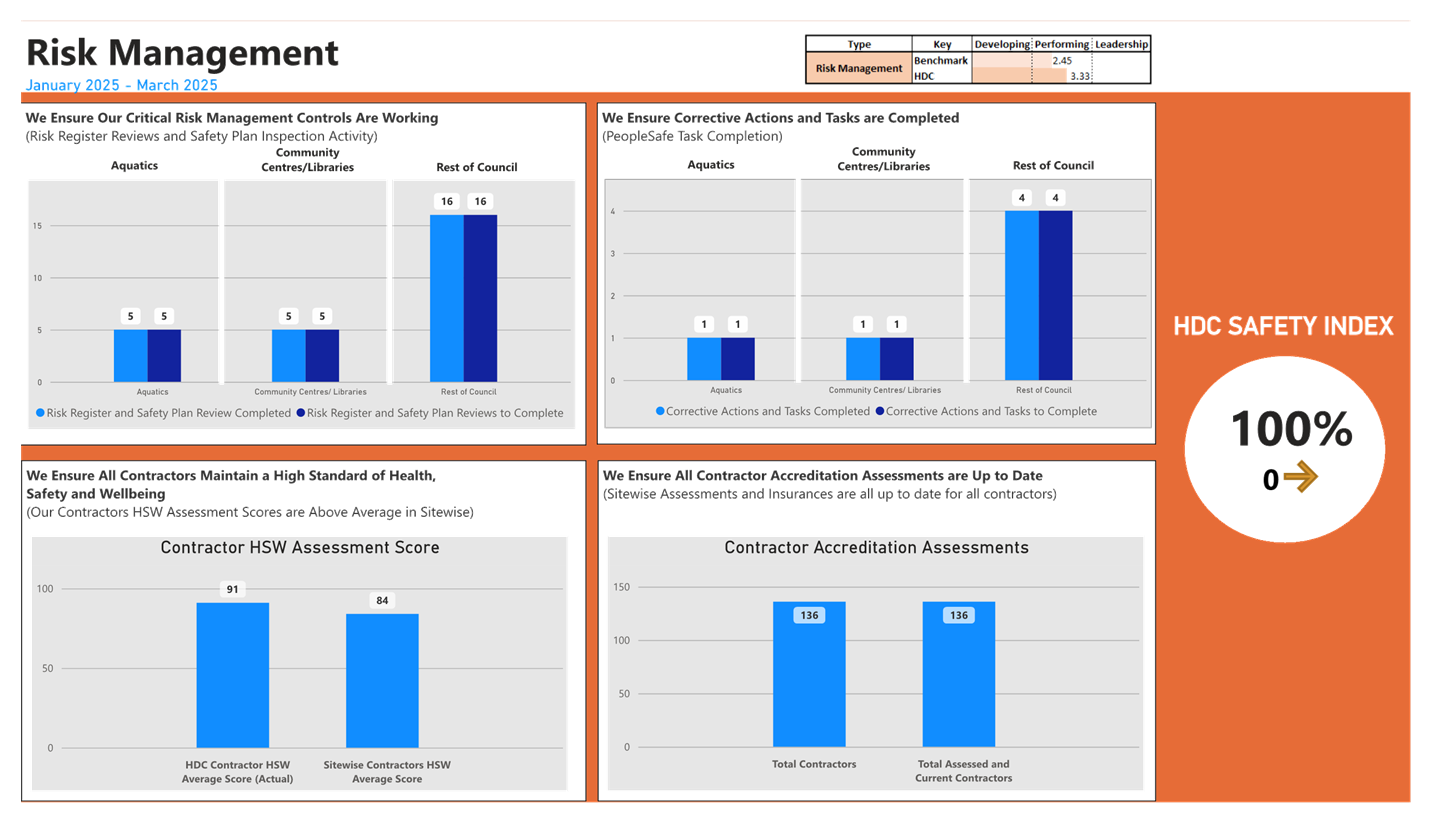

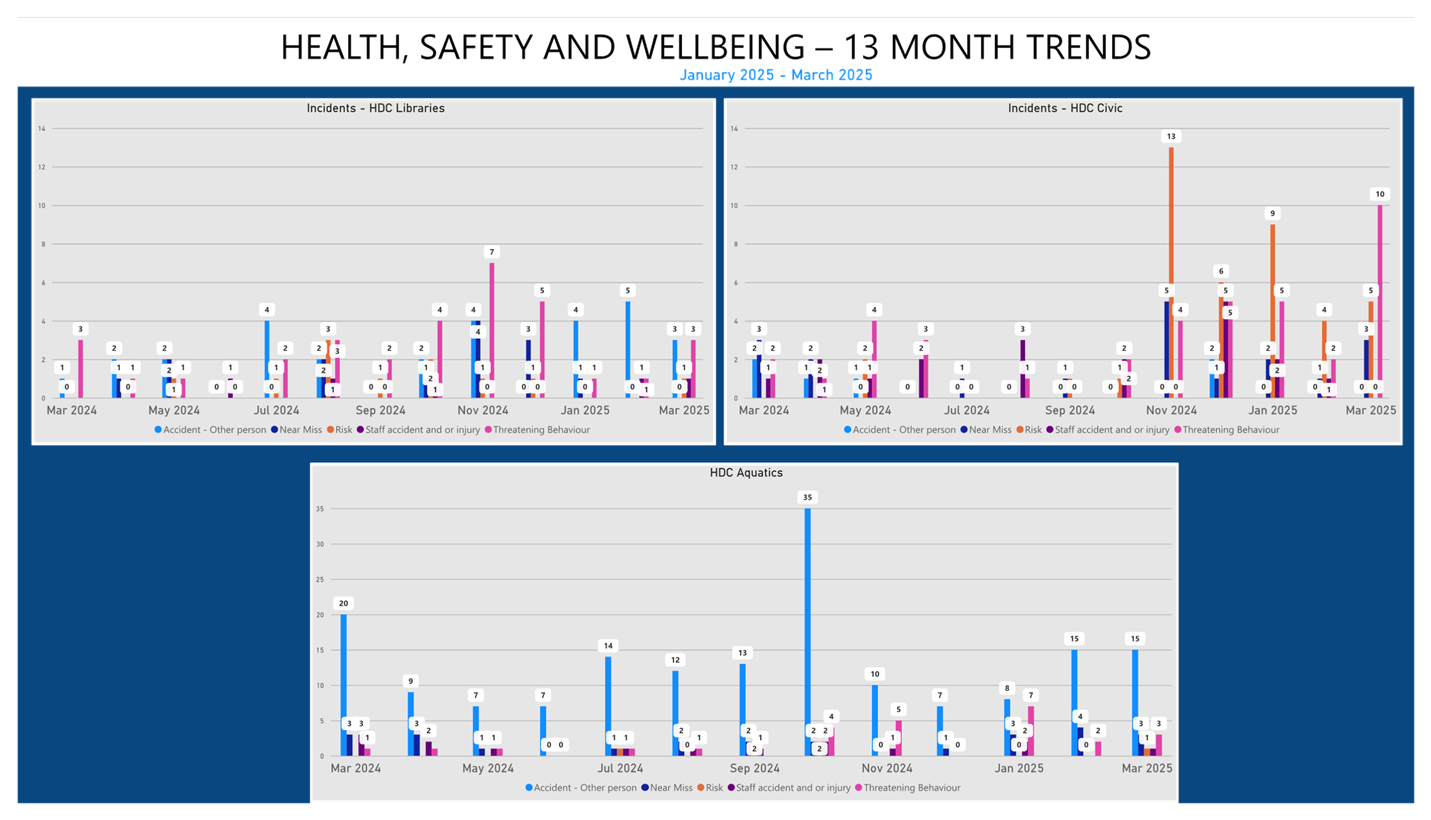

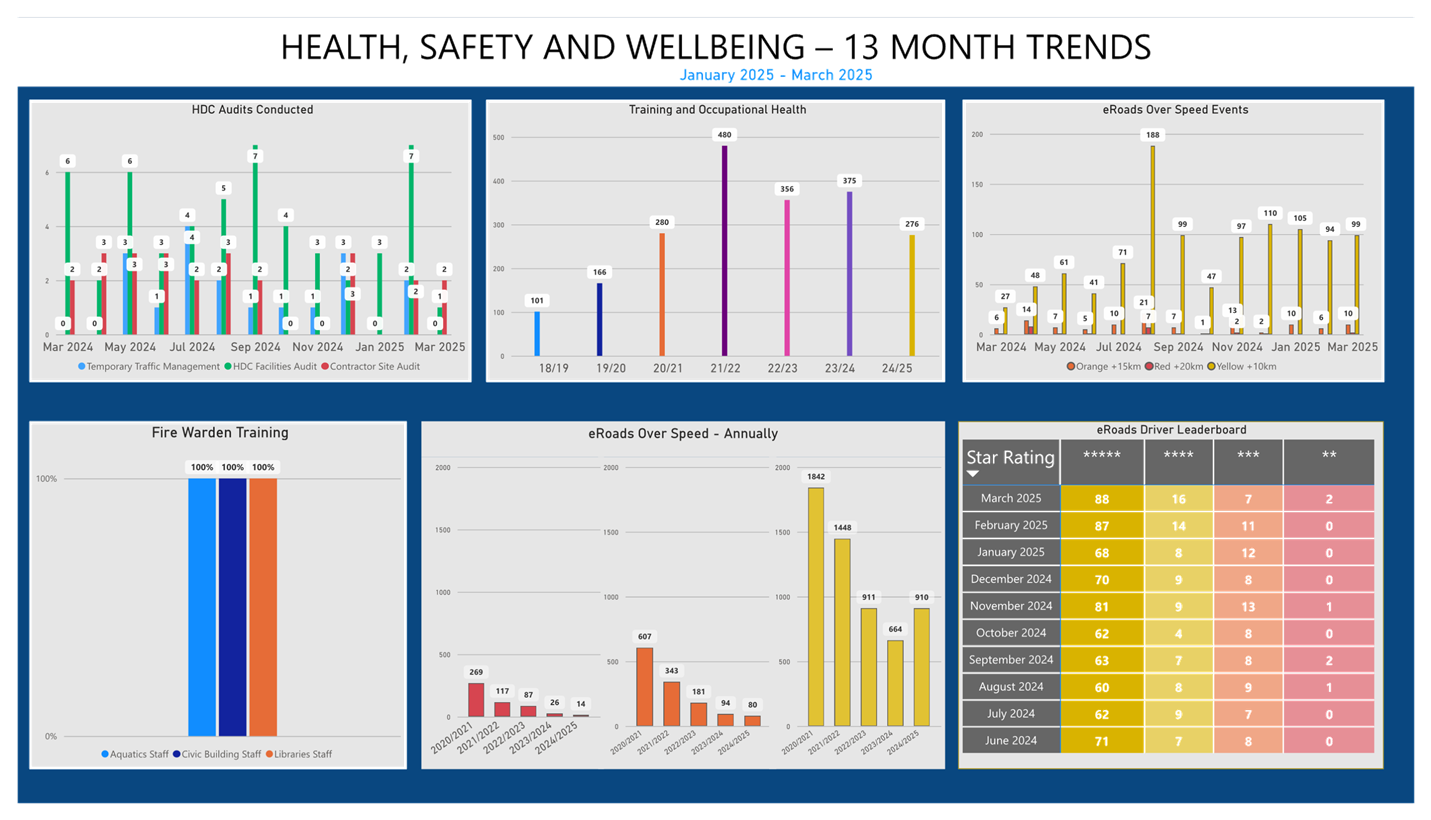

Health Safety and

Wellbeing Dashboard

2. The Health, Safety and Wellbeing (HSW) Dashboard report

gives a broad overview of lead and lag reporting across all of Council. It is

designed to give Elected Members assurance that HSW is being managed for all

staff through worker engagement, risk management and leadership. The variety of

reporting captures multiple aspects of data available to Council and allows the

story of HSW across the three-month reporting period to be told.

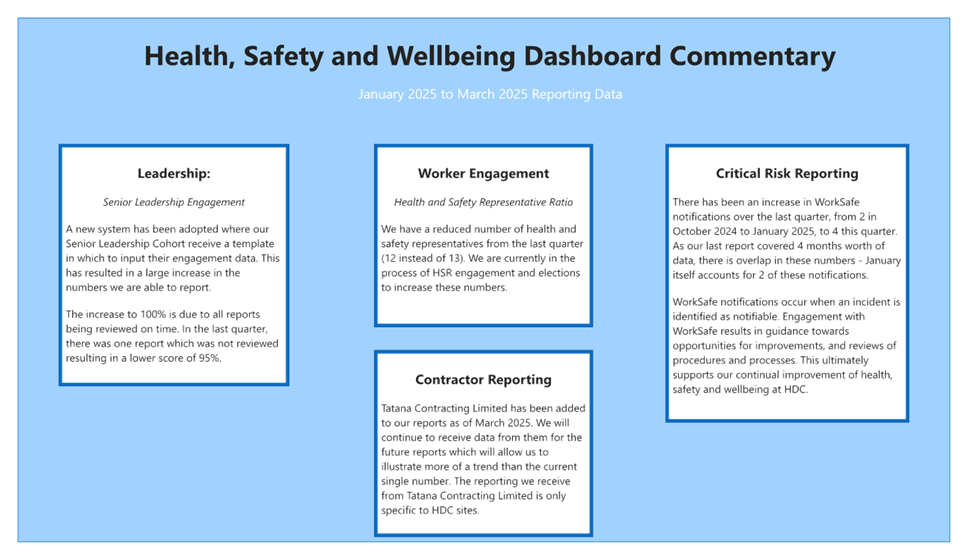

3. The dashboard report for this quarter shows a positive

approach to reporting across Council, including the areas of leadership

engagement and incident reporting.

4. The

HDC Safety Index on the front page has changed as of November 2024. We no

longer have access to our external provider for Health and Safety indices and

as such, we had to change our report to reflect internal data only. This change

has come about due to no longer having complimentary access to this

information. This gave us the opportunity to create a standardised marking

criteria that will allow changes and growth to be better tracked across the

months of the dashboard reports.

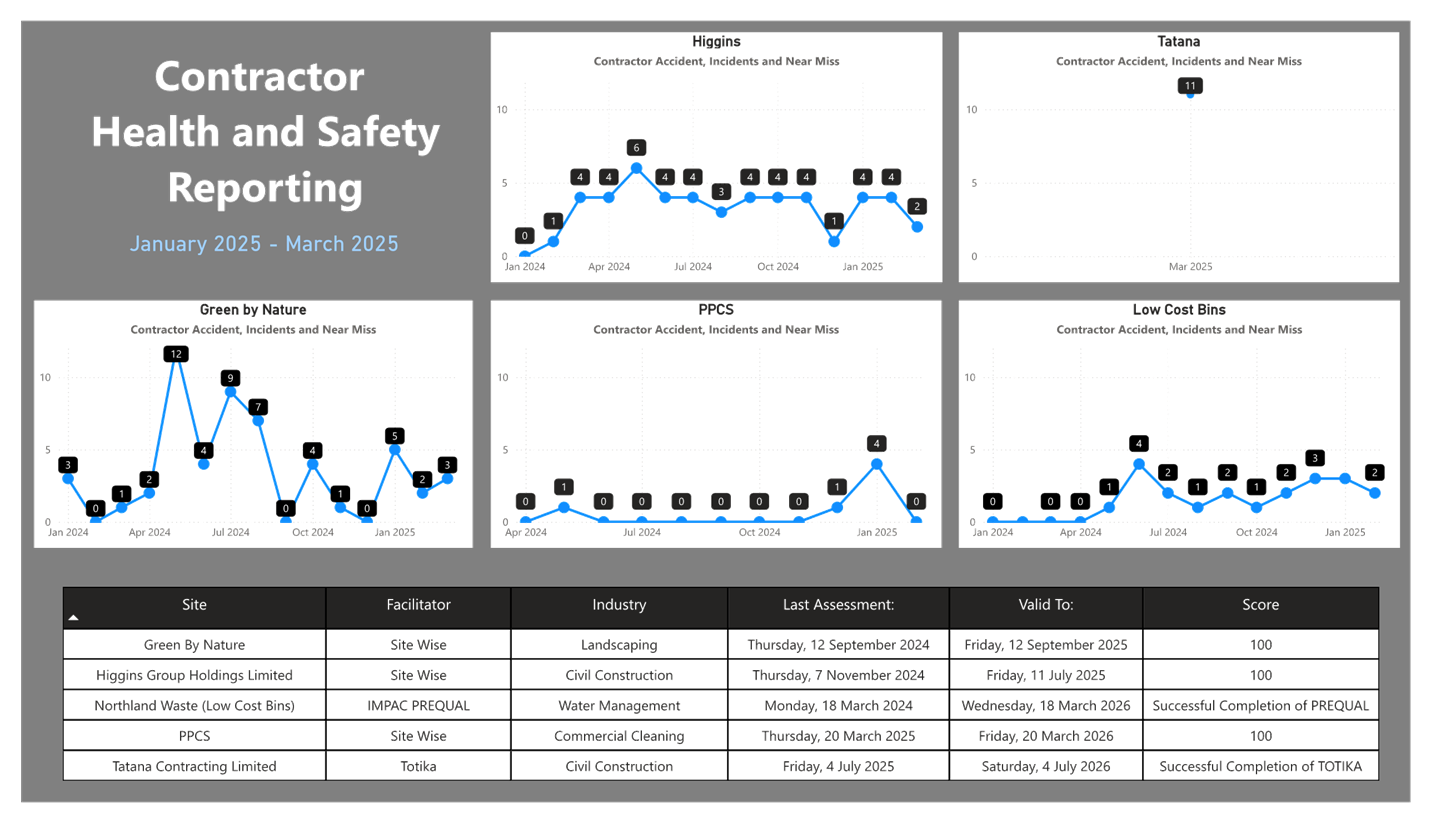

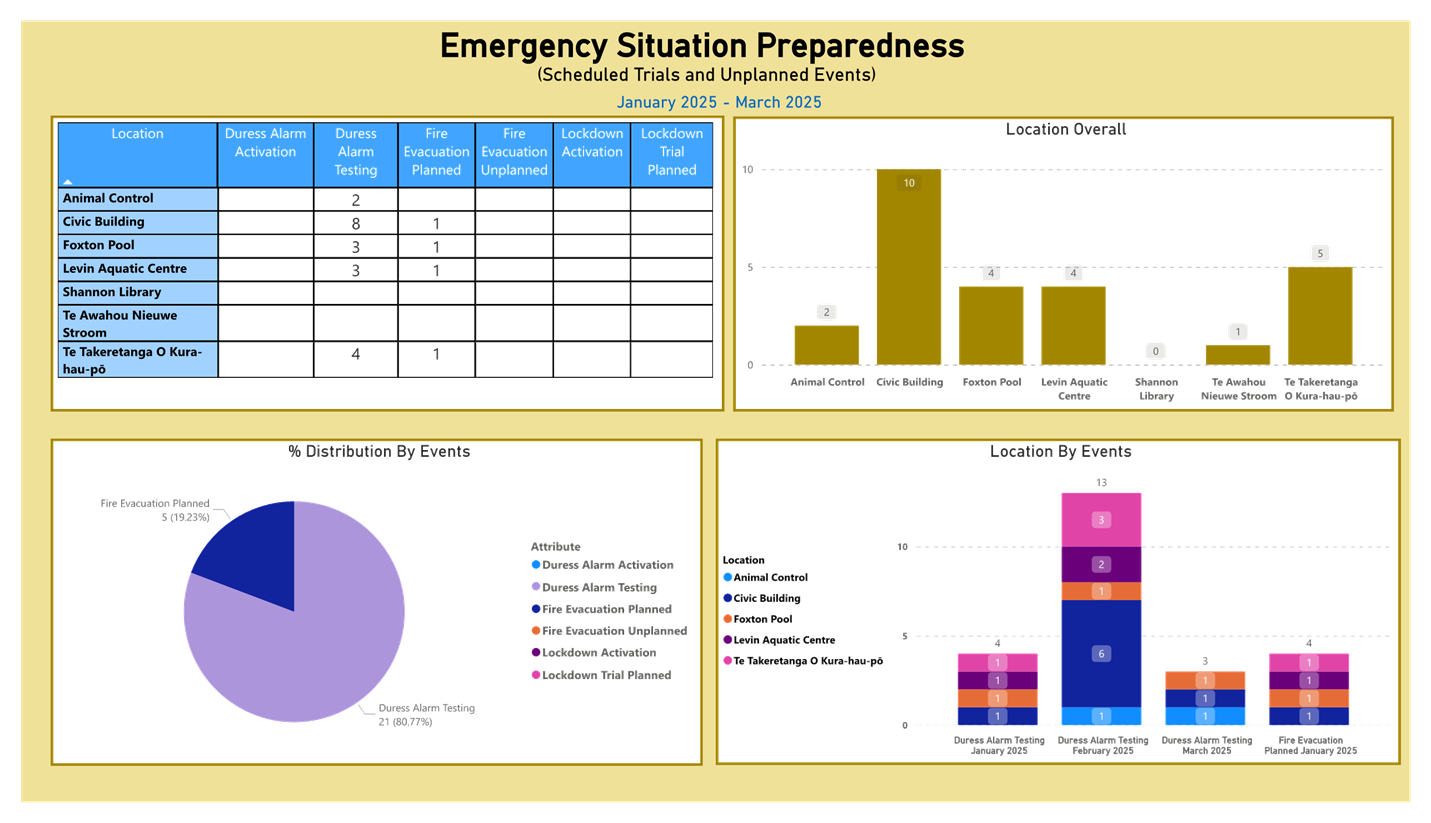

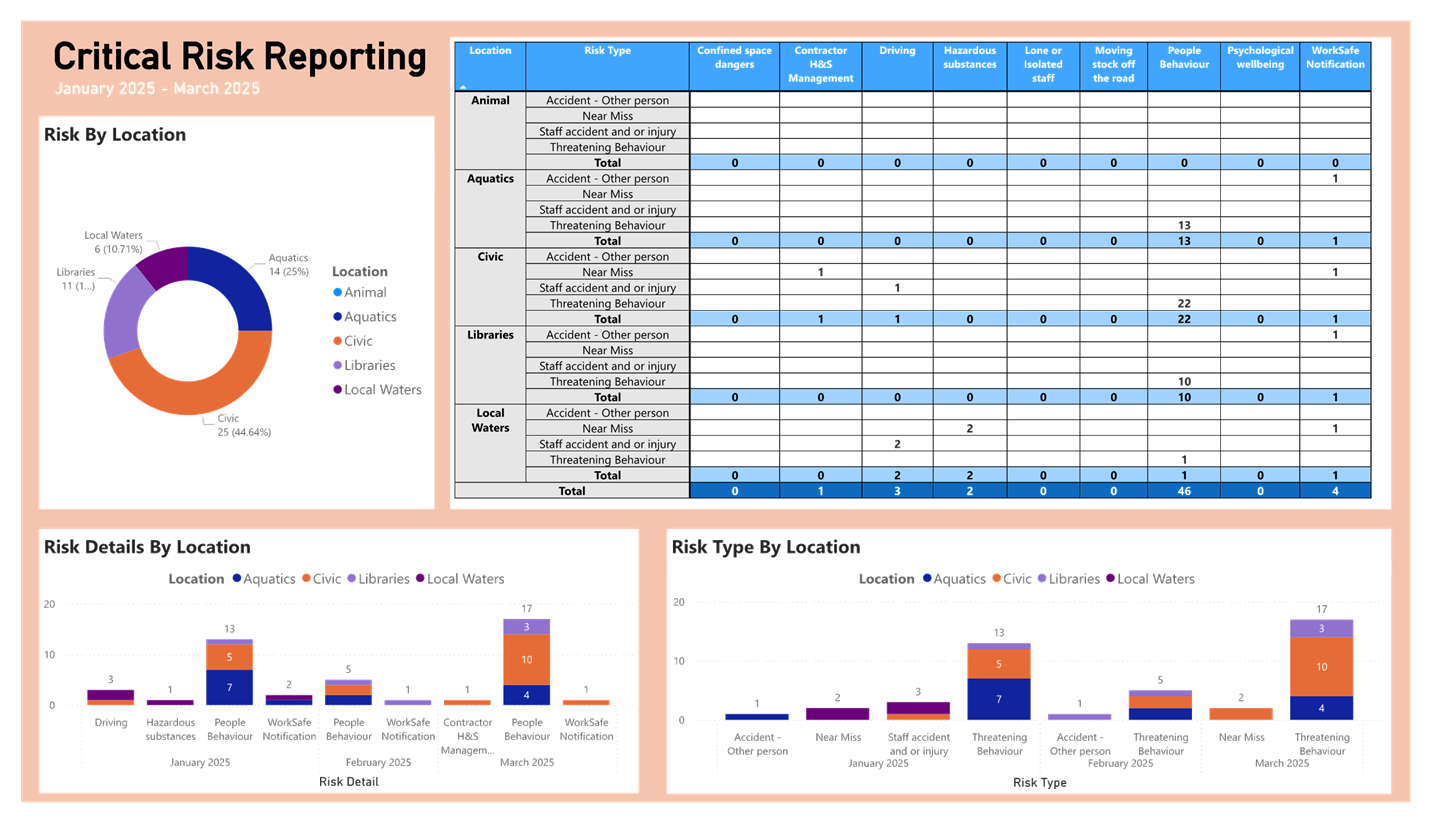

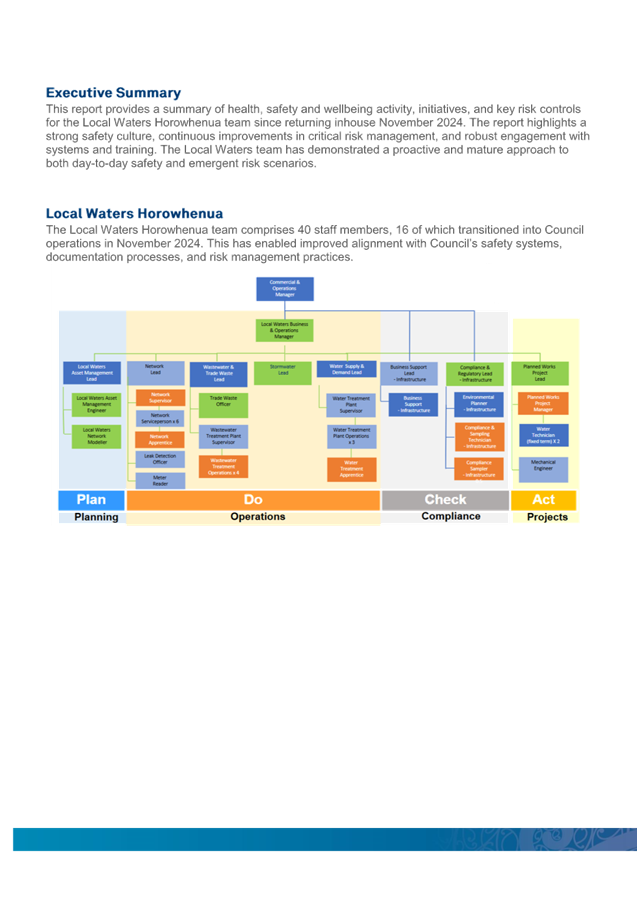

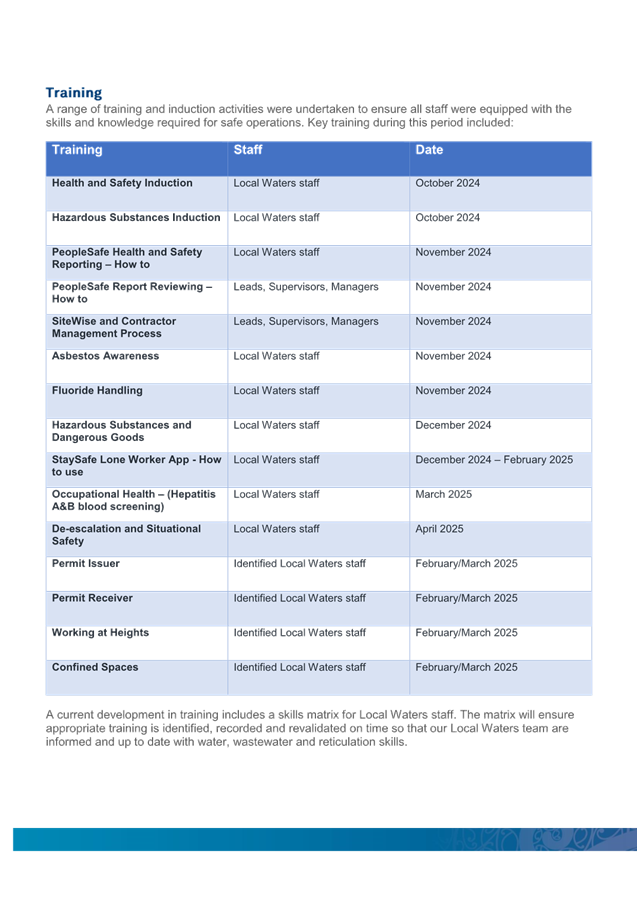

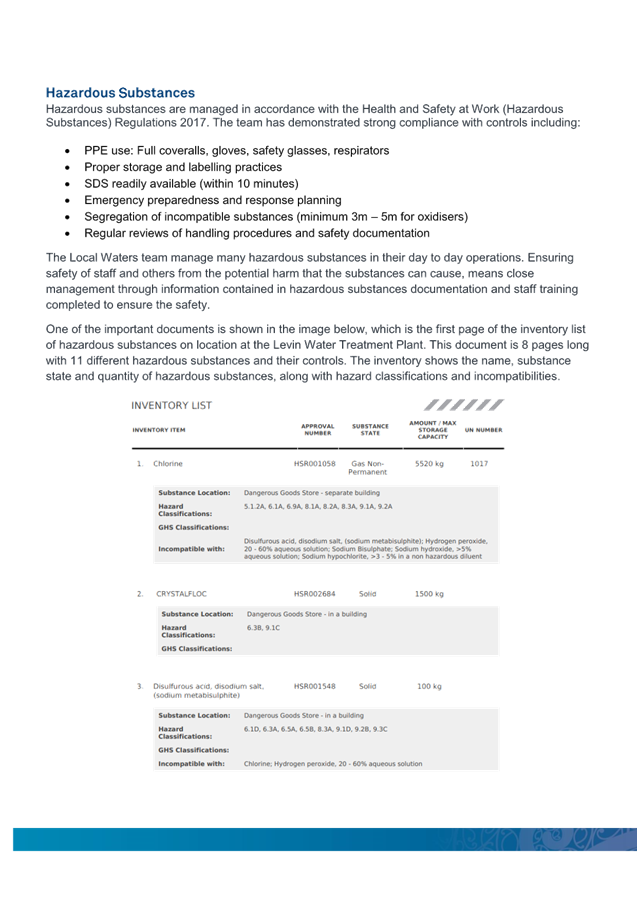

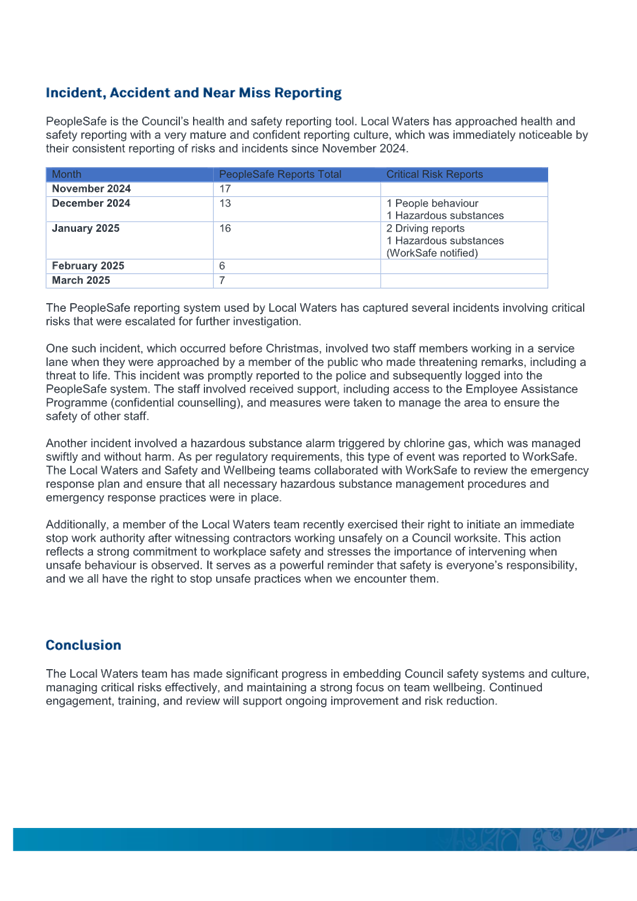

Deep Dive – Local

Water

5. The

Local Water deep dive supports due diligence by providing Elected Members with

assurance that Health and Safety has been effectively addressed and continues

to improve since the work was brought in-house. It highlights a strong focus on

risk reduction and preparedness through training. The deep dive also provides

evidence that Council has appropriate resources and processes in place to

identify, manage, and minimise significant risks.

·

|

Confirmation of statutory compliance

In accordance

with sections 76 – 79 of the Local Government Act 2002, this report is

approved as:

a. containing

sufficient information about the options and their advantages and

disadvantages, bearing in mind the significance of the decisions; and,

b. is

based on adequate knowledge about, and adequate consideration of, the views

and preferences of affected and interested parties bearing in mind the

significance of the decision.

|

Attachments | NGĀ

TĀPIRINGA KŌRERO

|

No.

|

Title

|

Page

|

|

a⇩

|

Health, Safety and Wellbeing - Dashboard

Report - January to March 2025

|

75

|

|

b⇩

|

HSW - Local Waters Deep Dive -

April 2025

|

86

|

|

Risk and Assurance Committee

30 April 2025

|

|

|

Risk and Assurance Committee

30 April 2025

|

|

|

Risk and Assurance Committee

30 April 2025

|

|

File No.:

25/208

5.4 Legislative

Compliance

|

Author(s)

|

Ashley Huria

Business

Performance Manager | Tumu Tutukinga Pakihi

|

|

Approved by

|

Jacinta Straker

Group Manager

Organisation Performance | Tumu Rangapū, Tutukinga Whakahaere

|

|

|

Monique Davidson

Chief Executive

Officer | Tumuaki

|

Purpose | TE PŪTAKE

1. This

report details the Council’s legislative compliance for the 12 months to

28 February 2025.

This matter

relates to Pursuing Organisation Excellence

Continuing the

journey of organisational transformation by enabling a culture of service,

excellence and continuous improvement.

RECOMMENDATION | NGĀTAUNAKITANGA

A. That Report 25/208 Legislative Compliance be received and noted.

bACKGROUND | hE

KŌRERO TŪĀPAPA

1.1 The

previous Legislative Compliance Report, presented to the Risk and Assurance

Committee on 16 August 2023, provided an overview of best practices, clarified

the concept of legislative compliance, and outlined the benefits of regular

reporting in this area.

1.2 At

that time, the following were identified as the key legislative acts for short

term reporting focus:

· Local

Government Act 2002

· Local

Authorities (Members’ Interests) Act 1968

· Local

Government (Rating) Act 2002

· Local

Government (Financial Reporting and Prudence) Regulations 2014

· Building

Act 2004

· Resource

Management Act 1991

1.3 Officers

manually reported on compliance with these acts to the Risk and Assurance

Committee. However, due to the early stage of maturity in the compliance

framework, and the absence of formal training and development, the reporting

was based largely on individual officers’ knowledge. A comprehensive

legislative review had not yet been completed, and as a result, the level of

confidence in the data provided was considered moderate pending the completion

of a full review.

DISCUSSION | HE MATAPAKINGA

2. Following

this 2023 report it was decided that we would investigate a better option for

monitoring compliance through completion of a regular survey. Officers selected

the company ComplyWith, after reviewing the product and discussing with other

Council’s across the country utilising the tool.

3. ComplyWith

is a New Zealand-based compliance management software solution designed to help

organisations understand and meet their legal obligations. The platform focuses

on simplifying legal compliance through plain-language legal content,

personalised obligation reporting, and intuitive software tools that enhance

accountability and reduce compliance risks.

4. Key

features of ComplyWith include:

· Tailored

Legal Obligations for each role: Delivers obligation summaries written in plain

language, specific to the organisation’s operations and structure.

· User-Friendly

Reporting Survey Tools: Enables staff to easily identify and report on legal

compliance risks, promoting internal ownership and awareness.

· Reporting

& Risk Visibility: Powerful tools to track compliance status, identify

potential risks, and provide clear, real-time reporting for decision-makers.

· Legal

Assurance: Regularly updated legal content authored and verified by experts to

ensure accuracy.

5. ComplyWith

is particularly well-suited for councils, and other organisations seeking

transparency, clarity, and efficiency in managing their legal obligations. The

platform supports a culture of proactive compliance, reducing the risk of legal

issues and enhancing governance outcomes.

6. Alongside

the software implementation, the previously outlined programme has commenced,

with many elements now underway or completed, including the identification of

all relevant legislation, including the higher risks areas and targeted

training and development.

7. In

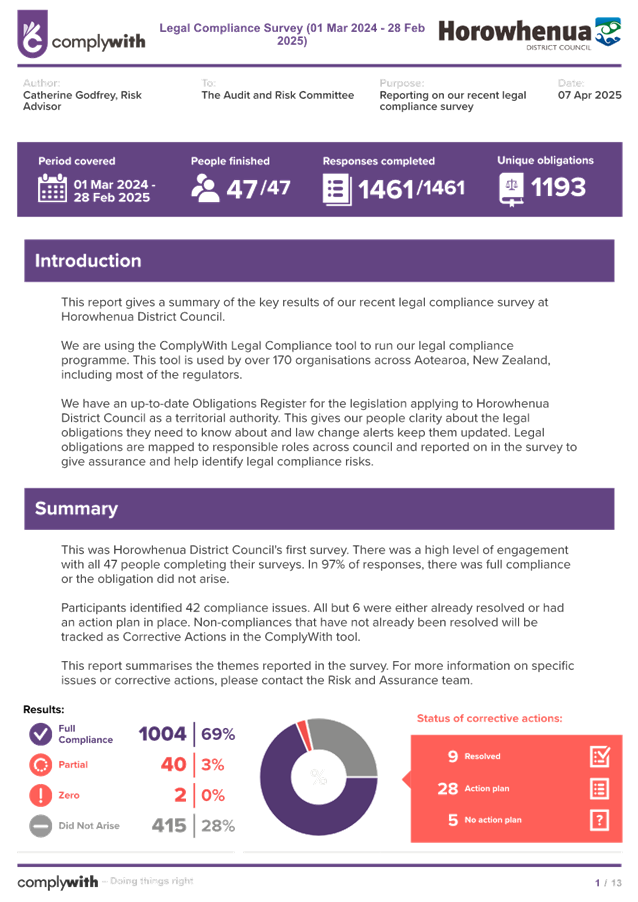

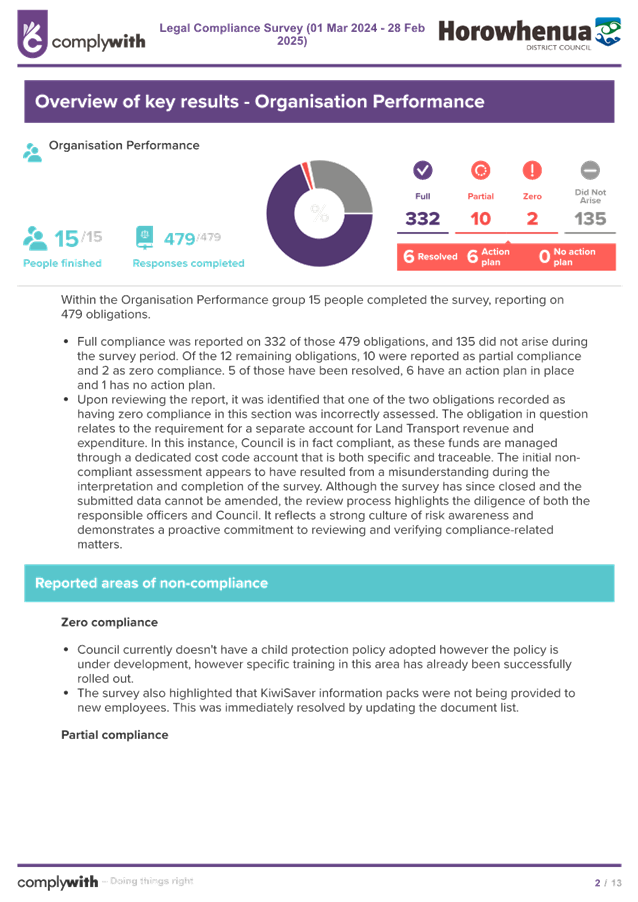

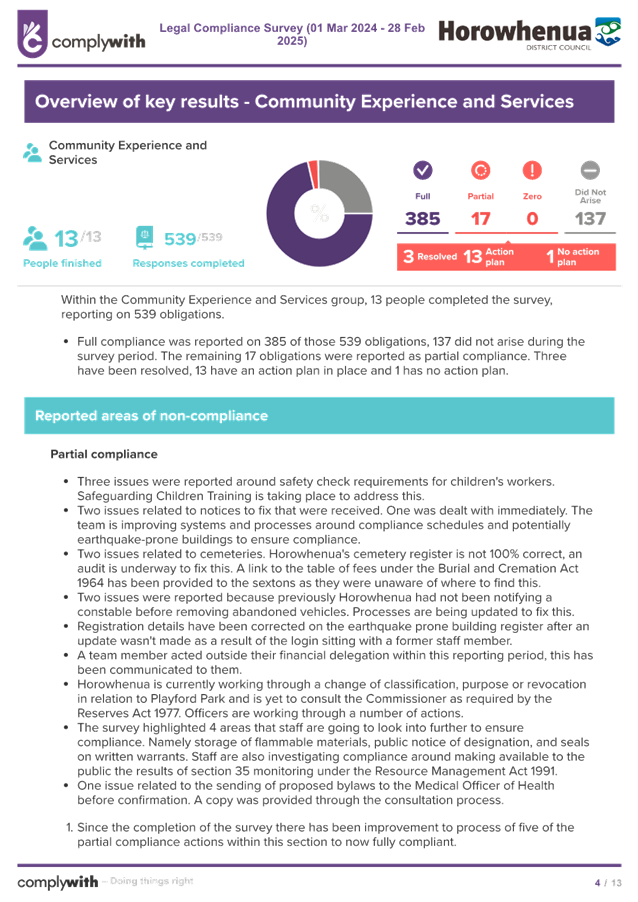

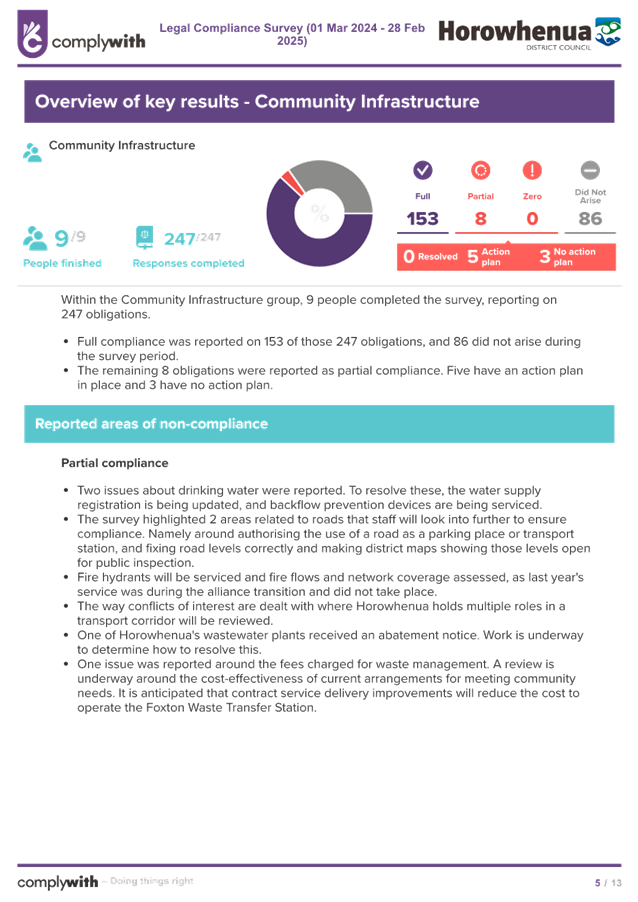

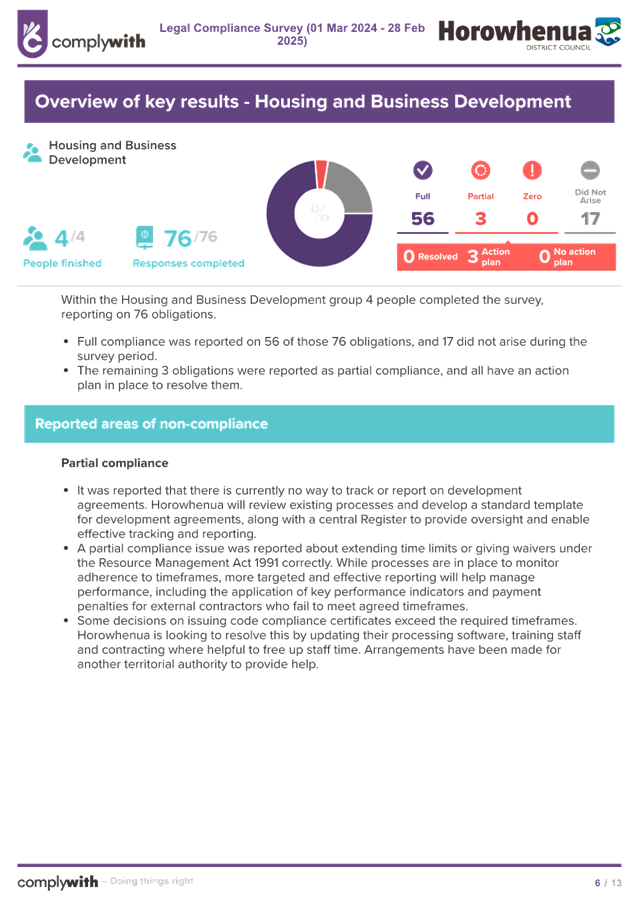

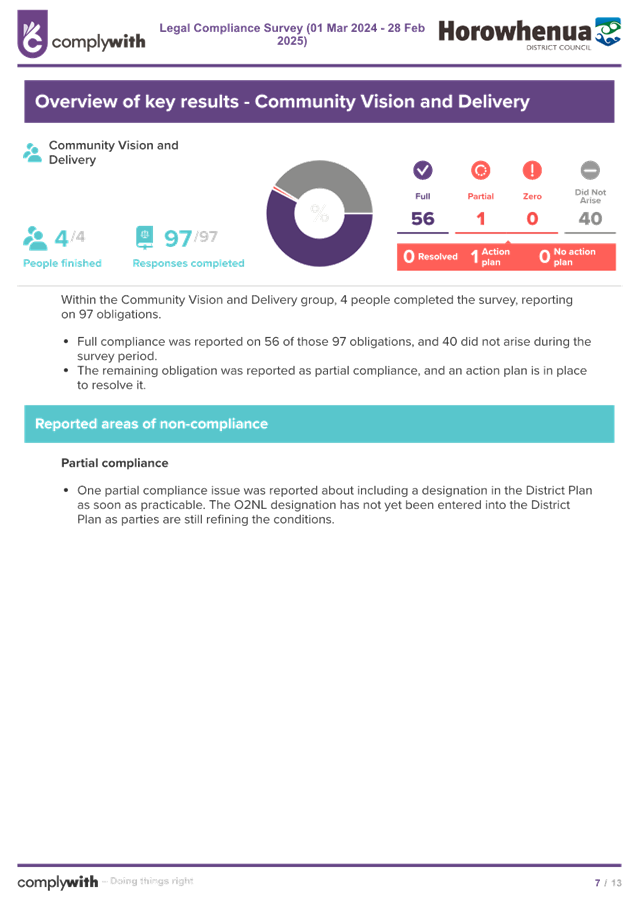

March 2025, the first comprehensive legislative compliance survey was

conducted, covering the period from 1 March 2024 to 28 January 2025. A total of

47 individuals were assigned 1,461 compliance obligations from 104 different

legislations. Of these, 1,004 obligations were met in full, 40 were partially

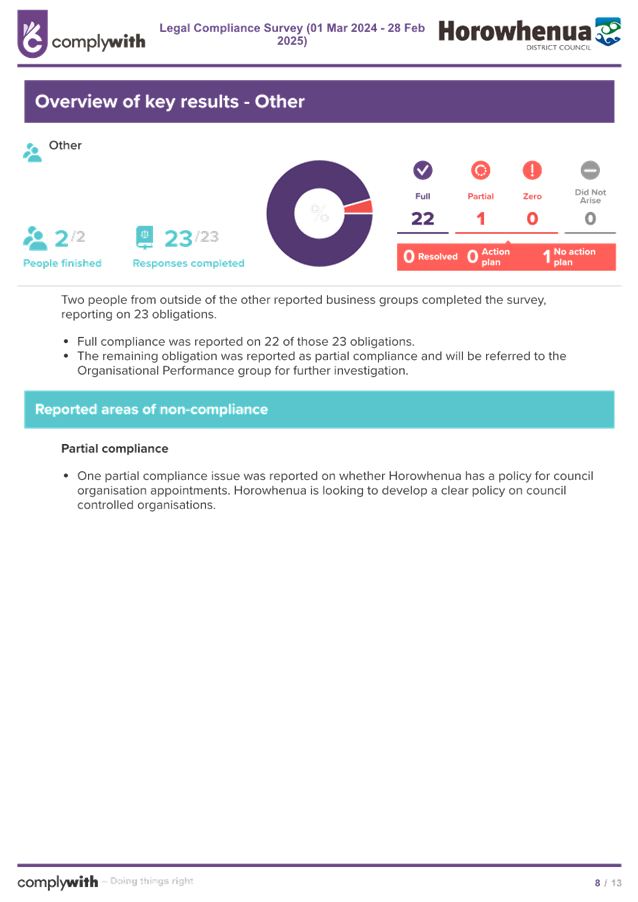

met, 2 were not met, and 415 obligations did not arise during the reporting

period.

8. Upon review of

the report, it was identified that one of the two obligations recorded as

having zero compliance, specifically relating to have a separate account for

Land Transport revenue and expenditure was in fact compliant, but had been

answered incorrectly. This has been noted within the report. While the survey

is now closed and no changes can be made to the submitted data, the review

process reflects positively on both officers and Council. It demonstrates a

strong culture of risk awareness and a proactive approach to reviewing and

investigating reported compliance matters.

9. Attached

to this paper is the detailed report.

NEXT STEPS | HEI MAHI

10. Officers

will review all obligations recorded as partially or non-compliant and

implement the associated action plans to progress toward full compliance.

11. A

monitoring report of partial and zero compliant actions will be present in the

upcoming agenda.

12. The

next survey period will be 1 March 2025 to 28 February 2026.

|

Confirmation of statutory compliance

In accordance

with sections 76 – 79 of the Local Government Act 2002, this report is

approved as:

a. containing

sufficient information about the options and their advantages and

disadvantages, bearing in mind the significance of the decisions; and,

b. is

based on adequate knowledge about, and adequate consideration of, the views and

preferences of affected and interested parties bearing in mind the

significance of the decision.

|

Attachments | NGĀ

TĀPIRINGA KŌRERO

|

No.

|

Title

|

Page

|

|

a⇩

|

Legislative Compliance - HDC

Legal Compliance Survey (1 March 2024 to 28 February 2025

|

102

|

|

Risk and Assurance Committee

30 April 2025

|

|

|

Risk and Assurance Committee

30 April 2025

|

|

File No.:

25/220

5.5 Risk

and Assurance Committee Work Programme

|

Author(s)

|

Ashley Huria

Business

Performance Manager | Tumu Tutukinga Pakihi

|

|

Approved by

|

Jacinta Straker

Group Manager

Organisation Performance | Tumu Rangapū, Tutukinga Whakahaere

|

Purpose | TE PŪTAKE

1. The

purpose of this report is to provide the Risk and Assurance Committee with an

outline of a draft Work Programme for 2024/25.

This matter

relates to Pursuing Organisation Excellence

Continuing the

journey of organisational transformation by enabling a culture of service,

excellence and continuous improvement.

RECOMMENDATION | NGĀTAUNAKITANGA

A. That Report 25/220 Risk and Assurance Committee Work Programme be

received and noted.

B. That the Risk and Assurance Committee supports the proposed Risk and

Assurance Committee Work Programme for 2024/25

DISCUSSION | HE MATAPAKINGA

2. The

Risk and Assurance Committee work programme is attached for consideration.

·

|

Confirmation of statutory compliance

In accordance

with sections 76 – 79 of the Local Government Act 2002, this report is

approved as:

a. containing

sufficient information about the options and their advantages and

disadvantages, bearing in mind the significance of the decisions; and,

b. is

based on adequate knowledge about, and adequate consideration of, the views

and preferences of affected and interested parties bearing in mind the

significance of the decision.

|

Attachments | NGĀ

TĀPIRINGA KŌRERO

|

No.

|

Title

|

Page

|

|

a⇩

|

Risk and Assurance

Committee Work Programme 2024/25

|

117

|

|

Risk and Assurance Committee

30 April 2025

|

|

|

Risk and Assurance Committee

30 April 2025

|

|

File No.:

25/224

5.6 Financial

Dashboard as at 31 March 2025

|

Author(s)

|

Pei Shan Gan

Financial

Controller | Kaiwhakahaere Tahua Pūtea

|

|

Approved by

|

Jacinta Straker

Group Manager

Organisation Performance | Tumu Rangapū, Tutukinga Whakahaere

|

Purpose | TE PŪTAKE

1. This

report presents a high-level overview of the financial position and results to

the committee, with a focus on the March 2025 results.

This matter

relates to Pursuing Organisation Excellence

Continuing the

journey of organisational transformation by enabling a culture of service,

excellence and continuous improvement.

RECOMMENDATION | NGĀTAUNAKITANGA

A. That Report 25/224 Financial Dashboard as at 31 March 2025 be

received and noted.

bACKGROUND | hE

KŌRERO TŪĀPAPA

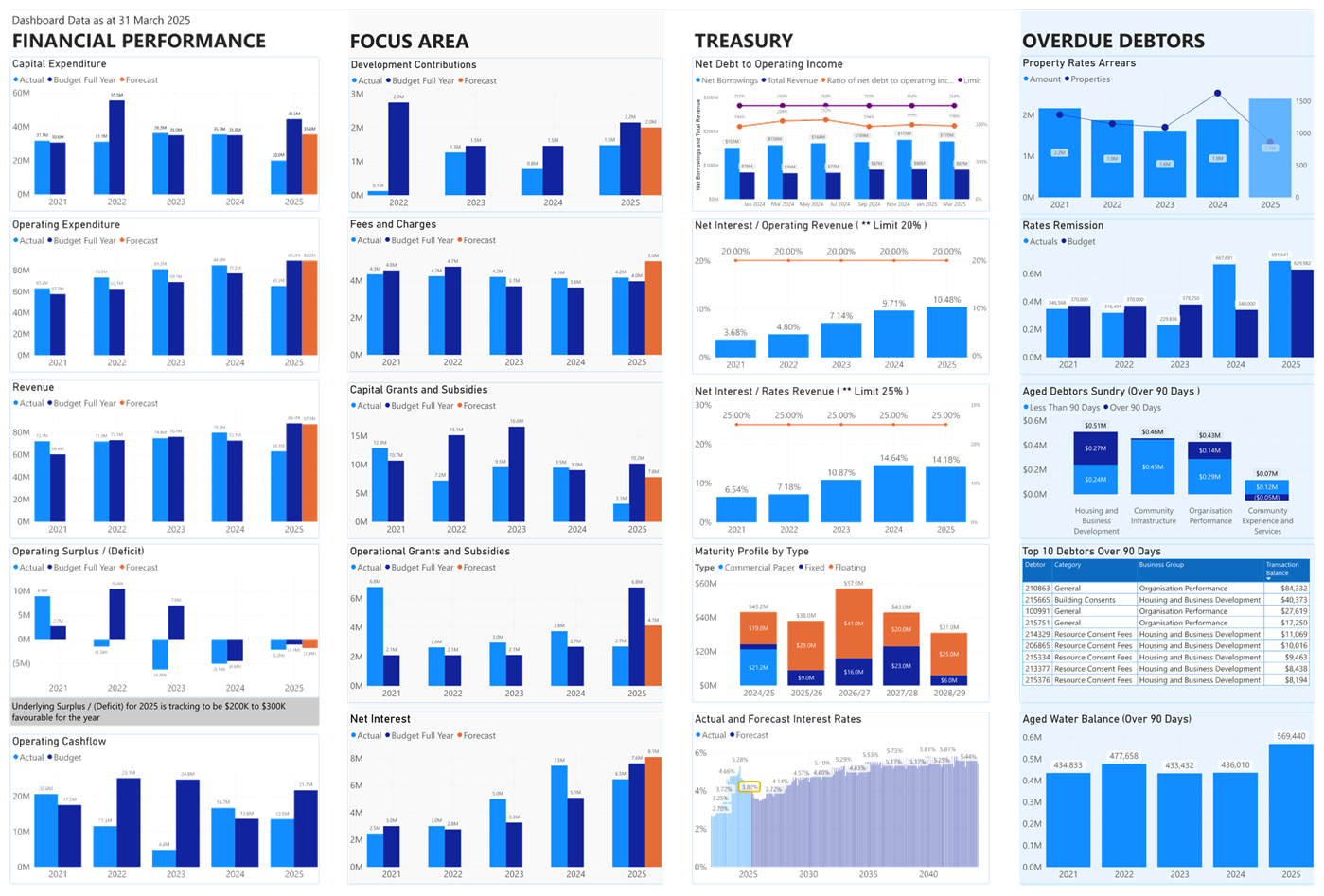

2. The

purpose of the dashboard is to provide an overview of the Financial Results to

enable the committee to understand the results from a risk perspective.

DISCUSSION | HE MATAPAKINGA

3. So

far this year we have received $3.2m less income than planned. This is mainly

due to lower funding from Waka Kotahi, which is offset by lower spending agreed

by Council. It is also due to delayed CIP funding with changes in the timing of

the associated capital projects. The position is forecast to continue for the

year. While the grants are lower, we are tracking well in our Regulatory area

with income for consenting higher than planned and additional waste rebate

received.

4. Our

operating expenditure is currently $1.7m below budget which is largely due to

lower professional services and other operating costs. We also have some

savings in employee costs due to vacancies in the first half of the year. This

is offset by $1.761m loss on interest rate swap. A loss on an interest rate

swap occurs when the value of the swap decreases due to unfavourable changes in

interest rates. Swaps are used to manage interest rate risk and potentially lower

borrowing costs.

5. We

are tracking well to meet the underlying operational budget (excluding capital

items) and we are targeting net savings of $200k to $300k. This is mostly

due to additional net income in Regulatory. There are some risks within the

three waters budget that need to be monitored closely for this to be achieved.

6. We

have completed just under $20m for the capital programme, with around $15.5m

planned to be spent for April – June 2025. This was discussed at the

Capital Projects Steering Group on 19 March and subsequently at the Council

workshop for 2025/26 Annual Plan on 9 April. Overall, we are projecting a

reduction in capital spending this year of $7.7m with a net reduction in

borrowings of $5m for 2024/25. Over the four years (up to 2027/28) it is

anticipated that we will have a net reduction of $4.7m.

7. Rates remission of

$691,641 for 2025 is over the budget of $629,982 predominantly due to Part 13 Council Owned Utilities remission ($175k vs a budget of $120k). This

is funded from additional rates income.

·

|

Confirmation of statutory compliance

In accordance

with sections 76 – 79 of the Local Government Act 2002, this report is

approved as:

a. containing

sufficient information about the options and their advantages and

disadvantages, bearing in mind the significance of the decisions; and,

b. is

based on adequate knowledge about, and adequate consideration of, the views

and preferences of affected and interested parties bearing in mind the

significance of the decision.

|

Attachments | NGĀ

TĀPIRINGA KŌRERO

|

No.

|

Title

|

Page

|

|

a⇩

|

Financial Dashboard as at 31

March 2025

|

121

|

|

Risk and Assurance Committee

30 April 2025

|

|

|

Risk and Assurance Committee

30 April 2025

|

|

File No.:

25/202

5.7 Treasury

Update - March 2025

|

Author(s)

|

Pei Shan Gan

Financial

Controller | Kaiwhakahaere Tahua Pūtea

|

|

Approved by

|

Jacinta Straker

Group Manager

Organisation Performance | Tumu Rangapū, Tutukinga Whakahaere

|

|

|

Monique Davidson

Chief Executive

Officer | Tumuaki

|

Purpose | TE PŪTAKE

1. To update the committee on the treasury activity for the last

quarter, which is outlined in the Bancorp Treasury Reporting Dashboard for the

March 2025 quarter.

This matter

relates to Ensuring Financial Discipline and Management

Monitor Treasury

opportunities to take advantage of favourable interest rates, reduce debt

servicing costs, and maintain the Council’s credit rating.

Provide transparent

financial reporting and regular updates to the community on the Council’s

financial performance and initiatives.

Ensure financial

discipline and compliance with our financial strategy and benchmarks.

RECOMMENDATION | NGĀTAUNAKITANGA

A. That Report 25/202 Treasury Update - March 2025 be received and

noted.

B. That this matter or decision is recognised as not significant in

terms of S76 of the Local Government Act.

C. That the Committee notes the Bancorp Treasury Reporting Dashboard for

the March 2025 quarter.

D. That the Committee notes the presentation from Bancorp Treasury that

is tabled at the committee.

bACKGROUND | hE

KŌRERO TŪĀPAPA

2. This

quarterly Treasury Reporting Dashboard is produced by Council’s treasury

advisors, Bancorp Treasury Services Limited.

3. The

Local Government Act (LGA) 2002 requires:

· liabilities to be

managed prudently and in a manner that promotes the current and future

interests of the Community (Section 101(1));

· A Liability

Management Policy to be adopted by Council (Section 102); and

· specific content

of such a policy (Section 104).

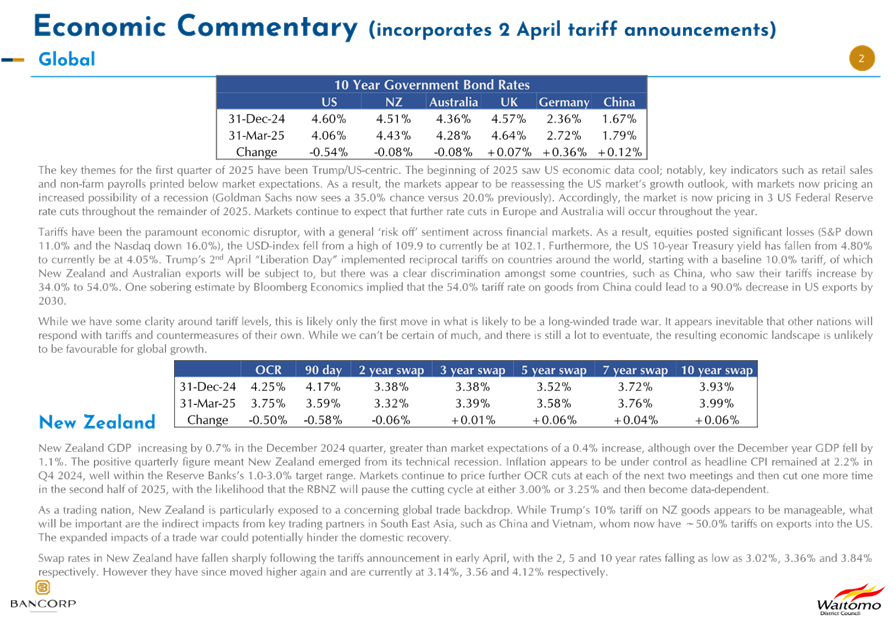

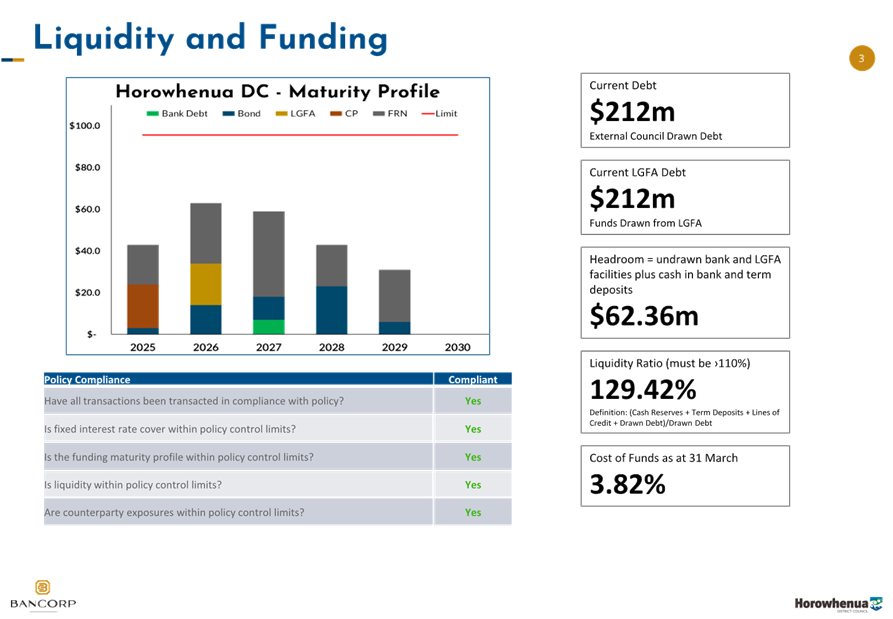

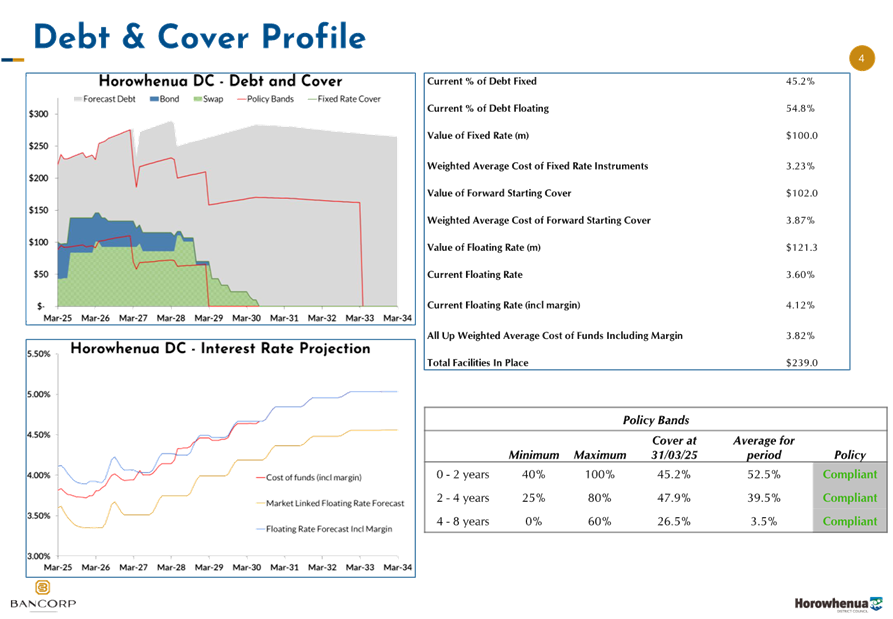

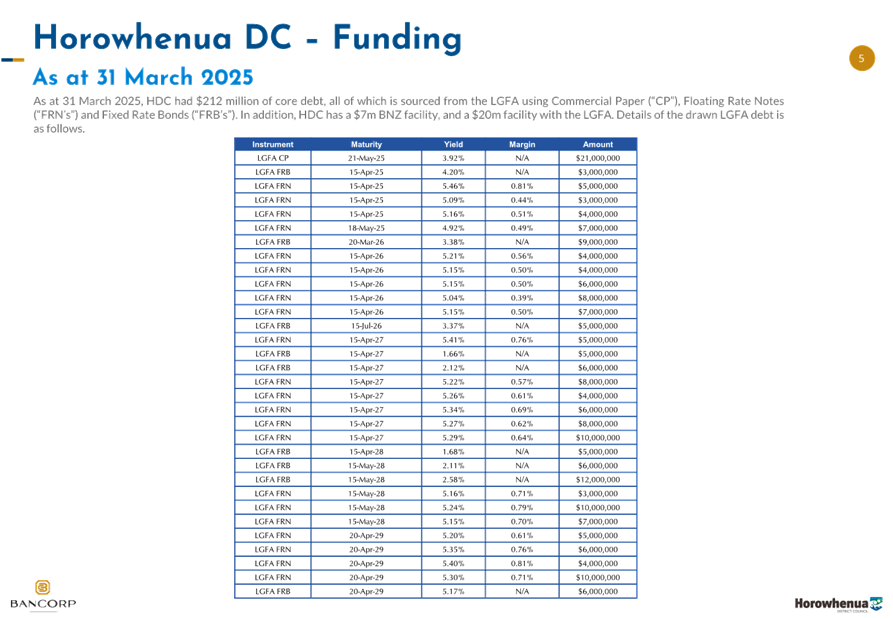

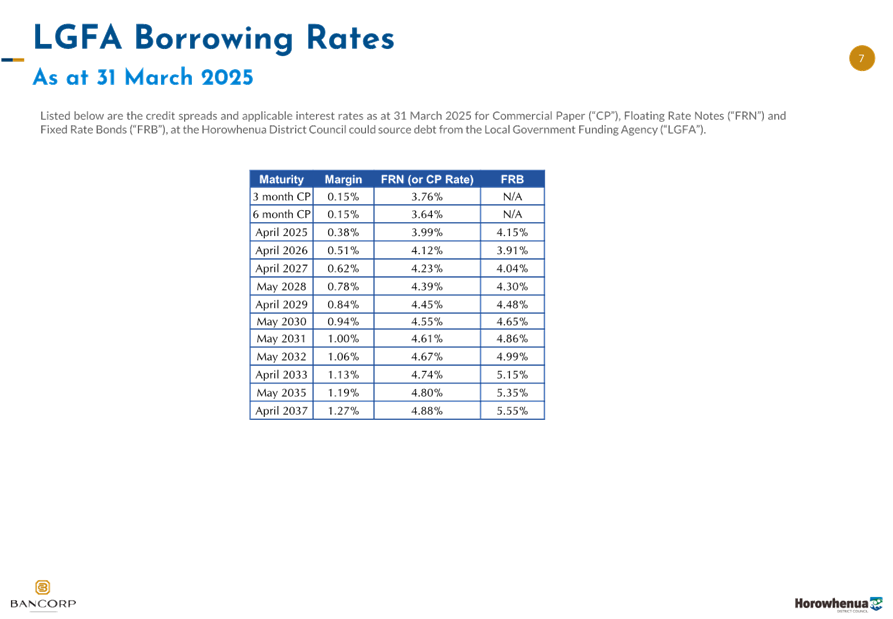

DISCUSSION | HE MATAPAKINGA

4. Council

had $212m of current external debt as at 31 March 2025 (no change since the

last quarter), which was all sourced from the Local Government Funding Agency

(LGFA). $22M of this debt relates to funds borrowed last year and placed on

term deposit to repay debt coming due this financial year. Currently fixed term

debt is $57m and represents 47.2% of our total debt. Floating debt is $155m and

represents 52.8%.

5. Council

is in compliance with it’s the debt profile targets set in its Treasury

management policy:

|

Years

|

Minimum Fixed Rate Amount

|

Maximum Fixed Rate Amount

|

Sept

|

Dec

|

MAR

|

Compliant

|

|

0

- 2 years

|

40%

|

100%

|

47%

|

47%

|

45.2%

|

|

|

2

– 4 years

|

25%

|

80%

|

46%

|

49%

|

47.9%

|

|

|

4

-8 years

|

0%

|

60%

|

30%

|

27%

|

26.5%

|

|

6. Since

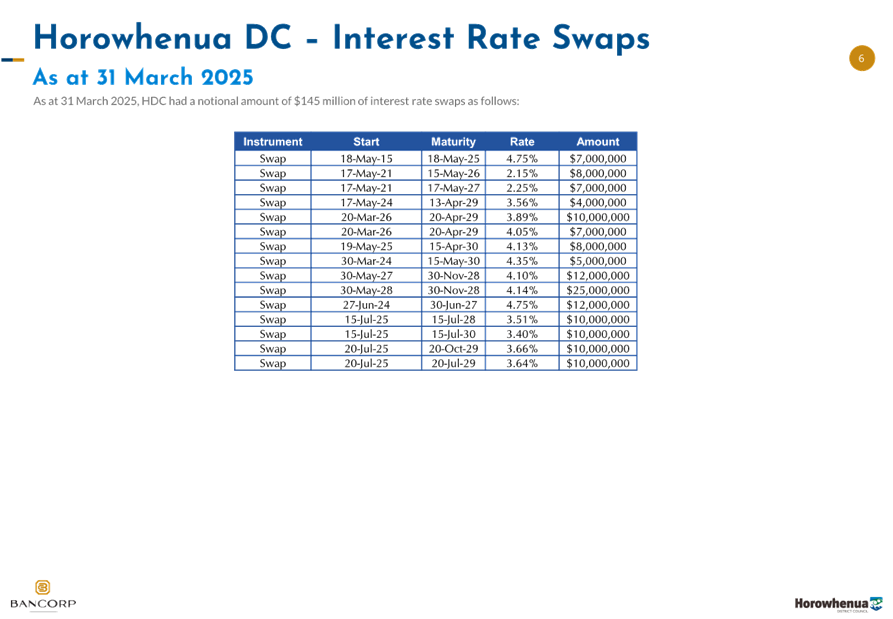

1 July 2024, we have entered into $50m worth of interest rates swaps.

|

Amount

|

Maturity

|

Rate

|

|

$10m

|

17-Jul-28

|

3.51%

|

|

$10m

|

16-Jul-29

|

3.48%

|

|

$10m

|

15-Jul-30

|

3.4%

|

|

$10m

|

23-Oct-29

|

3.67%

|

|

$10m

|

23-Jul-29

|

3.64%

|

We initially planned for a further

$22.5m of forward start swaps in the last quarter with maturity in 2029 and

2030 when interest rates are within the range from 3.6% to 3.65%. This did not

eventuate due to the volatility in interest rate market. Officers continue to

monitor interest rates closely together with Bancorp and will make prompt

decisions on utilising forward swaps as the market changes.

7. Our

average cost of funds as at 31 March 2025 was 3.82%. As at 31 March 2025, net

interest against budget and forecast is depicted in the table below. The higher

forecast is largely due to the interest free loan of $12.5m from Crown

Infrastructure Partners being delayed to 25/26 due to the project timeframe

shifting.

|

|

Actual as at

31 March 2025

|

2024/25 Budget

|

2024/25 Forecast

|

|

Interest

Revenue

|

$0.865m

|

-

|

$1.326m

|

|

Interest

Expense

|

$7.324m

|

$7.624m

|

$9.420m

|

|

Net

Interest

|

$6.459m

|

$7.624m

|

$8.094m

|

8. Council

did not borrow as part of the LGFA bond tender on the 12th of March.

Prefunding for our 2026 debt maturities was completed as part of the tender on

the 10th of April. A total of $43m was borrowed as prefunding. This

is borrowing will be put on term deposit to repay borrowings coming due in the

2025/26. No other extra borrowing was required in the March quarter.

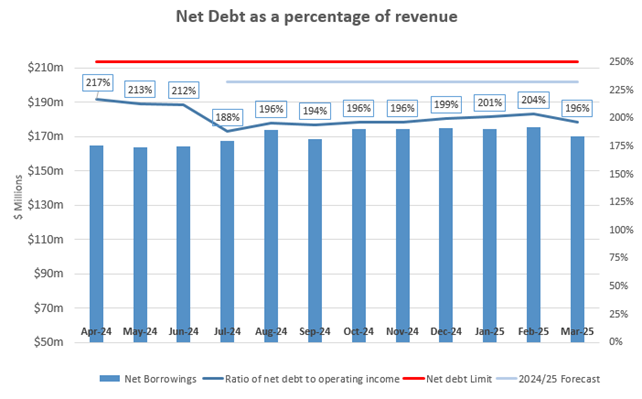

9. Council’s

net debt to total operating revenue as at 31 March 2025 is 196%. Officers have

continued to closely monitor the net debt to operating income ratio, which is

now expected to be below the budgeted level of 229% due to the net reduction in

the capital programme of $5m. This remains below the 250% financial strategy

limit.

10. Council has

recently confirmed the review meeting date for the annual credit rating review

with S&P Global Ratings. Meetings will be held with Council Officers and

the Mayor on 29 May and the rating will likely be provided in late June.

Next Steps | Hei Mahi

11. The Committee

will be discussing the options for credit rating services as part of a public

excluded session following this report.

·

|

Confirmation of statutory compliance

In accordance

with sections 76 – 79 of the Local Government Act 2002, this report is

approved as:

a. containing

sufficient information about the options and their advantages and

disadvantages, bearing in mind the significance of the decisions; and,

b. is

based on adequate knowledge about, and adequate consideration of, the views

and preferences of affected and interested parties bearing in mind the

significance of the decision.

|

Attachments | NGĀ

TĀPIRINGA KŌRERO

|

No.

|

Title

|

Page

|

|

a⇩

|

Horowhenua DC Treasury Report

as at 31 March 25

|

126

|

|

Risk and Assurance Committee

30 April 2025

|

|

|

Risk and Assurance Committee

30 April 2025

|

|

Exclusion of the Public : Local Government Official

Information and Meetings Act 1987

The following motion is submitted for consideration:

That the

public be excluded from the following part(s) of the proceedings of this

meeting.

The general

subject of each matter to be considered while the public is excluded, the

reason for passing this resolution in relation to each matter, and the specific

grounds under section 48(1) of the Local Government Official Information and

Meetings Act 1987 for the passing of this resolution follows.

This

resolution is made in reliance on section 48(1)(a) of the Local Government

Official Information and Meetings Act 1987 and the particular interest or

interests protected by section 6 or section 7 of that Act which would be

prejudiced by the holding of the whole or relevant part of the proceedings of

the meeting in public, as follows:

C1 Discussion on the Options for Credit Rating Services

|

Reason:

|

The public conduct of the part of the meeting would be

likely to result in the disclosure of information for which good reason for

withholding exists under section 7.

|

|

Interests:

|

s7(2)(h) - The withholding of the information is necessary

to enable the local authority to carry out, without prejudice or

disadvantage, commercial activities.

|

|

Grounds:

|

s48(1)(a)

The public conduct of the part of the meeting would be

likely to result in the disclosure of information for which good reason for

withholding exists under section 7.

|

|

Plain English Reason:

|

This report is to facilitate a discussion of potential

suppliers. Discussion of this item in public would disadvantage Council in

potential future negotiations.

|

C2 Risk Management Quarterly Report

|

Reason:

|

The public conduct of the part of the meeting would be

likely to result in the disclosure of information for which good reason for

withholding exists under section 6.

|

|

Interests:

|

s6(a) - The making available of the information would be

likely to prejudice the maintenance of the law, including the prevention,

investigation, and detection of offences and the right to a fair trial.

|

|

Grounds:

|

s48(1)(a)

The public conduct of the part of the meeting would be

likely to result in the disclosure of information for which good reason for

withholding exists under section 6.

|

|

Plain English Reason:

|

This report identifies potential vulnerabilities and

strategies to manage these vulnerabilities. Disclosing these would

negate the effectiveness of risk mitigations..

|